Ferrying FAIR to the New World

This 25th FAIR Conference has a punchy yet ambitious theme of “Insurance Transformation”. Can FAIR seize the challenge to make that leap to be a global force? Can it reach greater heights in line with the FAIR markets accounting for almost 20% of global premium pie?

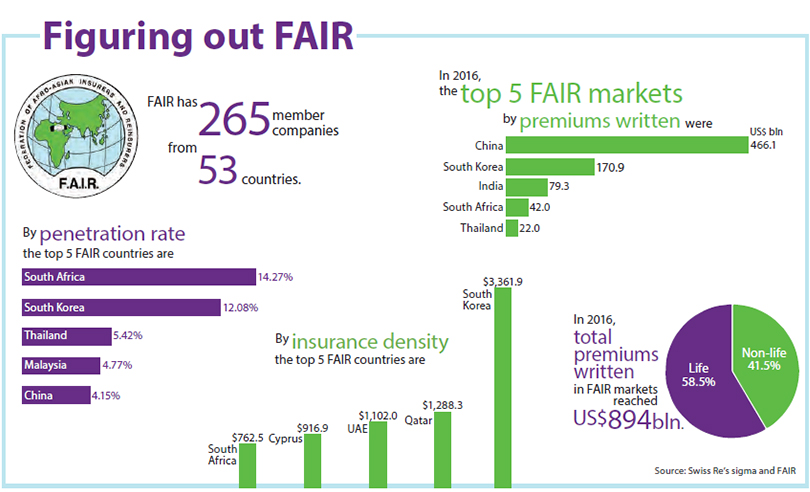

FAIR still has more political mileage and clout than actual business on the ground, though the three FAIR Pools and one Syndicate together account for a significant figure of just less than half a billion dollars in premium.

The float of political goodwill

FAIR has wide appeal. Each biennial conference still draws in the numbers, attesting the importance attached to FAIR be it in Asia, the Middle East or Africa. This year, despite the regional and global geopolitical tensions and the tough business environment, some 800 delegates will turn up in Bahrain. Interestingly in its 53 year-history, this is the first time that a FAIR Conference is being held in a GCC market where Secretary General Adel Mounir says almost 50% of FAIR members are from the Arab World – another draw for this FAIR.

FAIR has tradition, culture, and diversity. Aside from its obvious advantages – the power of meeting and networking – the real belief in FAIR is the cardinal quest for effective regional co-operation even in the era of globalisation. The various Pools and Syndicate are concrete achievements of that golden FAIR dream that one day the FAIR markets representing more than two thirds of the world’s population will actually come together to be a force to be reckoned with in any insurance arena.

Will it happen? Will transformation take place? What will be the catalyst for this big leap? Is technology the answer? Can FAIR ride the tiger of disruptive innovation to make heads turn?

The tech speed boat

Insurance, being data-intensive and data-sensitive, has been a natural draw to technology that has the means to make sense of Big Data and to even use these data to teach machines. From disruptors, InsurTech start-ups are evolving to be essential complementary partners to insurance. But unlike start-ups that can jump in to make changes whimsically, established firms have massive legacy issues, and they cannot make lemonade of their business with one squeeze.

So how can FAIR come in to help the members? Can FAIR serve as the trusted common supporting services hub for its members where data can be exchanged and used freely? Can FAIR provide the vital security and checks needed to protect data? Can they keep the hackers away?

In technology, the regional grouping will get global. Technology knows no barriers, and it is unstoppable.

The new Uber drivers

As always there are more questions than answers, but they set the direction for the winds to blow when one seeks transformation. FAIR, with its tech-savvy young workforce, perhaps already has the necessary talent to start this drive to digital transformation. Invest in new talent, and let them lead.

Though the journey is long, perhaps in Bahrain, marking FAIR’s 25th Conference, the Federation should take a pledge to get a leader to spearhead the “transformation”. Any takers?

The real appeal: Dollars and cents

At the end of the day, the real appeal of FAIR is the reality that there is business to be exchanged and money to be made. There must be awareness that there is an advantage going the FAIR-way be it through business exchanges or training. Membership must have real privileges that members need and want. Joining FAIR is for mutual rewards and not just to be part of the grouping as a CSR in the name of helping the regions.

Lastly, doing it the FAIR-way must be able to stand up to world standards too.

That is what the transformation should be about. FAIR is still growing: 10% growth this year to a presence in 53 markets says the Sec-Gen. So land ahoy!

Welcome to Bahrain!

“It is a great source of pride for me to see the large number of guests coming to Bahrain this year. The 25th FAIR Conference takes place at a critical stage of the Afro-Asian and global insurance industry where providers are required to adapt to the fast-paced technological change and be able to cope up with the accompanying socio-economic trends. Therefore, and in our goal to remain abreast with the global norms, we gave a special attention to the technological era we are going through nowadays as reflected in our conference theme “Insurance Transformation in FAIR-Land”.

We are positive that with the accumulation of experiences this Conference brings together, we can come up with a better perception of how to take advantage of technology and overcome its challenges for the benefit of our Afro-Asian insurance societies.

I look forward to this unique experience and am positive that the outcomes will add value to our industry.”

Dr Adel Mounir

Secretary General of FAIR

“FAIR has always been close to my heart ever since I joined the insurance industry many years ago. As an Egyptian, and with FAIR’s General Secretariat headquartered in Cairo, I always felt that we have an instrumental role in ensuring the continued success of this organisation and that Egypt is indeed ideally positioned, geographically and culturally, to bring the two great continents of Africa and Asia closer together.

The past six years have given me a real opportunity to actively contribute towards the operations of FAIR. I was President of FAIR between 2011 and 2013, followed by two years as Vice President and in 2015 Egypt, once again, hosted the FAIR conference and celebrated the 50th anniversary and I was honoured to become President for a second term.

As President, I focused on coordinating with and empowering the General Secretariat to achieve the FAIR goals. Achievements worth highlighting include amending FAIR’s statute and bylaws, in particular, the constitution of the Executive Board to ensure a more equal and balanced representation of the member countries and our two continents. We have also agreed the forming a Steering Committee to serve for the remaining period of the Executive Board.

I thank all members for their continued support and urge them not to forget the importance and unrealised potential of this organisation that could and will achieve much as long as the members dedicate their time and efforts. Finally, I wish Bahrain and FAIR’s new President, Mr Yassir Albaharna, a successful two years.”

Mr Abd El Raouf Kotb

Outgoing FAIR President

Have a fruitful FAIR in Bahrain

“Bahrain has always been a pioneer in several initiatives in the Arab world, and hosting FAIR Conference for the first time in the GCC is another noteworthy milestone.

Beside being a base for regional branches of many international reinsurers, Bahrain is home to two of the reputable and highly rated reinsurance companies, namely: Arab Insurance Group (Arig), and Trust International Insurance and Reinsurance Company (Trust Re). Bahrain is also home of one of the Federation established entities: FAIR Oil & Energy Insurance Syndicate. The reinsurance sector generates in total more than US$1 billion.

This event is the first conference of FAIR ever to take place in the Gulf region. We are proud and honored that Bahrain, our friendly island was chosen to be the venue of this conference, which is one of the most widely attended conferences in the Afro-Asian region. Furthermore, Bahrain is a perfect destination to mix business with pleasure. So during your stay, you are invited to explore the country’s rich heritage from the remains of the ancient Dilmun civilisation and cultural cities to the modern malls, the vibrant souks and entertainment.

The Organising Committee has made great efforts to ensure for our 800 guests from 62 markets to benefit from this special occasion and take advantage of the facilities the Conference provides as an efficient platform to build new relationships and further strengthen their business ties.

Welcome to Bahrain, and we promise you an unforgettable fruitful experience.”

Mr Nabil Hajjar

Chairman of the Organising Committee, 25th FAIR Conference

Disruption of insurance? Don’t get carried away

Dr Kai-Uwe Schanz, Chairman of Dr. Schanz, Alms & Company cautions against the disruption debate raging across the global insurance landscape taking on a life of its own, and says it’s time to pause and recap a few facts.

This is a slightly contrarian piece as it pours some cold water on the disruption hype that appears to have taken hold of the global insurance community.

Let us start with the ubiquitous notion as such. “Disruption” is worn out to an extent that any clear meaning has all but evaporated. In addition, it is not new and hardly different from Joseph Schumpeter’s definition of “capitalism”, coined in 1942, as a permanent process of “creative destruction”. Many proponents of disruption may never have heard about Schumpeter but will certainly take note of Jeff Bezos’ view: “At Amazon, we’ve had a lot of inventions that we were very excited about, and customers didn’t care at all. And believe me, those inventions were not disruptive in any way. The only thing that’s disruptive is customer adoption.”

Effective guide to change

For insurance executives who have to perform the art of the possible, this approach may serve as a more effective guide to change than fancy consulting mantras.

In the context of disruption, technologists immediately refer to Airbnb and Uber which are shaking up and fundamentally threatening the travel accommodation and taxi industries.

Despite the dramatic changes brought about by Big Data, the Internet of Things, autonomous cars and peer-to-peer (P2P) insurance, for example, the insurance industry is unlikely to be prone to disruption as defined by the technology industry.

6 reasons the insurance industry is unlikely to be affected by disruption

- Insurance customers are buying contingent rights to access cash frequently in situations of severe distress. It goes without saying that the scope for disrupting this business model is fundamentally different from transportation or temporary accommodation.

- Insurers already embrace many innovative technologies in order to enhance each and every link of their value chain. This includes the formation of non-actuarial, Big Data teams using various non-traditional predictive models. Kept in perspective, digital technologies are a great opportunity for innovation, rather than a source of disruption.

- Insurance requires massive amounts of capital to cover catastrophic scenarios. It is hard to see how P2P insurers, for example, would be able to build the level of scale needed to accumulate capital and use it efficiently. Such startups will inevitably be reliant on reinsurance for wholesale backing, literally. As such some of them look like brokers with uninspiring long-term profitability prospects.

- An online only insurance customer relationship may not survive critical situations arising from (major) claims payments or the sudden emergence of complexity requiring human interaction. Removing any alternative option for interaction may backfire.

- The rise of autonomous vehicles would shift risk from personal lines to commercial lines. Whether overall risk pools and the associated premium volumes will ultimately shrink is debatable and not predictable. Certain heavy personal lines motor insurers would face tremendous pressure to adapt – with many years available to do so – but probably not outright disruption.

- Regulators may simply kill any “disruptive” venture as soon as issues around customer protection or perceived unfair price discrimination emerge, which could be only a matter of time. This is a valid scenario, especially in politicised and fragmented regulatory environments such as in the US.

Full-blown transformation

Even if insurance avoids disruption in its literal sense, there is no doubt that it will (have to) undergo a full-blown transformation. There will be no alternative to a fully digitised value chain. And there will be no alternative to partnering with companies that originate and analyse real time data or provide superior customer access.

Once the respective strategies are in place, insurance executives should keep their minds firmly focused on what will remain the key performance indicators: underwriting margin and customer retention.

Golden jubilee celebrations at 2015 FAIR

The 24th Conference of FAIR celebrated the organisation’s golden jubilee at its birthplace in Cairo with the theme of “Building on 50 Years of Regional Cooperation”. Giving the opening speech, Mr Ashraf Salman, Egypt’s Minister of Investment, called on Afro-Asian markets to cooperate through legislation and regulatory reforms. He also urged the larger markets to support the smaller ones in the region. The Conference, held from 12 to 14 October 2015, attracted over 850 delegates, representing 300 companies from 51 countries.

First FAIR in the GCC opens amidst much fanfare

Bahrain made history yesterday as the first-ever GCC country to host a FAIR conference. Held at the ornately decorated Gulf Convention Centre, the opening ceremony of the 25th FAIR Conference was an impressive affair.

The Conference, with the theme “Insurance Transformation in FAIR-Land”, held under the patronage of HRH Prince Khalifa Bin Salman Al Khalifa, Prime Minister of Bahrain, was inaugurated by HE Rasheed Al Maraj, Governor of the Central Bank of Bahrain.

Tech innovation for edge in volatile world

In his opening address, Mr Nabil Hajjar, Chairman of FAIR 25th Conference organising Committee-Bahrain 2017, said that technology sweeping the insurance landscape today will define its future tomorrow. He was confident that the FAIR platform would provide participants insights and solutions to remain competitive in the volatile economic, political and technological environment.

Adopters of tech will emerge as winners

Mr Abd El Raouf Ahmed Kotb, outgoing President of FAIR, in his welcome address, spoke about the challenges that the reinsurance sector is facing globally, especially in the FAIR region.

He said the theme of the 25th Conference is very relevant as the technological advancements of today bring real opportunities, and only those who utilise these technological innovations will emerge as winners.

Glaring talent crunch needs to be addressed

In his industry keynote address “Propelling FAIR Insurance Industry through Innovation”, Mr Michael J Morrissey, President and CEO of International Insurance Society, touched on two important aspects: better customer experience through the use of technology and attracting and developing young talent for the insurance industry.

Elaborating on the second aspect, he said: “At the heart of every major FAIR issue – market development, customer centricity, Insurtech, capital management, product innovation and others – is the urgency of regional talent development.” The insurance industry, across the globe today, has a glaring talent crunch, which needs to be addressed.

Mr Morrissey said the industry needs to communicate more with both its customers as well as its current and prospective employees, especially if it wants to remain relevant in the changing landscape.

Economic and societal value of insurance

The international address delivered by Ms Anna Maria D’Hulster, Secretary General & Managing Director, The Geneva Association, focused on promoting the economic and societal value of insurance. She said the Association is currently focused on four programmes which include financial stability and regulations; extreme events and climate risk; global ageing and cyber innovation. “These issues that matter equally to the society and the insurance industry will lead to win-win solutions for all stakeholders,” she said.

The 25th FAIR Conference has been jointly organised by Arab Insurance Group (Arig) and Trust Re in collaboration with the Central Bank of Bahrain (CBB) and Bahrain Insurance Association (BIA). About 800 delegates from 62 Afro-Asian countries and globally are attending the three-day event.

A quick survey of CEOs’ top concerns

Q: What do you think is the most pertinent issue insurance CEOs need to address today?

“Keeping pace with digital transformation that impacts nearly every aspect of insurance today is becoming increasingly critical. From automating distribution, customer service, policy operations, data analytics and pricing, the technological demands are fervent and bring with it constant learning and system calibrations. But it also brings about innovation, like mobile apps that bring our customers closer to the solutions they need, or the use of drones for quicker aerial property risk surveys.”

Mr Christos Adamantiadis, CEO, Oman Insurance Company

“Building a stronger regulatory framework is the hottest topic in our sector nowadays. Indeed, new laws and regulations strengthen the regional insurance mart making it more resilient in a volatile business environment. The protection of our sector, especially in our region, is crucial given the economic, financial and political circumstances reigning in MENA countries. Regulators’ insights and companies’ strategies go hand-in-hand when it comes to the sector’s main goals of profitability and shareholders’ interests. In a highly competitive market, insurers must aim for a smart underwriting policy combined with an innovative high-tech customer-centric strategy both driven towards profits and growth.”

Mr Fateh Bekdache, Vice Chairman & General Manager, AROPE Insurance SAL

“A key challenge CEOs face is the ability to grow successfully their companies’ profile, whilst maintaining or improving earnings in a competitive, volatile and uncertain market environment. Continued pressures from shareholders to achieve enhanced returns in an overcrowded market where rates have softened also create a real dilemma for CEOs, who must balance the desire for market profile over profitability. We believe that adopting appropriate market strategies and risk practices remain essential to the future success of (re)insurers.”

Dr Roger Sellek, CEO, EMEA & Asia Pacific, A.M. Best

“The Middle East insurance markets are going through a four-pronged disruption, which is originating from: increasing customer expectations, regulatory changes, technological advancements, and economic pressures due to lower oil prices. Whilst we see pockets of growth, how individual insurers respond to these emerging challenges, will define the future leaders of the business.”

Mr Sanjay Jain, MENA Insurance Leader, EY

GIC Re and FAIR: A time-tested relationship

In this exclusive interview, Mrs Alice G Vaidyan, Chairman-cum-Managing Director of GIC Re, shares her views about the FAIR market, the protection gap in FAIR member countries, while touching on GIC Re’s performance, plans and strategies.

In 2016, among Asian reinsurers, growth was primarily driven by GIC Re, according to A.M. Best’s Global Reinsurance Review 2017 which features world’s Top 50 reinsurance groups.

In the global rankings of reinsurers released at Monte Carlo in September this year, GIC Re was ranked 12th, a two-spot improvement over the previous year. It has also emerged as the third-largest reinsurer in Asia. GIC Re also shares the distinction of being a founding member of FAIR.

Commitment to FAIR

GIC Re, the manager of the FAIR Nat CAT Pool, has been a leader on various treaty and facultative business accounts in the Afro-Asian markets.

In addition, GIC Re is a member on the technical board of FAIR Aviation Pool and is a significant aviation underwriter globally.

Mentioning the company’s long association with FAIR, Mrs Vaidyan said: “GIC Re has always been committed to FAIR. Our initiative to establish the FAIR Natural Catastrophe Reinsurance Pool is an example of this commitment.”

Africa, a benign CAT market

Traditionally Africa has been considered benign as far as CAT risks are concerned, and the region has significant over-capacity. However, perhaps due to the impact of climate change, the CAT market has picked up, with the region seeking increased CAT reinsurance support.

In 2016, Asia suffered 47% of the total global economic losses from Nat CATs, while its insured losses accounted for only 16% of total global insured losses.

Referring to the low insurance penetration in most of the member nations of FAIR, Mrs Vaidyan said that though reinsurers have a duty to help insurers introduce affordable products in their respective markets so that the penetration increases, they also have to ensure the sustainability of the industry. “GIC Re has always been a market-friendly reinsurer, and we will continue to further enhance that image,” she said.

GIC Re’s IPO

Speaking about GIC Re’s impending IPO, Mrs Vaidyan said: “Going public will bring more visibility, transparency and accountability to our functioning, in addition to improving corporate governance and risk management in the organisation.” She added that the IPO will unlock value for the company’s existing shareholders.

Agriculture boosts GIC Re growth in 2016-17

Crop insurance has emerged as one of the largest portfolios of GIC Re, said Mrs Vaidyan. The reinsurer posted an 82% growth in its overall gross premiums in FY17 compared to FY16, on the back of the Pradhan Mantri Fasal Bima Yojana (PMFBY), the government-backed crop insurance scheme.

The reinsurer’s net profit grew by 10% for the financial year ended 31 March 2017. It posted an after-tax profit of INR31.27 billion (US$480.8 million) in FY17 compared to INR28.48 billion posted in FY16.

Enlarging footprint

On the expansion front, the Indian reinsurer wants to have a presence in virtually all geographies.

“Our growth plans include establishing a syndicate at Lloyd’s of London and gradually expanding our relationship with US insurers and venturing more into that market,” said Mrs Vaidyan.

The Moscow representative office of the company will be converted to a subsidiary, while new representative offices will be established in China, Brazil and Bangladesh to exploit the potential of those markets, said Mrs Vaidyan. A strategic relationship in the area of reinsurance with Myanmar is also on the anvil.

In addition, GIC Re is planning to strengthen its life reinsurance capacities and is also focusing on cyber and liability lines.

An overview of India’s non-life insurance industry

These are interesting times for the Indian insurance industry. Several Indian insurers are poised to go public, and work is in progress for these insurers to be listed on bourses.

The sole Indian reinsurer in public sector, GIC Re is to be listed very soon.

Record growth in 2016-17

The non-life industry closed the fiscal 2016-17 with a gross premium income of INR1.27 trillion (US$19.5 million), registering a growth of over 33% over the previous fiscal 2015-16. This record growth was achieved largely on the back of government sponsored Prime Minister’s crop insurance scheme.

The beginning of the year also saw the India branches of major overseas reinsurers, including Lloyd’s, commencing their operations on-shore. This translates into more capacity, better products and improved insurance penetration in the country.

Association welcomes FAIR to Bahrain

Bahrain Insurance Association hosted an outdoor welcome reception on the first night of the Conference at the beautiful garden of the Gulf Hotel. After a long day of meetings and networking, guests appreciated the chance to relax and socialise under the moonlight, enjoying good food and drinks, while a violinist seranaded the guests.

Risk landscape to be shaped by urbanisation and digital revolution

The current global risk scenario has two main features - urbanisation and digital revolution, said Mr Cameron Murray, Head of Middle East & Africa, Lloyd’s of London, in his guest address.

Urbanisation

Urbanisation, while improving human life on several counts, is also concentrating high-value assets in cities, and this can result in a risk-management challenge. Today, cities are exposed to three kinds of threats: man-made, natural and emerging threats. Such a huge concentration of risks makes cities highly vulnerable.

According to a Lloyd’s study of the 301 cities globally, total GDP concentration is around US$4.56 trillion. Man-made threats alone account for around $2.13 trillion worth of GDP at risk in these cities.

Digital revolution

Digital revolution is something that is mind boggling, said Mr Murray. According to market statistics, every day we create 2.5 quintillion bytes of data. In 2016, global mobile subscriptions numbered 7.4 billion. All these would have a significant impact, especially with the rapid changes taking place in the needs and expectations of customers.

Cyber crime

The cost of cyber crime is predicted to hit $2 trillion globally by 2019 and, though the awareness of cyber risk is increasing, it is very gradual and not fast enough. In addition, it has both visible and hidden costs. Presently, the insurance industry is expected to protect digital and physical assets of the insured. Products need to be delivered in ways that are efficient, low cost, dynamic, smart and flexible.

Technology will drive solution

Mr Murray said solutions for such problems will increasingly be technology driven. It is already happening in the use of data and algorithms, eg, comparison websites and telematics in motor insurance.

InsurTech & disruption

Speaking on Insurtech and the dawn of the disruptors, Mr Murray said InsurTech would fundamentally change the way insurance is sold, claims are assessed and risk is commoditised. It would make distribution more streamlined and cheaper.

Mr Murray emphasised the need for ensuring that the talent and recruitment programme of the industry prioritise diversity and inclusion, and promote innovation to enable the industry to get closer to its customers.

Opportunities & the way ahead in FAIR

Afro-Asian economies have achieved healthy growth in the last decade, especially in sectors like petrochemicals, infrastructure and telecommunications where there was significant progress, said Mr Abdul Rahman Al Baker, Executive Director-Financial Institutions Supervision, Central Bank of Bahrain, in his special address.

Consequently, the insurance industry in these countries has experienced steady growth on the back of this tremendous economic development, improved regulatory environment, and increased public awareness.

Compulsory health insurance & takaful lead growth

Growth in the GCC insurance industry has quadrupled between 2006 and 2016, with premiums rising to US$26 billion at the end of 2016 from $6.4 billion in 2006, said Mr Al Baker.

“One of the major force behind the industry’s growth in recent years has been the implementation of compulsory health insurance schemes in various jurisdictions, as well as the outstanding demand for takaful products which create strong growth avenues for insurance companies in the region,” he said.

New products need of the hour

There is significant demand for a range of insurance products - from health, life, agriculture, property to catastrophe covers.

Therefore, insurance regulators in Afro-Asian countries need to ensure that the insurance market remains stable and continues to strive and prosper in these economies.

Regulations must keep pace with developments

Mr Al Baker said it is important that regulations be dynamic, up-to-date with market changes and in line with international best practices, so that the balance between proper regulation and market development is maintained. Regulations also need to encourage the development of new lines of insurance business like takaful, captives and microinsurance, he said.

Education vital for qualified talent

Mr Al Baker also called upon the insurance industries in Afro-Asian countries to build the talent base through offering multi-facetted insurance education in universities and private training centres. This will guarantee the necessary supply of highly qualified talented personnel to meet the growing demands of the market and regulatory authorities in these countries.

InsurTech to reach out to new digital customers

Although the global insurance sector is on the brink of a major disruption, Mr Al Baker noted that very few insurers in Afro-Asian countries are putting InsurTech as a top priority in their corporate strategies.

Consumer habits are evolving rapidly, and more and more clients expect insurance offerings to cater to their specific needs. InsurTech can be the facilitator to meet these needs, and if insurers do not urgently incorporate InsurTech into their core strategies, they risk going out of business.

Plenary Session I:

Regulatory challenges in FAIR-Land

The burden of compliance and the complexity of regulations is growing very rapidly, said Dr Kai-Uwe Schanz, Chairman and Founding Partner of Dr Schanz, Alms & Company AG and Member of the Board of Directors, Trust Re. Dr Schanz chaired the first Plenary Session on regulatory dynamics.

Risk-based solvency implementation a challenge

It would be a big challenge for the Indian insurance industry to move to a risk-based solvency regime, said Mr P J Joseph, Member (non-life), IRDAI. Risk management in India is very different compared to that of other insurance markets, he said. This is especially true for the recently introduced crop insurance scheme.

Another major challenge is that though the infrastructure and other industries are growing, insurance penetration is a growing but not at the desired pace. There is still a large challenge as far as the protection gap is concerned. The only consolation is that insurance coverage is certainly growing through several government-sponsored insurance schemes in both life and non-life categories.

Strong mechanism for protection of policyholders’ interest

The next panelist Mr Hassan Boubrik, President, Supervisory Authority of Insurance and Social Welfare (ACAPS) of Morocco said while the Kingdom has made significant progress in the spread of insurance awareness, it still faces three major challenges. These include the implementation of risk-based solvency regime, development of a strong mechanism for protection of policyholders’ interest, and the overall growth of the Moroccan insurance market.

Mr Boubrik said ACAPS lays tremendous importance on corporate governance, customer interest protection and public disclosure regulations.

Challenge in enforcing regulations

Ms Grace Mohamed, General Manager Insurance, The Namibia Financial Institutions Supervisory Authority, said that her country has two major challeges in the form of transition to risk-based solvency regime and how best to bring about consistency in the enforcement of regulations for various financial institutions.

Balancing the interests of policyholders and insurers

Next panelist, Mr Arup Chatterjee, Principal Financial Sector Specialist, Asian Development Bank, Philippines, spoke about the regulatory environment becoming complex and the regulators coming under tremendous pressure to not only protect the policyholders’ interest, but also to ensure the health of the insurers and improve penetration.

Mr Chatterjee mentioned that nowadays the tendency is to shift the risk from the government to the insurers. Though risk management has evolved and is evolving across the globe, much more needs to be done in this area.

He said the area of talent development for the insurance industry has not received the desired attention, and there should be an urgency in this regard on the part of all stakeholders to ensure that talent development is given the top priority.

Need for access to the vulnerable sections of society

The last panelist Mr Oscar Verlinden, Advisor-Access to Insurance Initiative, emphasised the need for providing access to insurance for the most vulnerable sections of society. Mr Verlinden said there should be a mechanism to ensure this.

Plenary Session II: Digital Strategy for Insurance - Product Innovation and Practical solutions

Traditional insurance model challenged by tech changes

The Plenary Session on Digital Strategy for Insurance saw a lively discussion on how the traditional time-tested insurance business model is now being challenged by technological and behavioural changes.

Data analytics and digitised processes are reshaping the insurance market and the industry must quickly adapt to these changes to stay relevant.

“IoT is here already, basic AI is starting soon and Mr Robot will be around in another year,” said Mr Bernd Kohn, CEO, Munich Re, Middle East and Africa. He highlighted the immense scope of the cyber insurance market which he believes will touch $10 billion by 2020. “Cyber insurance will become a game changer to our industry landscape in most product classes,” he said.

Prof Dr David M Dror, Chairman and MD, Micro Insurance Academy, spoke on the need for insurers to reinvent their customer relationship strategies that would ensure fairness and offer an interactive experience to customers of every level.

In a detailed presentation on the healthcare wellness paradox, Mr Zaheer Alli, Head of New Business, Vitality, South Africa spoke on how his company’s wellness offerings are enabling a shared value approach to insurance that delivers value to all stakeholders. “Vitality integrated insurance focuses on wellness and it allows for a completely differentiated insurance proposition and enables a physical manifestation of the brand,” he said.

The panel was chaired by Mr Ronal Klein, Director, Global Ageing, The Geneva Association and included Mr Corneille Karekezi, CEO, Africa Re.

Expectations for 1 January renewals

Reinsurance players weigh in on what the January 2018 renewals would look like.

“This year we have seen typhoons in Asia, eg, Hato, but much more significant was the impact of Hurricane Harvey in the US and the September events: Hurricane Irma, Hurricane Maria and the Earthquake near Mexico City. The retro and reinsurance markets will face significant loss burdens, and we believe there will be a noticeable correction of prices and terms and conditions on a global basis, more so in the more affected markets and treaties.”

Dr Peter F Hugger, CEO, Echo Re

“Although there has been an improvement in the risk management of the cedants following the recent fires particularly in UAE, we cannot say that it helped the rates to increase. There is still plenty of capacity in the region meaning that the soft market conditions will prevail in the upcoming 2018 January renewals.”

Mr Gökhan Aktaş, Head of Department, Foreign Inward Business, Milli Reasurans T.A.S.

“The 1 January property and casualty reinsurance renewals will not be significantly different from the prevailing soft market conditions. Competition is fierce, and it is challenging for insurers/reinsurers to continuously meet the growing expectations of clients. We expect stability in prices and conditions for the treaty renewals, but opportunities await innovative players providing value-added services.”

Mr Khaled Nouiri, COO, Oman Re

“We expect to see minor stabilisation during the January 2018 renewals following the frequency of risk and CAT losses. The pricing pressures will ease but not disappear. Trading conditions remain challenging for market participants due to surplus capital, economic and geopolitical pressures.”

Mr Kamal Tabaja, Group Chief Operating Officer, Trust Re

“Geopolitical and economic situations affect every reinsurer, but I don’t think it will create any hindrance during the renewals in 2018. Historically insurance has bravely faced every kind of crisis and has continued its journey to date. The industry currently faces internal challenges such as a soft-market scenario and is struggling to balance between under-writing and under-rating.”

Mr Manoj Zagariah, Director – Reinsurance, Protection Reinsurance Brokers

Arig Night Out

ARIG hosted a dinner for delegates of the 25th FAIR Conference at the open lawns of the Gulf Hotel. Delegates were treated to an ”international culinary celebration” where cuisines from different parts of the world could be sampled. The FAIR Hall of Fame Award Ceremony was also held during the evening and Mr Atul Boda, Chairman, J B Boda Reinsurance Brokers was inducted into the Hall of Fame. Local artistes performed music and dance after which a “live” band belted out rock-and-roll music much to the delight of delegates.

Quote of the day

“FAIR is a perfect platform for this exciting group to exploit the perfect opportunities the region presents for insurance to grow rapidly.”

Mr Zainudin Ishak

President & CEO, Malaysian Reinsurance Berhad (Malaysian Re)

See you at FAIR 2019 in Morocco!

Morocco will host the 26th FAIR Conference in 2019. The last time the conference was held there was in 2007. Morocco is one of the founding countries of the federation and its state-owned reinsurer Société Centrale de Réassurance (SCR) manages FAIR’s Aviation Pool which was established in 1985.