Welcome to Macau!

On behalf of the Macau Insurers Association and the Organising Committee, I would like to warmly welcome you to the 28th East Asian Insurance Congress.

The theme of the 28th EAIC is “The Future of Insurance – Customer-Centricity”. The healthy development of the industry depends largely on whether we are able to anticipate what customer needs will be. We must get ourselves ready to manufacture products that fulfil these needs and to offer the customer an experience that exceeds expectations and more.

Customers’ expectations are rising. In this fastchanging world, we are not only competing among industry players, we are competing with outsiders such as technology companies which thrive on speed and want a share of our market. We not only need to keep up, we need to move faster. We have to compete on the overall experience we offer customers from the very first contact!

Where great minds meet

EAIC offers the perfect place for this meeting of great minds and exchange of great ideas. We have a full programme to help us gain a better insight into who our customers are, how we can serve them better, what role technology plays, what impact the ageing population may have, and what the ultimate operating model is in an ever-changing marketplace. We hope you will be inspired by a host of world-class practitioners and speakers.

Besides being a convention centre, Macau welcomes you as a tourism and leisure destination with world-class attractions.

Meet up with old friends, make new ones, and enjoy the warm Macanese hospitality!

Mr Chris Ma

Chairman, Organising Committee, 28th East Asian Insurance Congress

The great expectations

We meet at a time of great expectations and great buzz over InsurTech and how innovative disruption is changing the whole world. There are some who are very much already on the bandwagon and themselves leading change. Several insurance innovation labs and garages have sprouted all over the region. And then there are the doubting-Thomases who still insist that insurance is so unique and specific and regulation-driven, that it will not be subjected to disruption.

But the big guys are already investing in InsurTech to find solutions for insurance problems be it in making operations more efficient or coming out with new products that appeal to consumers.

Pampering the customers

And that is the heart of this EAIC with the theme: “Being Customer-centric”. It is simple and bold and revolutionary, bearing in mind that insurance has traditionally been sold rather than bought. But people are waking up to the times as they get richer and have real assets they want to protect. They know, learning from Gen Y, what they want, how they want it and when they want it. So now is the time to strike. Even insurance is going to have its day on stage given the more inquiring seekers who want comfort and convenience.

The simpler the better

So being customer-centric will get that much easier if only people will make insurance simpler with less exclusions and less fine print. It is the small print, exclusions and no-claims bonuses that pound the image of insurance away. Denying claims based on fine prints is the one hot potato that kills the image of insurance even today. No claims bonus while excellent for risk management effectively penalises a policyholder for using his insurance? Is this the message to win customers?

Claims: A blame game

In making insurance customer-centric, attention should be paid to claims. Claims is the very raison d’etre of insurance. Yet claims denial no matter how legitimate is also the very death knell of the industry which gets affected by a single company’s act. So something needs to be done in the claims management front at C-suite level. The industry needs to be differentiated from its players and by its players. Customer-centric really means customer is King with executive powers too and not just a lip service or constitutional monarch. This is the future of insurance. Building a business model that responds to customers with a strategy to educate the customer on the value of his own insurance policy and the value of the insurer. Will FinTech and InsurTech get the industry up close and personal profitably with the customer? This is the billion-dollar question but massive investments in several quarters have been made to check this potential out.

What do EAIC customers want?

So at this EAIC, let’s be mindful of what the customers want? What do EAIC attendees want? Aside from the usual meeting old friends, keeping to tradition of being seen at the most important biennial insurance event of the year in Asia, the younger delegates want to see quality speeches and thought-provoking discussions. But with the lure of networking with reinsurers and reinsurance brokers in attendance as well as the renewal being round the corner with rate competition still a possibility, the temptation to skip sessions to meet clients is still strong.

EAIC and SIRC

Perhaps when the SIRC becomes an annual affair from 2017 onwards and renewals can be handled exclusively at the Singapore Rendezvous, the EAIC will revert to its aim of stimulating great ideas to promote greater regional dialogue and business co-operation. It can also tackle the matter of making EAIC more inclusive to draw in the other bigger markets of East Asia. China, the largest still remain conspicuously outside the EAIC.

EAIC still has room to grow and flex its muscles! Who will take the cudgels to do so for this venerable institution of 54 years of age?

Staying dynamic

The current market environment is challenging for all, but Mr Malcolm Steingold, CEO of Aon Benfield Asia Pacific is positive about the industry’s future. He shares his thoughts with us on growth, innovation and the potential of Asia.

Like everybody else, Aon Benfield’s priority is growth. “Opportunities don’t come to you, you have to seize them, and you have to adapt to new business models based on creating opportunities,” said Mr Steingold.

Creating such opportunities, Aon Benfield’s business model has changed to fit the times; with its treaty reinsurance brokerage business as the core, a substantial amount of its revenue is starting to come from non-recurring appointments. For example, the firm has been working with clients to enhance capital management, provide a rating agency advisory service and assist in M&A deals.

They have also been focusing on specialties like agriculture, marine, retrocession coverage and life reinsurance. “In the current market environment, these are strong growth areas, particularly agriculture. Our retro group, for example, has grown significantly despite the current market environment,” he said.

At the same time, Aon Benfield continues to set itself apart from the competition through technological innovation. “We’ve developed a software product called PathWise™ which is an incredibly powerful tool that helps life companies assess their financial data on a realtime basis. There is a huge amount of data and life companies have to understand the embedded liability in their portfolios. Where they used to run figures on a quarterly or monthly basis, they can now make their assessments in real-time for more granular assessment of their exposures.”

Staying ahead of the curve

In addition to an innovation centre in Ireland, Aon Benfield has also recently set up another centre in Singapore, another foothold for their expansion within Asia. “We want our innovation centre to be where the global economy is developing and we see great opportunity in Asia. The Singapore government is a very good partner as it actively encourages and provides an environment for innovation.”

Aon Benfield’s focus on data and analytics and its drive towards innovation is a way of future-proofing its business in an era of new emerging risks. “Underwriters are comfortable writing risk they can quantify, but as clients develop more sophisticated approaches, they become more confident in retaining their risks,” said Mr Steingold. “So underwriters need to start thinking about remaining relevant. The industry doesn’t have an option but to innovate and to develop solutions to emerging risks.”

Of the emerging risks that are the topic of discussion within the industry today, cyber risk is one of the most prolific and it sits very high on the Aon agenda. “Our approach to cyber and the development of cyber is we have taken experts in the area – not insurance or reinsurance experts, but IT experts to develop solutions. And we’ve realised that the solution needs to work for both clients and carriers.”

Aon’s global team working on cyber has engaged various external stakeholders to assist in the development of innovation such as the Aon Cyber Enterprise Solution. The initiative is also being supported across all its business units, be it insurance or reinsurance.

“In Asia, there’s some demand for cyber protection, but the demand does not reflect the exposure,” he said. “However, I think that will change quite rapidly. Once we start seeing decent limits available for clients at prices they’re willing to pay, we’ll see a great deal of growth in the area.”

Having boots on the ground

According to Mr Steingold, Aon Benfield’s Asia Pacific team used to be concentrated in Singapore. However, its new strategy now revolves around decentralising. “We’re putting our capabilities on the ground, on a country by country basis, so that our people are closer to the clients,” he said.

This has led to a twofold effect – it is more efficient from a cost perspective and it also enables them to work closer with the clients. “In terms of our overall strategy, it’s still based on really investing and continuing to differentiate ourselves on data and analytics, in addition to having very local teams.”

On the topic of the potential for growth in specific markets, Mr Steingold was highly optimistic about the region as a whole. “I find myself very bullish about Indonesia – large population, low penetration – and the Philippines. The economy there is starting to gain momentum and it’s an area where we’re starting to gain some traction.”

In the pursuit of superior service

Personalised service

This focus on the customer sets the standards in all Allianz products and services, defines our principles on business and digitalisation, and forms the basis for our growth strategies globally.

Allianz serves more than 85 million customers, though our unique capabilities means we are able to serve each customer as a segment of one.

We have been gradually transforming our business around this pivot, adapting alongside our customers as they face a fast-changing world.

Globally, and again probably more so in Asia, the way our customers want to be engaged have also switched – they want insurance, but on their terms – meaning they want it simply, transparently and quickly.

For us, this means a clear need to make our brand, products and services accessible across diverse touchpoints - digitally, on mobiles, in branches, with well-trained agents, via partners, in cars & cabs.

The journey to get there has also been incredibly exciting – a lot of listening, training, leveraging data, venturing with new partners, experimenting and learning new skills.

Mr Lars Heibutzki,

Chief Distribution Officer, Asia Pacific, Allianz

The Promise

For Aon, any discourse on customer-centricity can never depart from the topic of the Aon Client Promise. It rests upon the pillars of Partnership, Expertise, Innovation, Excellence, and Results.

Partnership. It is our mission to be responsive and trusted advisors to our clients. We achieve this by anticipating the needs and priorities of our clients, while developing and executing on shared objectives to achieve the desired outcomes.

Expertise. In every situation possible, we bring our customers the best of Aon by augmenting their risk management strategies with qualified and talented professionals. A key part of this is achieved by our commitment to attracting, retaining, engaging, and developing our talent pool.

Innovation. Aon invests in creative ideas, fact-based solutions, and pragmatic research initiatives that anticipate the needs of the markets we play a part in. This customer-centric approach to innovation spearheads the creation of industry-leading solutions, thereby creating distinctive customer value.

Excellence. Embracing customer centricity starts with the goal of serving our customers well. Backed by solution-oriented benchmarking and relevant analytics, we offer insightful and useful advice that clients trust.

Results. A key tenet of customer-centricity is to truly listen to our customers which will enable us to understand their needs, especially within the risk environment. This is always the first step in our commitment to ultimately helping clients produce stronger returns on their investments in risk and people.

Mr Rodolphe Guillard,

Chief Client Officer, Aon Risk Solutions, Singapore

Active, lifelong partner

At AXA, being customer-centric means we ensure that the customer is at the heart of every stage of designing the customer journey. We strive to deliver a fast, easy, clear, relevant and empathetic customer experience that matches their expectations in both digital and face-to-face environments. For example, our customers in China can complete the whole claim process entirely on WeChat, while customers in Thailand can quote for policies, ask about products and interact with our customer service agents using LINE stickers. It’s all about making ourselves available in their preferred everyday channels.

More than that, it is about establishing a mindset of being an active, lifelong partner throughout our customers’ various life stages with not just protection, but also preventive care to support their health journeys and well-being. Innovation in analytics and insurance technology will enable us to customise our products and services down to a scale much more relevant and responsive to customer behaviour.

Mr Frederic Tardy,

Regional Chief Marketing, Digital, Data & Customer Officer, AXA Asia

Insurance made easy

Insurance has been giving people an impression of being boring, not easy to understand, and not very relevant to daily life. At FWD, we have a vision to change the way people feel about insurance. We think insurance should be liberating, connected to people’s everyday life by covering a lifetime of todays.

At FWD, the journey of a new customer experience begins with the innovative and easyto- understand protections we offer. We create simple products that come with great flexibility and options to suit different needs, with a tendency to avoid complicated wording and terms. We also streamline insurance application, underwriting and claims processes because these are the moments of truth where insurance customers can practically experience the insurer’s service.

We are also keen on making ourselves easily accessible. Our omni-channel distribution and multi touchpoint services allow our customers and the public to reach us anytime and anywhere.

Mr David Wong,

CEO, Hong Kong & Macau, FWD

The moments that matter

What makes Marsh unique is our purpose – which is to make a distinctly positive impact on the businesses, people, and societies we serve by providing guidance and support during critical moments. We make a difference in the moments that matter.

Our approach is built on one basic objective: establishing a thorough understanding of our client’s business. With Marsh 3D, we are focused on:

- Defining opportunities to lower risk, improve efficiency, and reduce costs.

- Designing an optimal risk management strategy tailored to clients’ situations and risk profiles.

- Delivering results that are aligned with clients’ business objectives.

We are then able to maximise the return on clients’ risk management investment through increased efficiency, improved business-risk decisions, and lower cost.

Mr Alistair Fraser,

Managing Director, Head of Sales – Asia and Head of Insurer Consulting Group Practice – Asia, Marsh

Data, insight, communications

In the past decade, new technology and explosive data growth have empowered our customers in new ways; it is essential that Generali understands the new factors underlying purchasing decisions and create meaningful value for our customers. We have developed new capabilities to transit from traditional products and propositions to customer-centric ones.

These capabilities include customer-centric servicing models for our multinational program customers, 360-degree offering for our Construction customers as well as advanced segmentation and data analytics to provide the best-in-class solutions.

- Data – We have shifted our focus from products to customers by adopting a full-fledged Client Relationship Management (CRM) tool. By gaining a deeper understanding of our customers, we have leveraged customers’ data to provide comprehensive and relevant solutions, tailored specifically to their business and industry needs.

- Insight – Data analytics enable deeper insight, understanding and segmentation of our customers, products and markets, allowing Generali to provide precise and optimized risk management solutions for our customers.

- Communications – We provide a tailored offering in accordance with our customers’ needs, business strategy, industry trends and long-term risk management goals.

Ms Tricia Koh,

Head of Value Proposition & Marketing, Asia, Generali

Tangible value over customer’s lifetime

Customer centricity is about first studying consumer needs, wants, fears, pain points, and aspirations, then developing innovative and differentiated products, services and experiences that significantly improve the customer’s life in one or more areas.

It’s about creating tangible value in the customer’s life, and as a business, reinvesting to continue building and expanding that value over the customer’s lifetime.

It’s about measuring success through customer satisfaction and loyalty, earned by consistently listening to the customer and adding value to the relationship.

We also leverage advanced data analytics to transform data into customer insights that enable us to deliver more personalised and relevant service to customers – the right product offered at the right time, by the right distributor with the right understanding of consumer psychology. And adopting a test and learn approach – dynamic learning – to continually improve our performance to serve customers better.

Mr Ralph Brunner,

SVP – Global Marketing Strategy, Advanced Data Analytics, MetLife Asia

A reliable partner

At Peak Re, being customer centric means having the time and willingness to listen to what a customer is looking for, and then letting them know quickly whether we can deliver what is being sought. Peak Re’s approach has meant delivering on the things that we said we would do – settle claims quickly, be a reliable and equitable partner and be consistent in our approach.

I think it has been shown that we’ve built this into our approach successfully, as much of our growth comes from customers with whom we already have a business relationship. The approach is understood and applied throughout the organisation – everyone in Peak Re knows that without satisfied customers, we have no business in the longer run.

Mr Chris Kershaw,

Managing Director, Global Markets, Peak Re

The need for a hub

Mr Patrick Rozario, Managing Director of Moore Stephens Advisory Services, and Mr Paul Latarche, Partner and Head of Insurance at Moore Stephens, discuss the current issues faced by the Asian insurance market and how technology will play an increasing part in the solutions.

Q: How do Asian underwriters’ processes (ie, rating, underwriting and distribution) compare to more mature markets?

Patrick: Asia is complex with different markets at different stages of development. All have different issues and problems but we see a lot of insurers run on regional structures. And while they market similar products, the formation of those products can be quite different.

The collation and analysing of data is challenging particularly in emerging markets where there are underwriters who still use spreadsheets. The bigger the underwriters, the more the sophistication and it is the domestic underwriters of emerging markets that are having the more significant issues.

In terms of distribution, the brokers are having to contact the individual underwriters by phone or fax to deliver the risk details or obtain comparative quotes. Some underwriters are providing access to their websites but often it can be different forms for the same risk. There is a need for a hub.

Paul: There is a need for brokers, agents and underwriters to be able to access the risks and the pricing information from a single point. Underwriters are working hard to see brokers and agents to use technology which allows them to collate data on the risks they are offered, price and their aggregated exposure levels.

Q: What are the key issues for underwriters given the status of the pricing cycle?

Patrick: Pricing in some classes remains an issue due to the level of competition. Marine insurance, for example, is under pricing pressure with Hong Kong and Singapore as the significant underwriting centres for the class. For other classes pricing is not so much of a challenge, but there remain some classes such as PI, for instance, that are routed to London to be underwritten.

Once again it comes back to the issue of communication between the broker and underwriting markets and the ability to deliver and utilise data. The lack of data remains an impediment to underwriting the risk and there is a demand from underwriters for more timely data.

Paul: The ability to access and analyse the data is a particular concern. Underwriters need to have the ability to collect real time data on the product, exposures, and pricing to allow them to make pricing adjustments quickly if markets or claims experiences change.

Q: Where do you see the future for communications between underwriters and brokers?

Patrick: This goes to the core of the markets’ issues. Brokers would like to access information from underwriters by simply providing a single set of risk data that can be accessed across several markets.

Brokers need comparative pricing for their clients and would like to reduce the number of requests they have to submit, while the underwriters would like to remove certain levels of human interaction in the underwriting process.

Brokers simply want to obtain the quotes they require quicker and based on the same information so they and the client can better asses the insurers’ proposal not only on price but terms and conditions and breadth of cover.

Paul: There is the question of standards. Asian markets do have standards, however, they tend to be local and therefore provide another area where underwriters need to understand what they are being asked to adhere to. Systems need to provide the ability to assimilate these standards into the underwriting and quotation processes. It comes back to the fact that Asia is a dynamic region for the insurance sector not only in terms of growth but the level of maturity in the individual markets.

Q: What do you think will be the key topics for delegates at EAIC?

Patrick: I expect regulation will be a significant topic. Consumer protection has been a topic for a great deal of debate between the industry and regulators. We have seen some movement in terms of regulatory regimes across the region, which I expect will be a talking point with some delegates. Processing of data will be an issue, I am sure.

Paul: I would expect that questions around M&A and the movement of capital in the market will be discussed. What is clear is the need for better processing and the ability to communicate with brokers and underwriters across the region and also the global risk centres for business that is currently placed internationally.

Industry wavers between cautious optimism and pragmatism

The major reinsurers projected a positive outlook at this year’s Monte Carlo Rendezvous, seeing the end of the soft cycle on the horizon. However, not everyone shares the same sentiment.

The atmosphere at the 2016 Rendez-vous de Septembre was one of cautious optimism from the major reinsurers and pragmatic realism from reinsurance brokers.

Major reinsurers Swiss Re and Munich Re projected an eventual hardening of the market within the next few years. Mr Matthias Weber, Swiss Re’s Group Chief Underwriting Officer, said that certain segments of the market have already hardened and more will soon follow.

As for Munich Re, it projected a moderate premium growth in the reinsurance sector, with a significantly higher growth for primary insurers. During its press conference at the Rendezvous, CEO Dr Torsten Jeworrek said that the rates for reinsurance were stabilising.

Mr Ludger Arnoldussen, Member of the Board at Munich Re also maintained the Group’s cautious optimism, when asked about their expectations for the upcoming January renewals for their Asian markets. “The competition in Asia is the same as in other markets, with enough capacity and lower prices on the market-level than risk-adequate pricing in many markets. We will focus on sustainable profitability and differentiate through innovation and tailor-made transactions,” he said. “Basically, no big change from our expectations last year.”

Munich Re also expected a 0% growth in Asia Pacific over the next three years, mainly because of its projected negative growth in China due to upcoming capital regulations. However, other markets in the Asia Pacific region are projected to have significant growth in both the primary insurance and reinsurance sectors.

Reinsurance profitability is being squeezed

Reinsurance brokers, on the other hand, have a less optimistic view of reinsurance rates increasing. Mr James Vickers, Chairman of Willis Re International, believes that there will be more capital entering the market. “It’s a permanent part of the market now,” he said of the excess capital currently existing in the market.

“We believe that the underlying profitability of reinsurance is being slowly squeezed, but the reports of results have been satisfactory and within investor expectations. There will be a continued gradual softening of the market, although probably less than we’ve seen in the previous years,” he said. “It is not going to completely stabilise and certainly not reverse.”

Mr David Flandro, Global Head of Analytics at JLT Re said that it would require a confluence of events to remove the excess capital from the market, including a major catastrophe like Hurricane Katrina, hitting the bottom of the reserving cycle and another liability crisis within the space of a few months.

He also said that the (re)insurance market is in danger of releasing reserves, despite accident year experience suggesting redundancies are running dry, as revealed in JLT Re’s latest Viewpoint Report.

“The clear implication is that now is the time to seek protections. Reinsurance pricing is at or near period lows in many medium and long-tail lines and cover is more easily obtained than it has been, even in the recent past for those with the foresight to move quickly,” he said.

Casualty accumulations - Threats and reinsurance solutions

The largest casualty accumulation loss was twice as much as the loss from Hurricane Katrina, yet it is less understood than property catastrophe exposures. This needs to change, says Dr Victor Kuk, Head Hub Casualty Asia at Swiss Re.

Casualty accumulation is the concentration of insured risks or insurance coverages that may be affected by events or circumstances that cause substantial losses under several insurance policies, and potentially over multiple years and geographies.

Casualty accumulations are real risks for our society and insurance companies, and yet they are less understood than property catastrophe exposures. Modelling casualty accumulation is challenging, as only limited historical information is available. This is aggravated by a changing social and legal environment, for which past experience may not be representative for the future. A casualty accumulation such as asbestos can put an insurance company out of business. But what is the next asbestos? When will it happen? How big will it be? How can we protect ourselves?

For the insurance industry, asbestos was undoubtedly the largest casualty accumulation at a current ultimate loss estimate of roughly US$100 billion (twice as much as the loss from Hurricane Katrina in 2005). It is crucial for us to understand how such catastrophes arise and unfold.

Categories of casualty accumulations

Casualty accumulations can be classified into four categories:

-

Classic clash characterised by a sudden and accidental event, for example, the Mont Blanc tunnel fire or the Deepwater Horizon oil spill. This is the simplest form of casualty accumulation.

Further examples include a truck colliding with a bus leading to deaths, injuries and property damage with insurance policies triggered, including motor own damage, motor liability, workers compensation and commercial general liability. Another example could be a building collapse triggering general liability, employer’s liability and professional indemnity claims.

-

Serial aggregation losses, where multiple insurance policies are triggered out of one single defect, such as losses linked to the hazardous properties of asbestos, bisphenol A (BPA) or diacetyl.

For example, inhalation from the butter flavor compound diacetyl causes cumulative lung damage (“popcorn lung” as it is commonly known). Approximately 25 companies are linked to potential “popcorn lung cases” with some defendants having gone bankrupt. It also has the potential to arise in other industries (frozen foods, candy, pastries) where diacetyl is used. This is an example of where one product has impacted multiple companies, industries, and insurance products (workers compensation, products liability, product recall).

-

Business disaster, with multiple losses occurring as a result of a single failure or the disclosure of incorrect/misleading advice/ information.

For example, the bankruptcy of Enron or the Madoff Ponzi scheme. Enron went insolvent in 2001 which ultimately led to the demise of auditing company Arthur Anderson. Suits were filed against directors & officers liability policies, auditors professional indemnity, and financial advisors. The estimated P&C industry loss was $700 million.

Outside of insurance policies, many insurance companies had to write-off the loss to Enron stock on their balance sheets.

-

Systemic losses, where a repeatable process/procedure or industry/ business practice results in a series of losses over a period of time. For example, IPO laddering practices in the financial industry, pension mis-selling or sub-prime.

Another example is the concussion cases in sport. Repeated concussions have been linked to a degenerative brain disease (chronic traumatic encephalopathy or CTE). Approximately 1.6 million to 3.8 million traumatic brain injuries per year occur in the US. Claims can affect manufacturers of sporting goods, sports clubs, schools, and federations (eg, the NFL).

Actively managing the risk

Insurers face a diverse set of accumulation scenarios and must become more aware of such exposures. Particularly with the lessons of asbestos, history teaches us that the casualty accumulation risk must be actively managed.

Should a large casualty accumulation arise, the threat of sizeable and/or continuous reserve increases are considered to be the main dangers for insurance companies as they can have an impact on their capital, profit and financial strength ratings.

Outside interest in casualty accumulation is growing. Rating agencies and regulators are scrutinising it more than ever and are very interested in (re) insurance companies’ exposures to accumulation risks and how they quantify and manage those accumulations.

Today, casualty accumulation management is still in its infancy, but growing fast. Similar to managing property catastrophe risks, reinsurance products tailored to meet the reinsured’s needs play a central role.

Swiss Re has solutions to help our clients manage their casualty accumulation risk. Swiss Re is on the forefront of making the insurance industry more resilient against accumulation risk, by raising risk awareness within the insurance industry, by creating and implementing state of the art accumulation management tools, and by leveraging its own underwriting expertise to find tailor-made solutions for our clients.

Evolving with the times

The rapidly changing business environment is prompting innovation and change from all corners of the industry. Mr George Attard, Head of Aon Benfield Analytics International, discusses what it takes to keep up with the constantly evolving customers and market.

Since the major catastrophe events in 2011, data quality in the region has made vast improvements, both in accessibility and analysis. “If we look across the region, it’s the more progressive domestic insurers, and global players that are importing and sharing best practices. There have been regulatory and rating agency changes, including a growing trend toward risk-based capital and increased oversight that are also driving better data practices,” said Mr Attard.

One of the key factors to this improvement is the knowledge transfer and insights that Aon Benfield has been able to provide to their clients to leverage their data as a strategic asset, by demonstrating the impact of data quality and uncertainty and how it impacts modelling outcomes and how that then impacts their understanding of risk. The firm also takes steps to help clients understand that better data means an improved ability to underwrite and price risk.

There is plenty of room to grow, however, and not just within Asia. As the market continues to evolve, there will be an increased demand for data and clients looking to better understand what the impact is on their portfolios. “Interestingly, over time, we can expect to see importance move to less reliance on the policyholder, as we start to leverage other data sources using big data techniques to provide the relevant information to better underwrite and assess a particular risk,” said Mr Attard.

Other data sources, in this case, means public data sources, external data providers and an insurer’s own data, including everything from social media to weather data to telematics to connected devices.

Further, there are efforts to supplement or aggregate the existing data from the industry. Aon Benfield is a founding member of the Natural Catastrophe Data Exchange Alliance (NatCatDAX) in Singapore, a private-public partnership with the Monetary Authority of Singapore (MAS) that aims to accomplish this by increasing both insurance and economic data availability for natural catastrophe risks in Asia. This will enable better understanding of the underlying risk exposure, and when a loss occurs, allows them to collect an estimate from contributing insurers to enable greater transparency of industry losses.

Collaboration is the future

Aon Benfield is no stranger to private-public partnerships, having engaged with several government initiatives all across Asia – including the aforementioned NatCatDAX. Mr Attard believes that a collaborative approach is how these partnerships can make a real impact.

“With the increased focus on closing the protection gap, there has been a concerted effort to increase risk awareness and improve resilience through increased collaboration with initiatives such as the NatCatDAX in Singapore and globally the Insurance Development Forum,” he said.

While the impetus needs to come from the governments in promoting risk awareness within a particular market, driving compulsory insurance and also providing funding, Mr Attard’s own experience working with such partnerships has highlighted the importance of analytics.

Acting as an enabler to help governments understand what is required to enact or enforce a sustainable risk financing strategy over time, analytics also helps to pinpoint exactly where the governments, the global reinsurance industry and the local insurance market can play a part.

“For example, the local insurers have the infrastructure in order to deploy products and offer services such as policy administration, claims management and disbursement, so a partnership approach needs to be taken. You need to get all the key stakeholders at the table, to enable a sustainable outcome.”

How governments can help

“I think continued industry dialogue with governments and regulators is important,” he said.

In this rapidly changing landscape, governments also need to look at how it can facilitate innovation. Mr Attard pointed out the MAS and its implementation of the regulatory sandbox – a “safe space” in which businesses can test new concepts – as a positive example of encouraging innovation. It protects investors and policyholders, while also allowing innovators to experiment new products in a carefully managed environment.

Innovation, however, also leads to disruption, which has been the word du jour for anyone in the financial services. “We should all be considering how we might be disrupted and be prepared to respond accordingly.”

Aon is monitoring startup accelerators and incubators and seeing what venture capitalists are doing and where they are investing. As of now, everything across the value chain is of interest, as any inefficiencies present opportunities for innovation and disruption.

Aon, however, is not alone in embracing this change. “You’ll find that many progressive insurers have partnered with these innovative startups. Rather than feeling threatened, they are embracing it into their overall strategy,” he said.

Asia reinsurers set sights on a wider world

Asia has grown in importance for insurance and reinsurance as the economies in the region grew at a fast clip, some at double-digit figures for decades. International as well as domestic players have mushroomed and local companies have not only expanded their reach outside their countries into the region but are now going global too.

Globalisation is a matter of practicality for most Asian reinsurers. According to the National Reinsurance Corporation of the Philippines (PhilNaRe), the emerging markets in Asia need to be more globally competitive in order to grow properly.

Mr Augusto Hidalgo, President and CEO of PhilNaRe said: “Operating in catastrophe prone Philippines means we need to increase geographical and line of business diversification. This means cautiously writing more global business within appetite and underwriting competencies.”

Similarly for Japan-based The Toa Reinsurance Company (Toa Re), globalisation is the most direct path towards diversification of risks, helping them ensure a stable profit.

Catching up with the global market

Within their own country, a local (re)insurer can depend on longterm relationships within the private and public sectors to remain competitive. However, expanding globally and regionally will prove challenging in terms of building such connections, so technical expertise is required. Said Mr Hidalgo, “We must enhance our emerging market customers’ competitiveness by raising competence in capital management and technical skill. With this, they can more easily defend shares at home and be competitive abroad.”

The reinsurers we interviewed agreed that technical competencies and a customer-centric approach were important prerequisites for success. “What a reinsurer makes out of the market depends on these factors. That is why there are weather-beaten long-term players as well as fair-weather friends and fly-by-night operators in this business,” said Mr S A Kumar, President and CEO of Asian Reinsurance Corporation (Asian Re).

“There is no doubt that how long you have been in the market makes a big difference in your technical expertise,” said Mr Jong-Gyu Won, President and CEO of Korean Reinsurance Company (Korean Re). “However, Asian players in the (re)insurance industry are catching up fast with their counterparts in the advanced markets. There may even be some areas where Asian regional players know better than international players, such as knowledge of local market conditions and needs. This makes it crucial to seek cooperation with each other whenever necessary.”

The need for technical expertise

In an environment where the biggest names have been dominant for decades, having built strong long-term relationships with clients and set roots down in every major market in the world, Asian reinsurers are doubling down on their technical expertise in order to remain competitive as they enter the global playing field.

Mr Zainudin Ishak, President and CEO of Malaysian Reinsurance Berhad (Malaysian Re), said: “Technical expertise is important as this industry is driven by the quality of human capital and this is not only limited to underwriting expertise alone but other areas such as investment, risk management and actuarial are equally important.”

Mr Chris Kershaw, Managing Director of Global Markets at Peak Reinsurance Company (Peak Re), expanded on the topic: “The expertise needed is no longer the narrow catastrophe focused expertise of yesterday, but rather the business savvy expertise that understands and adapts to the markets in which our clients and their customers live and work. The logic of their being a growth reinsurer active in Asia is not just to be closer to the markets, but to actively engage with and help to address the challenges which emerge.”

Building bonds for better business

Long-term relationships have always been important in the reinsurance business and always will be, as they are crucial in building sustainable business over multiple cycles and remain relevant in the highly competitive Asian market. Globalisation increases the need to build such relationships, utilising knowledge and expertise of local partners to be competitive in a new market.

Mr Tomoatsu Noguchi, President and Chief Executive of The Toa Reinsurance Company (Toa Re) said: “We think these strategies lead to sound business expansion in Asia, eventually contributing to the development of the Asian insurance market.”

From the perspective of Asia Capital Reinsurance Group (ACR), robust relationships are the cornerstone of the industry. Mr Hans- Peter Gerhardt, Group CEO said: “Clients expect us to be consistent, dependable and predictable. These are the key building blocks of a company’s brand and what our business partners continue to value and appreciate. It is therefore important to always be on the ground with your clients so that you can better understand their needs and be able to respond to these needs more efficiently.”

Taking advantage of innovation

In keeping up with global competitors, Asian reinsurers have made significant strides to set themselves apart, innovating and transforming their business at a rapid rate. Integration of new technology, expanding into new lines of business and even restructuring parts of the company to improve efficiency and effectiveness are just a sample of the strategies employed.

In June 2015, Korean Re made the biggest reorganisation of its underwriting operations in its 52 years of history. The Overseas Department was dismantled, and the business that it had undertaken was broken down by line of business and integrated into underwriting teams such as Property, Engineering, Marine and Casualty.

Technology remains a strong driving force in innovation, with Mr Noguchi saying Toa monitors the impact of new technology and telematics in the life and automobile sectors, and the inevitable effects it will have on their clients’ needs for reinsurance and risk management.

“For example, there is a possibility that policyholders’ needs may change due to the progress of preventive care by the development of wearable technology or genetic testing technology. In such cases, new insurance products with more risk segmentation will be developed in accordance with the change of policyholders’ needs,” he said.

ACR has also been exploring technology-based methods, and has been investing in new online distribution mechanisms to share with their clients. “At the same time, we are also bringing in products that have been tried and tested in markets around the world and adapting it to the region and the needs of our clients,” said Mr Gerhardt.

Revenue diversification needed for secure growth

For Malaysian Re, they have been employing several strategic measures to ensure revenue diversification, in the face of the many challenges existing in the market today.

“One of the strategic measures our organisation is looking at is to offer a retakaful service. It is our strategic move that this retakaful division will become an alternative revenue contributor so that Malaysian Re will remain on a sustained footing amidst increasing industry competitiveness,” said Mr Zainudin.

And with the Malaysian financial market moving towards a more liberalised outlook, which would lead to greater business opportunities at the cost of higher levels of competition, Malaysian Re is placing strategic partnerships at the top of its priority list, in order to collaborate on and implement innovations in markets they have a strong presence in.

“Moreover, the establishment of retakaful window is expected to be a salient point to attract other reinsurers who are looking to have cooperation along the retakaful products,” added Mr Zainudin.

Forging ahead

The Asian reinsurers have always faced forward, and have been hungrily eating up the distance between them and solidly established global players. Despite the volatility of today’s financial environment, many of them are taking bold steps to catch up to, and even pull ahead of their competitors.

Talent development seems to be the main focus that is shared between most Asian reinsurers, many of them noticing the need for specialised expertise and skills in an increasingly sophisticated underwriting environment. With intentions of going global, Asian reinsurers are also faced with the challenge of dealing with different global regulations.

“To respond promptly to drastically changing business environments and diversified needs, we essentially need to further improve our expertise and skills on a companywide basis and cultivate personnel who can show appropriate leadership at worksites,” said Mr Noguchi. “Employees are irreplaceable assets for (re)insurers that handle invisible products. We regard human resource development as one of our top-priority issues.”

Mr Won also revealed similar plans, calling it a necessary element of the global expansion. Korean Re launched its global expert programme in March 2015, intended to improve their knowledge and information on various foreign countries which could be its potential markets. 44 countries were initially selected as targets for their research.

Asia’s reputation as the next frontier of insurance has grown rapidly over the past five years and (re)insurers in Asia have grown steadily as a result. With this growth comes a rising ambition to spread their wings and the Asian reinsurers are leading the way.

Stars shine at 20th Asia Insurance Industry Awards

Asia’s insurance industry feted winners from 15 categories at last night’s Asia Insurance Industry Awards (AIIA) gala dinner, which also celebrated the Awards’ 20th anniversary. Taiwan-based Fubon Group clinched two awards – Fubon Life Insurance won the Life Insurance Company of the Year award and Fubon Insurance Co received the General Insurance Company of the Year award. Both were exemplary in filling protection gaps and offering innovative products.

The Singapore College of Insurance won the Educational Service Provider of the Year award for its comprehensive range of training programmes and workshops which catered to all levels of staff, and reciprocal recognition of its qualifications by other respected institutions.

MetLife Asia’s Beautiful won the Innovation of the Year award for its originality in responding to the needs and wants of the underserved segment of women aged 30-50 with proven results.

The Service Provider of the Year award went to MDIndia Healthcare Services for setting benchmarks in the standardisation of costing, treatment and protocols in health insurance in India.

For setting up BengQ’s ERM framework featuring high-level management’s involvement, a risk indicator linked to corporate KPI and business strategies, and a top-down and bottom-up approach to risk management in a complex electronics industry, Mr Danny Lin of QISDA Corporation (formerly BenQ), won the Corporate Risk Manager of the Year award.

The Broker of the Year award went to Marsh (Singapore) for providing wide-ranging and industry-leading reports on insurance and risk management, as well as providing clients with cutting-edge technology tools and unique solutions.

Aon Benfield won the Reinsurance Broker of the Year accolade for bringing value-add to clients via innovative modelling platforms and its many published reports and conferences on pertinent industry developments.

The General Reinsurer of the Year award went to Munich Re for leading the market in risk modelling, published research, Nat-CAT products and new initiatives, including those relating to the digital world, fin-tech and ins-tech.

For its holistic partnership approach, innovative and attractive covers meeting customers’ complex and underserved needs, comprehensive end-to-end distribution solutions and investment in research, SCOR Global Life won this year’s Life Reinsurer of the Year award.

Tata AIG General Insurance Co bagged the Corporate Social Responsibility Award for contributing substantial resources and manhours to improve the lives of the underpriviledged and inculcating a pervasive culture of volunteering within the company.

The Technology Initiative of the Year award went to EAB Systems’ client-centric 121 System which combines a shared engine among different platforms with native user interfaces and provides client and sales-activity management features and easy-to-use configurators, maximising efficiency and productivity, and reducing the time to close sales.

Reinsurance Group of America won the Employer of the Year award for providing quality training programmes for its staff, proactive interactive career management, promotion of an inclusive culture, strong support of employees’ pursuit of professional certification, and provision of change management strategies.

Mr G Srinivasan of The New India Assurance Co was awarded the Personality of the Year for his contributions in representing the insurance industry, especially to the government.

Mr Toshiaki Egashira of MS&AD Insurance Group was honoured with the Lifetime Achievement Award for being the industry’s mover and shaker in his illustrious 30-year career.

This year’s AIIA saw 43 insurers and brokers, risk managers, service providers and industry leaders making it to the prestigious finalist list. The finalists were selected out of close to 400 entries, and 28 of them from nine of the 15 categories were given the opportunity to make their winning bid for the Award at the face-to-face judging process.

A secret ballot was cast and the scores were tabulated and audited by independent auditor KPMG, who was also present at the final judging.

Over the past two decades, the AIIA has seen about 250 nominees emerging as winners from some 10,000 entries.

Be ever-responsive to changing needs

Changing consumer expectations and demographics require insurers to remain dynamic and innovative in adapting their products and distribution to current needs, said Mr Anselmo Teng Lin Seng, Chairman of the Board of Directors of the Monetary Authority of Macao.

He noted that changing customer expectations will have implications for both product design and service delivery, and insurers will have to constantly remodel their propositions to keep up with the evolving consumer outlook.

One example is how life insurers have changed their marketing to focus on the pursuit of healthy lifestyles, he said. Digital technology also requires insurers to improve their level of engagement and accessibility online.

But in the era of technology, insurers should step up their risk management efforts in the face of cyber threats. “It’s become more of a challenge to secure data, so I encourage market participants to balance your risk while pursuing new niches,” he said.

Turning to Macau, he said the market will continue to strengthen its supervisory regime by remaining vigilant on IAIS guidelines. He added Macau is currently in the process of raising the standard of insurance intermediaries and will soon launch a professional training scheme for this segment.

Brexit: Implications and lessons learnt

Brexit is arguably one of the biggest developments in 2016, a decision which reverberated around the world. But what does this mean for the insurance industry and what are the lessons for the region here?

Mr Kent Chaplin, CEO, Lloyd’s, Asia Pacific, cited a recent KPMG report on the implications of Brexit in ASEAN. It suggests that companies in ASEAN need to examine the implications of a potential loss of access to the Single Market via subsidiaries in the UK.

However, they should also consider the potential upside of new trade deals between the UK and ASEAN states as a result of the UK’s new-found status. Once the UK is free to do so outside the EU, the UK’s new Department for International Trade will be seeking to conclude free trade agreements quickly. “Malaysia’s Prime Minister has also said he sees Brexit as an opportunity to improve relations, especially in trade and investment,” he added.

It is probably too early to tell what will eventually happen. Even though UK Prime Minister Theresa May declared her intent to start the two-year process of leaving the EU in March next year. “As of today, nothing has changed. The UK is still very much a full member of the EU,” said Mr Chaplin.

Benefits of market harmonisation

As to what Asia can learn from it, he said that the case of the EU has shown the benefits of greater market harmonisation. It enables the industry to be closer to its customer to better cater to their needs and provide greater value.

“At Lloyd’s we support the importance of building integrated agreements and access to trade and services freely across the region. From an insurance perspective, this permits insurance clients unrestricted access to the growing capacity and expertise available across the region,” said Mr Chaplin.

On the regulatory front, he said that in the case of ASEAN with its varying levels of economic development, it is important to proceed at the pace that the individual markets are comfortable with. In the ASEAN Economic Community (AEC), this may well translate into ensuring the local supervisors retain supervisory responsibility for local insurers.

A model worth looking at is the European Insurance and Occupational Pensions Authority – the EU’s “super regulator”. He said that the Authority has the considerable responsibility for the form that insurance regulation takes in the EU. However, it does not have the day-to-day responsibility for the regulation of individual insurers within the EU, which remains with the national supervisors.

“The greater harmonisation of regulatory regimes across markets will drive improvements in local knowledge and technical expertise,” he said.

What does the “chair” say?

“Generation Y”, in some cases already the industry’s current generation of customers, are significantly more engaged. “This is true across every channel and across every geography. This is an absolutely universal phenomenon, that we have a generation that is growing up wanting to be more empowered and more engaged with service and product providers,” said Mr Andrew Rear, Chief Executive of Digital Partners, Munich Re. Digital Partners is a global, multi-line business working with startups and other businesses which are disrupting insurance.

Consumer expectations

But is the industry ready to engage them?

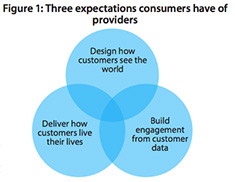

Figure 1 shows the three expectations that consumers have of providers.

Digital innovation is not about taking physical forms and sticking them on the internet, he said.

The empty chair

To meet these customers’ expectations and to improve customer centricity, he cited Jeff Bezos, founder of Amazon, who recognised the importance of keeping the customer in mind by having an empty chair during meetings and asking “What does the customer say?”

For the insurance industry, the “customer” in the empty chair is likely to tell us:

- We need to stop building propositions around our industry and our legacy system and start building propositions around the way customers perceive their own needs.

- We need to stop delivering products to suit our channel structure and start delivering products to suit the way our customers want to live their lives.

- We need to stop treating our customers like strangers that we need to question before we allow them into our club and start engaging customers through data that they are willing to share with us.

“I believe that as an industry we can do this and we can become a customer-centric industry,” he concluded.

Securing future of the industry

Market players should continue to cultivate the dynamism of Asia’s insurance sector in order to support the region’s rapid economic growth, said Mr Jiang Yi Dao, President of the Macau Insurance Association at yesterday’s opening ceremony.

“In the next decade or two, Asia will become the global economic growth engine and the region’s insurance industry can be propelled by this growth, so we need to look after our insurance environment in order to support economic growth,” he said.

A critical element in the sustainability of the sector is the development of new talent and in that regard, the EAIC’s latest initiative to launch the “Young Insurance Practitioners Programme” is a timely move, said Mr Steve Chen, President of the EAIC.

Member cities of EAIC nominated two insurance practitioners under-35 to attend this year’s conference, as both a means to mark Insurance Day, but also crucially to encourage more participation from younger insurance professionals at the EAIC conference in order to regenerate the industry.

The nominated delegates will also have the opportunity to submit suggestions to improve the EAIC conference, added Mr Chen.

Drivers of change in the energy market and risk landscape

Mr Kamal Tabaja, Group Chief Operating Officer, Trust Re, shares the key findings of “The Changing Global Energy Landscape: Opportunities and Challenges for Energy Underwriters”, the research paper produced in partnership with Dr. Schanz, Alms & Company.

In line with our mission “to be innovative in providing reinsurance solutions and prompt responses, always”, we continuously work towards strengthening our value proposition to our Business Partners. Customer Centricity is key.

One such way is by means of thought leadership. In the summer of 2016, we were pleased to partner with the renowned Dr. Schanz, Alms & Company AG in Switzerland to produce a research paper entitled “The Changing Global Energy Landscape: Opportunities and Challenges for Energy Underwriters”. Here is a look at the key themes of the paper, as well as the growing importance of sound Enterprise Risk Management (ERM) practices. The latter are especially relevant given the very real threat of emerging risks such as terrorism and cyber.

Global energy demand by source, sector and supply

A number of factors, including economic, political, technological and societal, determine the development of the global energy market. Today’s largest oil consumer, the United States, will see its oil consumption decline by about 25% until 2040, due to higher efficiency standards for passenger as well as heavy duty vehicles. In contrast, India’s demand for oil will rise strongest, followed by China.

World oil production is predicted to grow by 15% - 30% until 2040, depending on the source of research and the underlying scenario applied. Other than oil, all sources for electricity generation are projected to increase, including nuclear. For the foreseeable future, fossil fuels will remain the dominant source of energy.

An overview of global energy and power insurance markets

In upstream energy markets, from 2014 to 2015 alone, premium volumes have dropped from about US$3 billion to $2.3 billion; at the same time, overall losses whether insured or not, have risen. Likewise, in the downstream sector premium volumes are being eaten away fast, as a result of abundant capacity and increasing reliance on captives. Contrary to the upstream sector, however, losses recorded in downstream are much less.

Volatile oil prices have impacted the upstream and downstream sectors differently. In the former, an increasing number of clients have opted for lower programme limits and higher self-retentions despite the fact that the decline in oil prices has reduced the scope for a “natural” hedging of exposures. Whereas in the latter, the contrary is true: the sharply reduced cost of feedstock has boosted refiners’ margins, with business interruption values up accordingly.

Further consolidation is very likely given the current turmoil affecting the global oil and gas industry, implying that the demand for energy insurance capacity will come under additional pressure.

A changing risk landscape

Sound Enterprise Risk Management (ERM) practices are a further way in which reinsurers can add value to stakeholders. The risk landscape is changing fast, presenting both challenges and opportunities.

With reference to the energy sector, technological progress is of particular relevance. One example is the rise of subsea drilling, as opposed to traditional platform-based field drilling. Statistics reveal that such completions operate relatively smoothly after the initial installation. In addition, they are economically advantageous and offer environmental benefits.

Another relevant trend is risk concentration. It presents major underwriting challenges in most areas of energy and power insurance. A further development to monitor is supply chain risk, as exemplified by the Tohoku earthquake, the Thai floods and the Tianjin blasts.

Emerging risks: Terrorism and cyber

By now, terrorism has become a global phenomenon. Although particularly highly concentrated in a few countries, it is spreading to more. Terrorism continues to be a threat with the resulting growing need for, and uptake of, terrorism and political violence insurance by businesses as a risk mitigation measure. Trust Re provides Terrorism & Political Violence cover as part of its Specialty Lines reinsurance offering.

Cyber-attacks are placed within the top ten global risks in terms of likelihood and have become increasingly relevant for many companies, especially due to the growth in use of cloud computing, social media and big data. The energy sector is certainly not immune to the threat of terrorism or cyber-attacks.

Against the backdrop of a rapidly changing operating environment in the energy sector, those who embrace the opportunities of ERM as both a risk mitigation measure and value-added proposition are those most likely to weather the current storm. The same is surely true for the non-energy sector.

Growth, growth, growth

Those were the three keywords at yesterday’s City Reports by the chief delegates of the 12 member cities of the EAIC. The fact that Asia is growing economically is nothing new, but the numbers shared yesterday spoke volumes of the potential lying latent in the insurance industry.

Each of the 12 member cities reported respectable growth in both life and non-life sectors, as well as not-inconsiderable growth in insurance penetration numbers, as eachchief delegate briefly shared the current market conditions and some future plans in their respective markets.

Even Indonesia, which had seen sluggish economic growth in the last two years, was able to report a 12% y-o-y growth in gross written premiums, for both the life and general insurance sectors. Cambodia, the smallest market amongst the 12, reported a massive 40% growth in gross written premiums for the general sector, and a 240% increase in premiums for the life market (bearing in mind that life insurance in Cambodia has only existed for a few years).

The Philippines boasted a 7% growth in their GDP in 2015, making them the fastest growing member, and in the same year also recorded a premium growth of 18.8% in life, and a 7% increase in general insurance premiums. This same success has them aiming for an insurance penetration of 3% of the national GDP by 2019 (up from the 2% it currently stands at).

Much of the growth for the general insurance field was driven, unsurprisingly, by motor insurance, most of which is mandatory in most markets. Standouts include Brunei, Thailand and Taiwan, where motor insurance accounted for at least 50% of the general insurance pie.

Within the life insurance sector, bancassurance proved to be a strong avenue of distribution, coming close to matching the efforts of the many life insurance agents that work across the region.

Always forward

Much of the growth in the region was catalysed by government and industry initiatives to increase insurance awareness, enhance education and improve the perceived value of insurance amongst the general public. Malaysia has recently implemented the Life Insurance and Family Takaful Framework to increase penetration and consumer knowledge, while Japan has introduced several schemes to target the rapidly aging population with great results. Meanwhile, the Philippines insurance industry is developing a curriculum aimed at high school students to educate them on the value of insurance.

Japan’s measures to protect their elderly population – by 2040, it is estimated that one third of the population will be aged 65 and above – include service guidelines for the elderly implemented by the Life Insurance Association of Japan (LIAJ) and the General Insurance Association of Japan (GIAJ), rebranding life insurance as an inheritance tax-saving measure and an increased emphasis on healthcare and nursing care.

These initiatives have proven to be successful in capturing this rapidly growing market segment (a segment that is also steadily growing in other parts of Asia, such as Hong Kong, Thailand and Singapore), with 19.6% of all life insurance policies being held by citizens aged 60 and over.

Laying the groundwork for the future

While Japan focused on its elderly, the ASEAN nations set their sights on cultivating their youth. Chief delegates of Singapore, Hong Kong and Malaysia spoke of youth internship programmes and their success in attracting and grooming the next generation of insurance talent.

Besides the education curriculum being developed in the Philippines, the Malaysian industry also innovated with the Youth Video Awards, capitalising on social media and video-sharing site Youtube to capture the attention of an entirely fresh and new customer-base.

Malaysia is not alone in utilising technology. Hong Kong, already well known for its strong FinTech presence, set up a task force in September 2015 to further promote mobile and digital technology, with insurance being one of the industries set to benefit.

Taiwan’s FSC is also looking at implementing policies to develop a FinTech business model, as part of their long-term strategy to increase insurance penetration, and Macau is following closely on their heels.

Further, Korea, already the most connected city in the world, are poised to take advantage of their infrastructure to improve data collection and adapting the industry to technology and social media developments.

Impact of the Zika virus

“Batch” claims all over US$10 million each are a hypothetical worst-case scenario but worth consideration nonetheless. Ms Kristen Kenst, AVP, Healthcare Underwriter for North America – Healthcare Division, Allied World, discusses insurance risks and risk management strategies in coping with the Zika virus.

Although there is much that is still unknown about the Zika virus, which is spread primarily by the Aedes species of mosquito to humans primarily through infected insect bite, the early research does not leave much room for optimism. In fact, top US health officials have stated that the Zika virus, and its link to birth defects and neurological disorders, is worse than they originally suspected. Given this information, we can anticipate that the strain on healthcare facilities will be significant.

The front line diagnosticians (primary care physicians, OB/GYNs, emergency room physicians, etc) have the first opportunity to identify patients who have been exposed to the Zika virus. The Centers for Disease Control (CDC) in the US has produced testing algorithms related to pregnant women who have travelled or who reside in an area with Zika, as well as for infants who may have been exposed to the virus. And with the recent discovery of an “almost certain” link to Guillain-Barré syndrome, these clinicians need to be mindful of the signs and symptoms of that rare condition as well.

We can also anticipate that there will be an additional strain on laboratories as healthcare providers order blood tests to look for Zika. The CDC has a permanent lab set up in Puerto Rico, and recently has begun importing staff and equipment to conduct 100,000 blood tests a year (which is five times as many as it can do now). It is unclear whether this will even be enough, as top officials predict that over the next year more than four million people could be infected, but it is a start. All Zika testing is to be coordinated through the CDC, and the Federal Drug Administration has issued an Emergency Use Authorization (EUA) for a diagnostic tool for the Zika virus that will be distributed to qualified laboratories and, in the US, those that are certified to perform high-complexity tests.

Insurance risks linked to Zika

Although the current focus is on research and prevention of the Zika virus and the health risks it poses to the population, we should also consider the risks it could pose to the business side of healthcare.

In the medical malpractice world, there may be claims for wrongful birth due to failed or inaccurate tests performed during pregnancy. The average cost of caring for one child with birth defects can be over US$10 million. There could also be claims alleging failure to diagnose where the damages could be equally severe. And what role might “batch” claims play in this scenario? Thirty claims all over $10 million each would exhaust most insurance towers.

These are admittedly hypothetical worst-case scenarios, but are worth consideration nonetheless. They also highlight the need for accurate and timely testing, which in a situation where the volume of ordered tests outpaces the labs equipped to handle them, can be precarious at best. As CDC director Thomas Frieden has said, at some point Zika cases will increase “not steadily, but dramatically.”

Healthcare facilities will also want to be mindful of their business continuity plans. And though many organisations purchase business interruption insurance, coverage for lost revenue arising out of a nonphysical damage event (such as a quarantine of facilities or medical professionals) may not be available on some business interruption coverage forms

Risk management strategies for Zika

In talking with some of the most sophisticated healthcare organisations about their approach to managing the Zika virus, it is evident that it is still early stages even for them. Thus, at this time, the risk management strategies for Zika are not unlike those for other pandemics. This may change as we continue to learn more about Zika.

In most healthcare organisations, pandemic preparedness is managed through an infection control plan. It is vital that an organisation’s infection control specialist have a close working relationship with the local health department, as they will be the first to receive information from the CDC about the early identification and management of any widespread disease.

For individuals, the focus must be on limiting exposure to areas with mosquitoes that are known to spread the Zika virus, wear long-sleeved shirts and pants, and use appropriate insect repellents. According to Mr Frieden, “There is nothing about Zika control that is quick or easy. The only thing quick is the mosquito bite that can give it to you.”

Insurers of tomorrow

The industry has historically been plagued with low customer engagement, which means a lack of data with which insur- ers can build customer insights and fulfil consumer needs, said Mr Hendry Yoga, Director and COO of Astra Insurance at yesterday’s plenary session on Customer Centricity. However, the digital era has helped a lot in that regard, with advancements in mobile and communication technology and customers’ eager adaptation of this technology.

The panellists discussed the various ways the industry could adapt its business model, product design and marketing strategies to approach this ever-evolving breed of customer. Mr Scott Ryrie, Commercial Director Asia Pacific at A.M. Best Asia Pacific, noted that while there were many efforts to grab the customers’ attention with better product design, innovative marketing and digital engage- ment, not much airtime was given to the claims process. Being an important part of the customer experience – arguably the most important part – the claims process needs to cater to the consumer as much as the rest of the value-chain.

Dr Tobias Farny, CEO of Asia Pacific, Greater China and Korea at Munich Re, spoke of his own pain points as a customer who owned property in two different parts of the world. “Why not have the flexibility to adjust premium and exposure if I can prove that the exposure has changed?” he said. “That’s a flexibility that I hope to see in the future. Technology can allow us, in the future, to be more client-centric by being able to change products on a short notice.”

However, such advancements within the industry requires an immense amount of data, which in itself comes with its own slew of challenges. “There’s so much data around, but what part of that metadataset do you harness?” said Mr Ryrie.

Mr Ramon Yap Dimacali, President and CEO of FPG Insurance, said that there was a different problem with data in the Philippines. Due to slow internet speeds, collecting data online was a challenge. However, the solution lies in other parties who own that data. “Re- mittance companies, banks and cooperatives, they have the exact data we want, because they’re the ones who deal with the money.”

“We cannot own all the data, so we must partner with the people who have the data we need,” he added.

Creating customer profiles

Even with the data, an insurer will still be unable to engage with the customer if that data isn’t utilised in the correct way. Ms Candy Yuen, CEO of HSBC Insurance Asia Limited, shared the comprehensive method HSBC used to improve customer centricity of their life insurance business in Hong Kong.

Starting with analysis of quantitative data on customer behaviour and attitudes, they moved on to segmenting their customers based on demographic attributes. Delving further into their data within each segment, they created customer personas to better understand a customer’s thought process and identify his needs.

The exhaustive process helped HSBC create new products and services, pushed through the right channels to reach the right segments, using the right type of advertising and marketing.

Avoiding superficial engagements

The industry has typically used rational arguments in their marketing, com- bined with a focus on the technical aspects of the product, leading to the myth that insurance is confusing and complex. “We all have a responsibility to dispel this myth,” said Ms Yuen.

Lately, insurers have been adopting a more emotion-based approach in their marketing. However, these “emotion-plays” have not quite been translated to customer engagement, and some of them fell into the trap of being superficial – “emotive branding and videos”, as Ms Yuen pointed out.

Ms Yuen also noted that the industry had classically been “event-driven” in their consumer engagement efforts, targeting customers based on sig- nificant life events such as critical illness or starting a family.

She suggested that insurers shift gear and adopt a “change-driven” model. “Change in any aspect of life is able to disorient and cause some level of distress. If insurers are able to provide a solution during a stage of transition for customers, we can perhaps develop a more long-lasting and emotive relationship with our customers,” she said.

All of these attempts to engage with the customer is predicated on the fact that the industry knows who the customer is. With the internet and everyone being connected on a global level, customer perspective is widening, said Mr Dimacali. “The customer is changing because of technology, because of behaviour, because of experience, and the industry needs to follow suit.”

Awareness on cyber security still lacking

Promoting better data security amongst corporates in Asia should be an area of advocacy for insurance companies to help mitigate the risk of cyber crime, said panelists at yesterday’s plenary session on cyber fraud and crime.

“Many companies have not looked hard enough at data security and integrity because they believe the IT department have things covered through encryption and anti-virus. That is not enough to secure you, so we need to move to data security at both the insurance level and in corporate boardrooms to better understand this underlying risk,” said Mr David Piesse, Chief Risk Officer, Guardtime.