Welcome to Tokyo!

It is a great honor for us at that the General Insurance Association of Japan (GIAJ) to host the IUMI 2017 Tokyo Conference for the first time since 2006. I would like to express my heartfelt gratitude to all participants coming from around the world.

While this is the 5th occasion for the conference to be held in Tokyo, the year 2017 marks the 100th anniversary of the foundation of the GIAJ. Therefore, it is our great pleasure that the historic and distinguished IUMI Conference is back in Tokyo on such a commemorative year for us.

The common theme of the IUMI 2017 Tokyo Conference is “Disruptive Times - Opportunity or Threat for Marine Insurers?” Under this theme, a lot of experts from a broad range of spheres will deliver presentations and host productive discussions at the workshops. I believe that this conference will be helpful for all participants to confront the difficulties that we are currently facing and will face in the future.

Finally, I hope that all participants enjoy their time in Tokyo, the host city of the 2020 Olympic and Paralympic Games, and one of the safest and most exciting cities in the world.

Noriyuki Hara,

Chairman, the General Insurance Association of Japan

Welcome message from IUMI Secretary General

It gives me great pleasure to welcome you, on behalf of the International Union of Marine Insurance (IUMI) and the General Insurance Association of Japan (GIAJ), to the 2017 IUMI Annual Conference here in Tokyo.

The common theme for this year’s conference is “Disruptive times – opportunity or threat for marine insurers?” and it could not be more fitting given the current market environment. The theme encompasses the recent difficult market conditions and unsettled political environment through which marine insurers must navigate if they are to continue to provide high quality underwriting provision for their clients.

There are major changes under way with cyber attacks, big data, Internet of Things, accumulation of values and autonomous shipping, to name just a few of the challenges we face. Coming together here in Tokyo, a remarkable and beautiful city with a deep-rooted history in marine insurance, is the perfect time to exchange ideas, as well as embrace the emerging opportunities that will inevitably accompany these changes.

As an organisation, we trace our roots back to the late 19th century and an initiative by the German underwriters who, in 1874, formed the Internationaler Transport - Versicherungs - Verband in Berlin. This later became IUMI and its purpose was to create an association “where the members could discuss business matters of common interest”.

Our association has thrived throughout a period of continuous increase in the volume of international trade and consumption; and of constantly improving communications.

Now, 143 years later, IUMI represents 43 national and marine market insurance and reinsurance associations. Operating at the forefront of marine risk, it gives a unified voice to the global marine insurance market through effective representation and lobbying activities.

I hope that you find this year’s conference interesting and thought provoking and please do not forget to have fun and enjoy the wonders and kind hospitality of Tokyo, a city unlike any other!

Lars Lange,

Secretary General, IUMI

Autonomous ships - Redefining the industry?

Capt Jarek Klimczak, Risk Engineer-Marine, Asia Pacific, XL Catlin, Singapore looks at the evolving role of ship captains in the wake of technological advancements and the emerging trend of “autonomous vessels”. How does this impact insurance and risk management?

In the “old times”, the shipmaster was considered “next after God,” because there was seldom anyone else onboard the ship with greater power. The status of the Ships’ Captains has gradually diminished due to changes in the industry and technology. But as the command centre slowly shifts ashore, the question remains whether modern ships still require Masters and crew on board?

Industry observers and several research projects have already acknowledged that autonomous shipping is the future of the maritime industry. The MUNIN (Maritime Unmanned Navigation through Intelligence in Networks) programme, led by Rolls Royce and co-funded by European Commission, aims to design autonomous cargo ships that could be remotely navigated from Shore Control Centre (SCC) by land-based controllers.

Another project called MARS (Mayflower Autonomous Researcher Ship) was also launched early this year, from a partnership of Plymouth University, autonomous craft specialists MSubs and Shuttleworth Design, to create trimaran equipped with state-ofthe- art wind and solar technology enabling an unlimited range.

Economic incentives

The current shipping market, affected by a global recession, faces various challenges. New international requirements impose legislations to limit ecological impact of ships, especially in relation to emission, ballast water treatment and disposal of sewage.

The attraction of an unmanned ship would also increase cargo intake in place of the conventional accommodation. Such vessels need not be equipped with all crew support systems ie air conditioning, sewage treatment plant, food storage facilities and lifeboats.

In addition to these economic considerations, statistics reveal that almost 75% of maritime accidents are attributed to human error and “a significant proportion of these are caused by fatigue and attention deficit”.

Risk management – Convincing stakeholders of safety

A challenge for designers of autonomous systems is to convince users, clients, various maritime institutions, administrations, classification societies and insurance underwriters that the system is safe and 100% reliable.

The major concern is related to the communication and flawless teleoperation between ship and SCC. Another area which requires impeccable interpretations and compatibility of data, is coordination between autonomous and conventional ships. In this sense, the ship’s architecture will be based on sensor fusion and multitask processing of data under all conditions and in all situations.

Providing that all technological challenges related to design self-maintaining, autonomous propulsion system for long deepsea voyages are overcome, the list of other factors under consideration still remains long. Each risk can escalate into different exposures leading to a consequential interdependence of a chain which is only as strong as its weakest link.

Different skillsets needed due transformation in industry

Due to the fact that conventional shipping is transforming into areas that require different skillsets, especially closely related to communication and IT systems, the role of marine risk managers will have to be redefined. Seagoing experience will likely be superseded by expertise in automation, communication, data processing and IT systems security.

Conclusion

It is doubtful that the transition from the current conventional marine transportation be abruptly dominated by autonomous, unmanned ships. The pace of transition will be rather slow and may require a couple of decades.

But once the first autonomous ship starts her virgin trip across the oceans, the new era will begin. In the aftermath of the revolution, there may be a mixture of vessels with different levels of autonomy operating at sea.

Navigating uncertain times

Mr Dieter Berg, President of the International Union of Marine Insurance (IUMI), gives an overview of the marine insurance market today, noting that there are positive signs but warning against rising protectionism which is a threat to all.

Mr Dieter Berg, President of the International Union of Marine Insurance (IUMI), gives an overview of the marine insurance market today, noting that there are positive signs but warning against rising protectionism which is a threat to all.

In 2016, the “Year of the Rooster” brought with it some fresh challenges for the marine insurance market. The rooster symbolises fidelity and punctuality, and with the continued decline in marine insurance premiums over recent years, marine insurers could do worse than adopt these two qualities as they navigate the immediate future.

A challenging market

The current market environment continues to test marine insurers. Renewals are extremely competitive with ongoing rate reductions, heated by the continuing overcapacity and an abundance of capital, leading to reduced levels of profitability.

The pressure on marine insurance premiums over the last years is beginning to level out as cycle management becomes key with regard to shrinking margins. Coupled with this, the market is now much more aware of large potential risks associated with cargo storage and value accumulation. This has led to decreasing insurance capacity in some industries, particularly in the automotive sector.

In offshore energy insurance, the low oil price and its constraining impact on oil exploration and production has encouraged insurers to compete fiercely over shrinking premium volume. The result of this has been a significant drop in premium income and a growing disparity between market premiums and actual losses. A flicker of hope is the embryonic oil price recovery and oil companies are adapting their business models to this new norm. A number of mobile units that had been laid up are now returning to service and employment in the energy sector is starting to grow.

Positive signs

The development of the global economy is an important factor/driver for global trade and marine insurance. There are some signs of emerging opportunities in 2017. We expect a slight acceleration in global economic growth, with activity projected to pick up pace this year and in 2018, particularly in emerging markets and developing economies. The current strong US dollar is helping to support struggling economies in Europe and Japan, boosting exports.

The Asian marine insurance market accounts for almost 30% of global premium income, and trade in this region continues to grow. Other positive signs include stronger growth in the USA, the recession in Brazil and Russia coming to an end, energy prices stabilising in 2016 with normalisation continuing into 2017 and a recovery in other commodity exporting countries due to higher prices. But these benefits could be countered by a rising move towards greater protectionism.

Potential risks

The banking and sovereign debt crisis in the Eurozone has not been solved and several EU member states continue to face difficulties. There is a risk of slumps in emerging markets, particularly China, where for the last three years, China’s imports have been much lower, which has negatively affected the economies of other exporting countries.

World trade volume has stagnated since 2011, with a probable decrease in 2015 and 2016. Besides the weakening of the world economy, another reason is the continued increase of protectionist measures since 2009, which is a major threat for economic growth.

More than ever, free trade agreements are currently in jeopardy, particularly in Europe and USA, where there is a political trend to blame globalisation for domestic problems, strengthening populist movements and an upsurge of nationalism. The free trade system created greater wealth worldwide and strengthened the peaceful cooperation between trading nations but has never been popular.

Free global trade and the global exchange of goods is the foundation for growth and prosperity across the world economy. Going back to nationalistic isolation and protectionism is likely to have a negative impact on all those involved – industrial countries, emerging markets and developing countries – including global marine insurance.

Mr Dieter Berg is President of the International Union of Marine Insurance (IUMI) and Senior Executive Manager at Munich Re. This article was first published in Asia Insurance Review, October 2016.

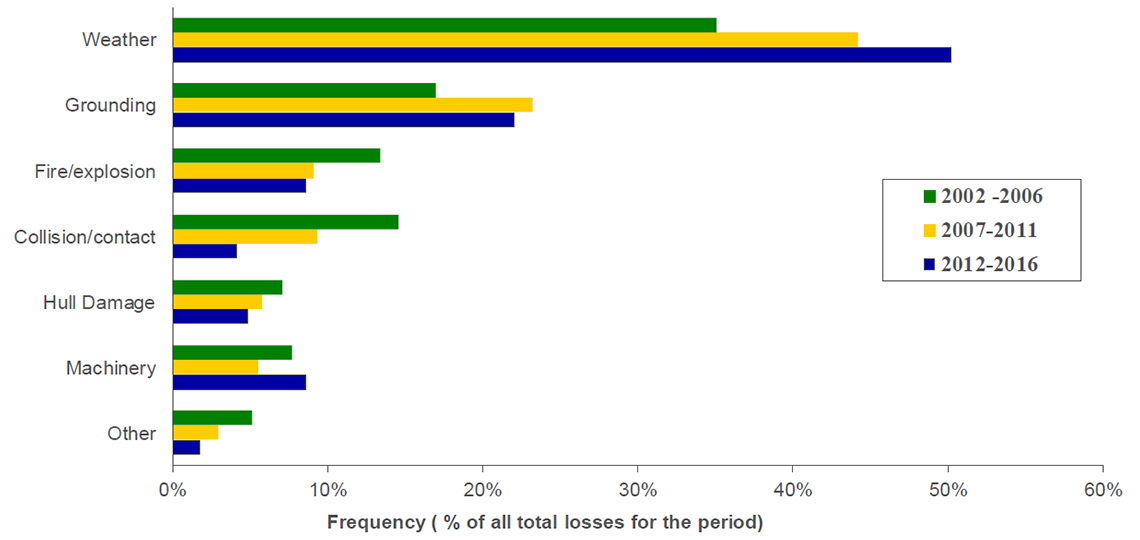

Charting Hull Casualties

Statistics of Hull Casualties

Total Lossess 2002 - 2016 by cause, all vessel types, vessels > 500 GT

Source: LLI, total losses as reported by Lloyds List

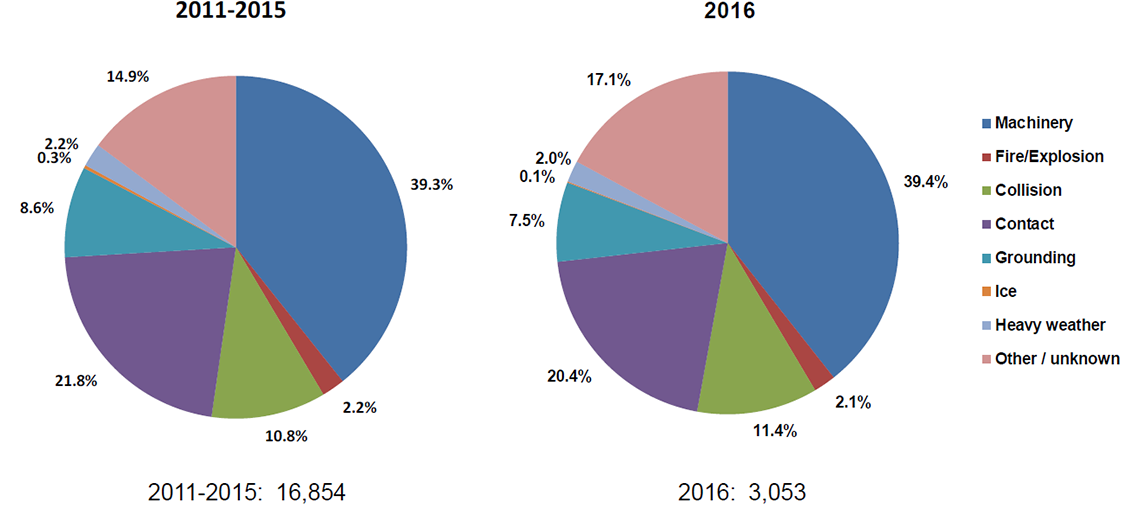

Total number of claims

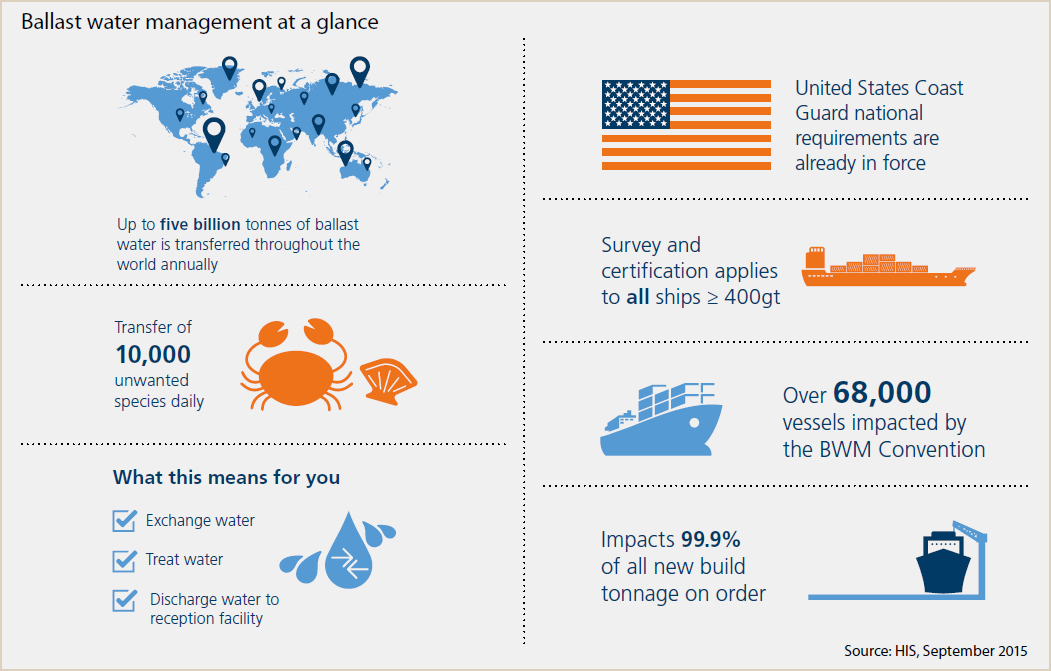

Ballast Water Management

While ballast water is essential for safe and efficient modern shipping operations, it may pose serious ecological, economic and health problems due to the multitude of marine species carried in ships’ ballast water. These include bacteria, microbes, small invertebrates, eggs, cysts and larvae of various species.

After more than 14 years of complex negotiations between IMO Member States, the International Convention for the Control and Management of Ships' Ballast Water and Sediments (BWM Convention) was adopted by consensus at a Diplomatic Conference held at IMO Headquarters in London on 13 February 2004.

The BWM Convention recently entered into force on 8 September 2017.

IUMI 2017 promises to be special

This year’s IUMI conference brings more than 400 delegates together at the “Grand Nikko Tokyo Daiba”, which is known for its beautiful scenery backdropped against the Tokyo Bay.

With the marine industry undergoing massive changes from smart ports to autonomous vessels, the theme of the conference “Disruptive Times – Opportunity or Threat for Marine Insurers?” is a timely one.

There can be no doubt that interconnected systems, which will be the norm in shipping and logistics in the very near future, are inherently vulnerable and that these vulnerabilities will be exploited. To support the industry and capture the opportunities of this new paradigm, marine insurers will have to be creative and resourceful.

Over the next three days, the conference will cover pressing topics such as the Internet of Things in shipping, cyber risks and big data analysis. A broad view of the marine insurance environment, evolving marine liabilities, automotive risks, marine security threats and the currently distressed shipping market will round off the agenda.

Here’s to a fruitful and enriching conference!

Digital forces will shake up marine insurance

Digitalisation will redefine the shipping and logistics industry and marine insurers need to have a good understanding of these technological trends in order to undertake sound risk evaluation and risk management, said IUMI President Dieter Berg.

During the opening session yesterday, Mr Berg said the theme of disruption for the conference was apt from various angles – from technology to politics and global trade.

From a macro perspective, the marine industry continues to feel the impact of a weak global economy that has resulted in lower investments as well as weaker trade, which has been further compounded by an upsurge in protectionist trends.

While there have been signs of recovery in some of the major as well as emerging economies of the world, there also remains continuing headwinds as anti-globalisation forces have put many free-trade agreements (FTA) at risk, said Mr Berg.

He added that free trade and global exchange of goods remain the foundations of growth, although FTAs would also need to be fair and balanced.

Creating new value

Parallel to global trade volumes, marine insurance premium has been steadily falling since 2012 and will continue to shrink amid disruptive forces.

Mr Berg said digitalisation will transform the existing insurance value chain, amid an evolutuion in distribution trends as well as the changing consumer habits of millennial clients.

However in response, insurers should evolve their value proposition beyond merely paying claims but also providing expertise in risk consulting – which includes preventive risk management as well as loss mitigation.

He added that technical underwriting alone will not suffice in time to come, and so insurers need to innovate by using smart technology and data analytics to identify and mitigate risk.

By being a trusted consultant and adviser, insurers provide more than just a commodotised product – which are often the easiest to digitise and disrupt.

Mr Dieter Berg also outlined three focus areas for IUMI at the moment.

- Focus on Asia

- IUMI’s strategic goal of realising an Asian hub is well underway after it opened its first office in Asia in Hong Kong last October in partnership with the Hong Kong Federation of Insurers (HKFI) - the first time IUMI has established a permanent presence outside of Europe in its 143-year history.

- Communications Strategy

- IUMI hopes to raise public awareness of the excellent work of its technical committees, as well as advocate the interest of the global marine insurance industry through continuous presence in relevant forums. Earlier this year, it launched a new interactive portal (www.iumi.com) which embraces IUMI’s new corporate identity and updated logo.

- Education

- In light of the continuous ‘war on talent’, IUMI hopes to attract more young bright minds into the industry and giving them sufficient training. In that regard, the organisation has designed a comprehensive education programme for the global marine insurance industry.

Tokyo Governor graces opening day

Ms Yuriko Koike, Governor of Tokyo, graced the opening session yesterday where she welcomed IUMI delegates to Tokyo, and briefly spelled out the facelift the city is undertaking in time for the 2020 Tokyo Olympic & Paralympic Games.

Her vision of a “New Tokyo” centres around a more diverse, smarter and safer city. She also spoke on her vision of re-establishing Tokyo’s position as the top financial hub in Asia. At present, the financial sector accounts for 5% of the country’s GDP – and the aim is to double that figure thereby boosting GDP by JPY30 trillion. The first step of this vision was the establishment of the Advisory Panel for Global Financial City Tokyo in November 2016.

She welcomed the insurance industry to do business in Tokyo as the city looks to reassert its prominence in the financial services sector – which includes a focus on asset management and FinTech firms.

GIAJ hails IUMI’s important role

As host of this year’s IUMI Conference, the General Insurance Association of Japan’s (GIAJ) Chairman, Mr Noriyuki Hara, warmly welcomed delegates back to Tokyo – which last hosted the conference in 2006.

In his opening address, he hailed IUMI’s invaluable contribution on the marine insurance education front, especially within the emerging markets.

He added the theme of the conference - “Disruptive Times - Opportunity or Threat for Marine Insurers?” – was a timely one as innovative technology has and will trigger a lot of changes within the maritime industry.

Global marine premiums continue to fall

Global underwriting premiums for the marine insurance industry fell to US$27.5 billion in 2016, a 9% reduction when compared to 2015, reported Ms Astrid Seltmann, Vice-Chairman of IUMI's Facts & Figures Committee.

Speaking yesterday morning, she explained: "The 2016 number follows a continuing downward trend in marine underwriting premiums. In 2015 the adjusted figures of US$30.5 billion was in itself a 9.9% reduction from 2014. We attribute part of the reduction to the strong US dollar when compared with other currencies, but also to general weak market conditions in terms of the global economy, general commodity prices and the poor state of the shipping and offshore sectors.

“This worrying downward trend leads to an increasing mismatch between income levels and the marine insurer's obligation to cover major losses, particularly in light of the trend for larger vessels and greater accumulation of risks in ports."

Premium income came mainly from Europe (50%) and the rising market of Asia Pacific (27.9%). Transport cargo was the best performing line of business, with 54% of the 2016 premium and global hull came in a distant second at 25%.

Cargo and hull best-performing lines

The cargo sector reported a premium income of $15 billion for 2016 – a 6% reduction on the 2015 figure. Exchange rate fluctuations impact most strongly on cargo premiums and the recent strong dollar has "reduced" premium income from most other countries, thus making it challenging to identify any real market development.

The 2015 Tianjin disaster significantly eroded the performance of the 2014 and 2015 underwriting years. The final position of 2016 is still unclear due to the impact of the loss of the Amos 6 satellite and the current issues surrounding Hurricanes Harvey and Irma.

The hull sector achieved a premium income of $7 billion, which was a 10% reduction on the previous year. Although exchange rates may have been partly attributable for the decline, this has much less impact than in the cargo sector due to the global nature of the hull portfolio.

Whilst the world fleet continues to grow, it also continues to age. A certain reduction in vessel values will follow with the ageing of these vessels, but the two-digit drop in values from 2015, and particularly for bulk and supply/offshore vessels, must be seen in the context of the challenging market environment. Hull premiums have deteriorated in line with falling average vessel values, and there is now a mismatch between fleet growth and income levels.

Keynote: A call to action

Both keynote speakers urged insurers to constantly add new value as the industry moves ahead at a rapid pace.

The trend towards environmental safety in shipping will lead to a return to wind power as well as greener technology to propel ships in the future, said Mr Koichi Muto, President of the Japanese Shipowners’ Association in the first of yesterday’s keynote address.

He said environmentally-friendly ships are trying to move towards zero emissions, as international shipping - which runs largely on bunker fuel - is coming under increasing pressure to tackle climate change by reducing emissions.

For example, global shipping firm Maersk has announced plans to fit spinning “rotor sails” to one of its oil tankers to reduce fuel cost and emissions – in what would be the first retrofit installation of a wind-powered energy system on a tanker.

As the shipping industry make rapid advances in big data, artificial intelligence, robotics and automation, cyber risk will be a major concern as well as opportunity for the insurance industry, said Mr Muto.

He urged marine insurers to respond positively to the evolving risk landscape and take up the challenge to provide the right solutions for ship-owners.

Marine Insurance in Japan

In the other keynote address, Mr Kiyoaki Sano, President of the General Insurance Institute of Japan, spoke about the progress of the Japanese marine insurance sector – where the first marine insurer, Tokio Marine, was first founded back in 1879.

Today, Japan is the fourth largest hull insurance market in the world, with a book size of approximately US$600 million.

On the other hand, its cargo insurance market ranks second in the world, behind the UK, with a book size of US$1.4 billion.

In both areas, Japanese underwriters still value “face to face communication” with clients, and Mr Sano urged them to continue adding more value to their offering as the sector looks to avoid commoditisation.

Seaborne trade still growing despite dark political clouds

Global seaborne trade increased by 3.5% in 2015 and 2016 despite political uncertainties in various parts of the world, said Mr Donald Harrell, Chairman of the Facts & Figures Committee, during his report yesterday morning.

“Seaborne trade is 85% of all global trade and the growth has been very consistent over the past 5 years,” he said. 2016 saw 11.1 billion tonnes of gods being shipped, with energy being the lion’s share of all trade (38%).

This growth occurs in a climate of political change, with US trade policy shifting towards protectionism, Brexit threatening upheaval in Europe and possible looming hostilities in the Korean peninsula.

There has been good growth in GDP in Brazil, with stable growth in the UK, US, China and India. Most of this growth is likely the result of disruptive innovation and technological advancements, as well the continued recovery of commodity pricing.

Toughest year since financial crisis

2016 has been called the toughest year for the marine industry since 2008. “There have been signs of improvement, but it is still tough to see where we will be over the next 5 years,” he said.

The growth of the world fleet is easing and is expected to stabilise around 3%. However, the possible crisis that might arise in South Korea, one of the three main sources of shipbuilding in the world, brings up the question of risk accumulation. According to a study by RMS, the two ports with the most risk accumulation sits in Nagoya, Japan and Guangzhou, China, the two other major shipbuilding sources.

“What can we do to mitigate this risk, and are there any other ports in the world that can take on some of the load?” asked Mr Harrell.

The offshore industry is going through its own series of issues, with almost 50% of all rigs currently stacked and 33% of OSVs in the same situation. Fortunately, Hurricane Harvey managed to avoid most of the offshore production and laid-up assets around southern US.

Mr Harrell also projected a positive future for rig utilisation, in 2017and 2018, correlating with the slow rise of oil prices. “A slow growth is good for the industry, we don’t want a sudden spike in prices,” he said.

Steady decline in number of loss incidences

“Since 1999, we’ve gone down to 0.1 to 0.2% of the world fleet in terms of loss incidences,” he said. “If you break it down by type, weather is the largest cause of loss, which indicates that there have been a lot of things the industry has done to manage risk, to improve maintenance and improve shipping schedules and it has had a great impact.”

IUMI Executive Committee 2018 announced

At the 143rd annual meeting of the IUMI Council, Secretary General Lars Lange revealed the proposed lineup of the Executive Committee for 2018.

The Executive Committee is responsible for the administration and management of IUMI in accordance with the general policy determined by the Council. The Executive Committee is limited to six vice-Chairmen.

On top of that, the Executive Committee also appoints the Secretary General, the Liaison Officers and Observers.

- Dieter Berg, Germany – President

- Frank Costa, USA – Vice-Chair

- Agnes Choi, Hong Kong - Vice-Chair

- Lars Rhodin, Sweden – Vice-Chair

- Colin Sprott, UK – Vice-Chair

- Patrizia Kern-Ferretti, Switzerland - Vice-Chair

- Takeshi Miyazaki, Japan - Vice-Chair

- Lars Lange – Secretary General

New risk landscape for marine cargo

Mr Mike Davies, XL Catlin’s Chief Underwriting Officer, Marine, for Asia-Pacific, shares his views on some of the major opportunities and threats facing the logistics industry.

The theme of this year’s IUMI conference is "Disruptive times - opportunity or threat for marine insurers?" What's your view?

New competitors, tailor-made solutions and technologies have always been a factor in the maritime shipping and logistics industries. Today, however, it does feel as if these disruptions are coming more quickly and from more quarters.

Do these represent an opportunity or threat? Both are distinct possibilities. What’s more relevant is how companies respond when something new and innovative emerges.

The imperative today for businesses across the sector is improving operating efficiencies and resource utilisation. In my view, the innovations that could help companies achieve these outcomes include autonomous control systems and self-steering ships; connected objects and the internet of things (IoT); and blockchain and online freight platforms.

How will mobile autonomy and the IoT impact the industry?

Automotive and technology companies have invested heavily in mobile autonomy, and the technologies that make it possible are rapidly becoming more sophisticated and less expensive. These innovations are now starting to appear in our industry; self-driving ships are currently being tested, and some will go into operation next year.

The primary benefit of un-manned fully autonomous vessels is that the elements and systems devoted to the crew can be scaled back if not eliminated. That leads to lighter vessels with lower construction and operating costs. Some observers predict that an autonomous ship could reduce transport costs by as much as 20% compared to a traditional vessel.

At the same time, the proliferation of sensors and connected objects will enable ship owners to monitor the performance and condition of different components with greater precision and reliability.

And perhaps more importantly, outfitting more and more containers with sensors could help insurers to better understand accumulation exposures. That, in turn, would enable underwriters to tailor coverages more precisely and also bring reinsurance costs down.

Finally, spoilage and theft are the most frequent losses cargo owners and insurers face; sensors in containers could substantially reduce the incidence of these events. Furthermore, reductions in the cost of tracking devices now make it more feasible to secure high-value shipments like pharmaceutical products and electronic devices that are attractive to cargo thieves.

How will these and other developments affect the risk landscape?

The industry already has an admirable safety record. Nonetheless, research shows that about 80% of incidents, both at sea and on land, are caused by human error. So the introduction of autonomous control systems should lessen the likelihood of accidents.

At the same time, these technologies can introduce new threats. While the pace of innovation continues to accelerate, the security of many applications are still lagging. IoT devices, for example, often lack basic protection measures.

These vulnerabilities pose a significant challenge to shipping companies and port operators, and to their insurers. Drug smugglers have already hacked the control system at a major port, and there are examples of autonomous vehicles being commandeered by an “outsider.” Many people are rightly concerned about the possibility of a terrorist organisation taking control of a giant self-steering ship.

These developments also have significant implications for our marine risk engineers. In particular, as ships become increasingly automated, marine risk engineers will need to develop expertise in AI, robotics and IT systems as well as know-how in assessing the capabilities and psychological fitness of land-based controllers.

Mike Davies has more than 35 years of experience in marine underwriting and has been based in Singapore for most of the past 20 years. He has also held several leadership positions with IUMI, including serving as Vice Chairman of the Executive Committee and Chairman of the Cargo Committee.

A welcome 11 years in the making

Japan welcomed the 544 delegates of IUMI 2017 on Sunday evening, treating them to the best Japanese cuisine and serenading them with traditional Japanese music.

The inclement weather did nothing to dampen the mood, as the members of IUMI - both old and new - enjoyed the very best of Japanese culture.

Special mention to the organisers for the smooth and efficient proceedings.

Work needed for better treatment of seafarers in accidents

A high level code of investigative conduct should be developed for maritime nations in order to have a more transparent and efficient process when dealing with maritime accidents in sovereign waters, said Captain Jonathan Walker of the London Offshore Consultants in the Political Forum workshop yesterday morning.

Speaking on the topic ‘Government intervention impacting the cost of claims’, Captain Walker said that while the industry acknowledges the sovereign right of authorities to conduct investigations, detention and long delays still occur which, among others, may be due to a slow investigative process, convoluted laws and emotive local issues that may result in the criminalisation of seafarers.

Crucially in some cases, the grounds for such detentions have not been clear to the seafarers being detained or to the international maritime community, he added.

Captain Walker offered several suggestions which includes a unified approach by the International Maritime Organisation (IMO) to develop a marine investigation code to ensure greater transparency, as well as a call for the IMO and ILO to develop early release procedures for seafarers under investigation by member countries.

He added that many seafarers suffer emotionally and financially from the long detention of vessels, and much more needs to be done to protect them from unfair incarceration.

He also encouraged marine insurers to be more proactive in maintaining regular conversations with government officials, as appointed officials may change quite frequently in certain jurisdictions.

Both insurers and governments should also ensure that those dealing with marine casualties have the requisite knowledge and experience, as a lack of expertise would increase cost dramatically.

Two-thirds of all ferry accidents happen in 5 countries

Approximately 3000 people die every year in ferry accidents, said Mr Neil Baird of the World Ocean Council during his presentation on fatal ferry accidents. “I say approximately, because reports are few and far between, especially in the black box of local government.”

Mr Baird also added that 80% of all ferry accidents over the past 15 years occurred in ten countries, while 66% occurred in five - Bangladesh, Indonesia, Philippines, Tanzania and the Democratic Republic of Congo). “Fatal ferry accidents are overwhelmingly concentrated in the hot, humid, poor, corrupt and water transport dependent areas of the tropics,” he said.

In these danger zones, a lot of the vessels used are mismanaged or mishandled, lacking adequate safety measures and are poorly maintained. Most of them also suffer from overcrowding of passengers.

Even still, the best designed, built, equipped and ‘safest’ ship is doomed if its commander and officers fail to exercise good seamanship and common sense, he said. Human error is the cause of 98% of all fatal ferry accidents. However, there are still incredibly unsafe concepts for seafaring vessels, such as the monohull Ro-Pax and the Filipino motor bancas.

Governance and enforcement needed

Ferry accidents cause about 4 times more fatalities than aviation accidents, but remain woefully underreported. He brought up the ‘Dona Paz’ disaster in the Philippines in 1987, which had over 4000 fatalities, but remained mostly unknown by most people in developed countries. While the advent of the internet has caused a large spike of reported incidents – almost tripling the number of reports – there is still not enough done to resolve the issue, with local authorities appearing remarkably unconcerned.

“Poverty, corruption, ignorance, fatalism and negligence combine to contribute to the appalling record in these 5 countries,” he said. “With the exception of the Philippines, nothing is being done to improve the situation, with some of them getting slightly worse.”

The extent of corruption bleeds into all aspects of the ferry operation, to loading controls, safety surveys and awarding of certificates of competency, as highlighted in the inquiry reports of the Rabaul Queen (Papua New Guinea, 2012) and Sewol (South Korea, 2014) incidents. The Sewol disaster also revealed how even developed nations are not immune to this problem.

There seems to be no aid to be received from international bodies, either. “IMO mandate specifically excludes domestic travel, which is the majority of all ferry travel,” said Mr Baird. He criticised the IMO for their ‘token’ efforts in some of these developing nations, even after considerable urging from Interferry and Worldwide Ferry Safety Association.

Prediction of more regulations

During the panel discussion on regulation, attendees were surveyed about the current state of regulations. The answers below highlighted very obvious trends within the industry, as well as the concerns marine insurers have.

"Far too many regulators do not understand us at all, but they do control our destiny, which is why we have to try to get through to them," said Mr Neil Roberts, of Lloyds Market Association and Committee member of the Political Forum.

Do you think there will be less government intervention in the future?

-

No

86.0%

-

Yes

14.0%

The main driver for regulation will be

-

Environmental concerns

45.8%

-

Safety concerns

21.5%

-

Disruption (technology, geo-policies)

14.0%

-

Financial

18.7%

Is the industry prepared for a cyber attack on connected systems on board vessels?

-

Yes

3.4%

-

A few companies are

45.3%

-

Most companies are

4.3%

-

No

47.0%

Can regulation keep up with disruptive new technologies?

-

Yes

10.8%

-

Yes - in 20+ years

26.1%

-

Not likely

48.6%

-

Never

13.5%

Japan's fishing industry has recovered post-tsunami

The earthquake and tsunami that ripped through the Tohoku region of Japan in 2011 almost brought the local fishing industry to its knees. Six years on, the resilience of the Japanese people is evident, as Mr Koji Okumura of Munich Re reported that the Japanese fishing industry has hit 99% of its recovery targets.

The 9.0 magnitude undersea earthquake – the strongest recorded in Japan and the fourth most powerful earthquake since 1900 – triggered tsunami waves up to 10 meters high, leading to the destruction and damage of almost 29,000 fishing vessels and 319 ports. Combined with the losses in aquaculture facilities and stock, the total cost was just under US$16 billion.

The local government targeted 20,000 of those vessels to be repaired and returned to full function, of which they have hit 92% of the target as of this year. 99% of all affected ports have recovered to full operation and 99% of all wrecks have been removed from aquaculture and stationary fishing sites.

Improving Japan's fishing industry

However, there are still challenges that remain for the fishing industry. The number of fishermen have been declining over the past decade, with only 160,000 remaining as of 2016 (there were 222,000 recorded in 2008). At the same time, fishermen are an ageing population, with their average age at 56.2. There has also been a decline in the consumption of fish in Japan.

Furthermore, only 167,111 fishing vessels have been insured as of 2016, representing a steady drop since 2012, even less than the number of insured vessels in 2011.

However, several efforts have been taken to continue improving the health of the fishing industry. An expansion of the direct fishing market is underway, providing fishermen the ability the sell directly to customers and afford them better control of prices.

Improved risk management against tsunamis have also taken place, with the construction of more breakwaters and embankments, as well as updated evacuation simulations and guidelines.

Maritime sector faces evolving risks?

The maritime sector is seeing new and emerging risks and facing challenges. In this extract from a speech, Mr Todd Wilhelm of QBE Insurance gives an overview of the sector today.

Today’s marine insurance sector is as much in a forward-moving mode as it has ever been. Whether we like it or not, there is no turning back to a more predictable global economic environment and a calmer geopolitical situation.

There is also no turning back to what one maritime economist calls “The Marvellous Millennium”, the period between the late 1990s and 2008, when surplus capacity was a rare event, and when ship owners saw fortunes coming back in their favour. No turning back to the days of fewer regulations, lower compliance requirements and less disruptive innovation. Gone are the times of smaller, less complex ships.

Climate of uncertainty

Today, we operate in a climate of uncertainty. For example, today’s environment is one where a number of nations are negotiating more free trade agreements, yet there is also concern over increased protectionism in some markets.

What’s more, there are predictions that, over the next couple of years, global trade will grow at the slowest pace since the last financial crisis. We seem trapped in a place where variable economic reports and political instabilities impact business confidence.

For insurers, the concerns go beyond the growing sizes and increasing complexities of ships, not to mention worries about salvage capabilities when a large ship is lost. The conversation also includes concerns about the massive cargo values that these gigantic vessels may carry.

Ultra large vessels can quite quickly translate into ultra large losses. The concentration of risk is considerable when you think about: a US$200 million ship could be transporting 19,000 TEU that collectively might hold several hundred million dollars’ worth of cargo.

Insurers must know what clients/ brokers are looking for

Against this backdrop of continued uncertainty and rising risk intricacies, maritime insurers really only have one option. Like Cortés’ men, they also need to move forward.

Obviously, this must be accompanied by our vow to continue providing and delivering insurance products that meet the particular needs of the maritime market.

Equally obvious is the fact that insurers cannot move forward as if we are on our own little island. We need to continue to collaborate closely with brokers, agents and end-customers to identify and satisfy their needs. We must be ready to offer bespoke solutions regardless of how complicated the issue. We also need to continue to share information and data, not only on products, but also on trends.

Ultimately, we need to be customer-focused in product innovation. Customer-driven in product design. Most importantly, we must be customer-centric in product delivery.

New breed of marine underwriters

The most acute need is for a new breed of marine underwriters who understand the evolving risks, and can tailor products to meet the marine industry’s changing needs.

As the President of the International Union of Marine Insurance has noted, marine underwriters are now facing levels of risk previously unheard of. This means that within the insurance industry, we need to continue to attract, develop and cultivate smart, solid, technically capable marine underwriters. It is imperative that we create and retain specialists with expertise not only in underwriting, but also in issues related specifically to shipping.

This article was first published in Asia Insurance Review, October 2016.

Cape Town beckons in 2018

The IUMI Conference moves to Cape Town, South Africa, next year where the organisation will hold its 144th Council Meeting.

We all look forward to another exciting edition of the conference against the splendid backdrop of South Africa’s enchanting southwest coast!