The phoenix, a colourful, vibrant and long-lived mythological bird, cyclically and spectacularly regenerates from its own ashes. Australia’s life insurance industry, which has been suffering scorched earth since 2011, is now rising from those ashes, led by claims management innovation, says Mr André Dreyer from RGA Reinsurance Company of Australia Ltd.

The year 2013 was, at best, challenging for Australia’s life insurers. While claims experience had been deteriorating for several years, never before had there been the sort of slump as was experienced by the country’s group disability market last year.

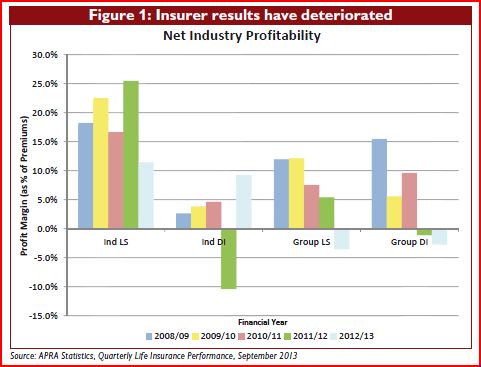

Unusually high and unexpected losses

In 2011, individual income protection (disability) insurers in Australia had begun experiencing unusually high and unexpected losses stemming from several causes, including underestimating the length of time disability claimants stay on claim.

By the end of 2013, just two years later, claims experience had reached unprecedented levels, with significant group lump-sum disability losses dominating. Individual income protection claims experience had further deteriorated and losses attributable to individual policyholder lapses worsened as well. According to fourth-quarter 2013 statistics published by the Australian Prudential Regulation Authority (APRA), which regulates the country’s financial services industry, life industry profitability was well below expectations (see Figure 1).

Reinsurers increase claims reserves by more than US$1 bln in 2013

The most common explanation offered for losses on the group side in Australia was that the environment changed rapidly over the past decade, so much so that using past claims experience to credibly price large group policies had become an unreliable predictor of future claims experience.

However, no one could have anticipated that claims experience would deteriorate as rapidly as it did from 2011-2013. Group disability experience in 2013 was quite extreme, which contributed to the country’s four largest reinsurers collectively increasing reserves by more than US$1 billion.

These losses sparked a genuine push for change in Australia’s disability market. Price increases alone are not likely to return group disability to sustained profitability. Changes to product design, conditions around eligibility for group cover and a paradigm shift in claims management should be, and is, underway.

By the end of 2014’s first quarter, many Australian life insurance companies have either completed or were planning to revise its claims practices. Some are even revisiting their entire approach to claims management.

There appears to be two schools of thought in addressing the current and growing challenges faced by claims departments: some seek to improve current practices and optimise the existing claims payment model, while others, having endured the recent challenging results within the current framework, are willing to try new things.

Innovation – Burn it to the ground

Over the past several years, more than a few innovations have occurred across the life insurance continuum. For example, companies have moved from participating to non-participating policies. Critical illness cover, invented 25 years ago, has evolved into a range of options including severity-based, multi-pay and single impairment policies. Insurers have also developed and introduced functional impairment disability policies to supplement and sometimes replace occupational disability policies.

Underwriting rules engines (UREs) have been automating new business processes for life insurance companies for more than a decade. Although Australian life insurers were relatively late adopters, this technology was vigorously embraced and the country soon became a leading market in terms of the proportion of insurers using UREs.

Claims processes, however, have seen little innovation until now. Indeed, few Australian insurers today have automated claims workflow systems in place.

The Australian life insurance industry is currently undergoing a once-in-a-generation sea change in claims management. This market cannot continue to handle the current rising incidence rate and claims payment volumes, and insurers see that the rapidly growing demands on claims professionals need addressing. Pricing and product features can and will repair future generations of claims risk, but companies now need to address how they handle claims on current risk exposures.

A new claims paradigm

The goal of disability claims management today is to provide necessary services, using appropriate resources in cases where there is a potential to recover, to promote an impaired individual’s maximum recovery and productivity.

Life insurers in Australia know that effective claims management can bring immediate bottom-line results. Hence, some are looking to invest as much as A$50 million (US$46.3 million) in claims systems and processes in the coming years.

Return-to-work and rehabilitation programmes are proven, effective tools in disability claims management. However, the true potential of these management tools as well as others, used smartly and effectively, has only recently become apparent. The industry is also benefiting from ideas found to be effective in other countries and for affiliated industries, such as workers’ compensation.

In the late 1990s, Canadian group disability insurers, under pressure for improved results, substantially reinvented their approaches to claims resulting in a paradigm shift from claims adjudication (centred largely on the eligibility decision relying on medical diagnosis) to holistic case management (which extends its lens beyond the medical to such important elements as the functional and vocational workplace factors). Not only does this broader perspective substantially impact the eligibility decisions, it provides the necessary understanding to properly manage a case to a positive resolution.

Challenges today - Mental illness, ageing population and obesity

According to Ms Maria Vandenhurk, founder and chief operating officer of Banyan Work Health Solutions, based in Toronto, Canada, the country’s fast-changing landscape is again forcing group disability insurers to prepare for new challenges. Canadian claims operations that have not already evolved to best practice are under considerable pressure to do so as a result of challenges such as:

• Greater complexity in mental illness claims, and the increased presence of “coping with life” issues not specifically labelled as mental health. A preponderance of such claims are occurring among individuals under age 40, frequently indicating difficulty coping with such elements as the “sandwich generation” (simultaneous demands of child care and elder care), financial strain prolonging working careers (especially stemming from the recent financial crisis), marital breakdown, and reduced resilience (or perhaps willingness) to work while managing unwelcome and stressful life changes.

• As in most developed markets, Canada’s population is ageing rapidly and a massive exodus of its working labour force (the “boomers”) is expected through the coming decade. The new workforce poses a high level of uncertainty in terms of disability incidence rates and cultural receptiveness to the industry’s claims management techniques.

• The continual and staggering rise of obesity throughout the world’s population was also evident in Canada. Obesity is linked to impairments such as diabetes and cardiovascular disease as well as to mental and other health conditions.

The resulting impact of these trends was unprecedented. In Canada, 25% of mental health short-term disability claims outside of the province of Quebec were becoming long-term claims. In Quebec almost one in two converted to long-term claims! In the US, by comparison, only 8% of mental health short-term disability cases converted to long-term claims.

Focus on prevention and minimisation of illness and disability impact

Best practice “case management” is a model that focuses on prevention and minimisation of the human and economic impact of illness and disability. Moves toward this model in Canada have thus far resulted in considerable gains both for employees and employers in Canada. Active stakeholder engagement is central to the approach, involving the employee and employer, the insurer, treatment providers, and union representatives (where applicable). The end result is optimised quality of care, improved productivity and return-to-work rates, organisational health, and as a welcome by-product in Canada, regulatory compliance.

A growing body of medical and psychological research literature provides evidence that work is healthy and contributes to both quality of life and longevity. According to Ms Vandenhurk, claims decision-makers need to believe they are doing good, seeing themselves as promoters of health and productivity.

In our view, a holistic approach to claims management is worth further exploration in Australia. Such an approach, with a focus on incorporating claims assessment, planning, management, with medical and vocational aspects, workflow, use of resources and quality assurance, can help realise a lasting transformation of claim practices. Process improvements are achievable, and change is possible, as many of the practices are reasonably simple to understand, perhaps more challenging to implement, yet fundamentally all the same.

Conclusion

Going forward, investments in claims systems, processes and professionals will be critical for many insurers. The disability claims management innovations of the past few years are now becoming part of Australia’s claims landscape, promising stronger, more effective financial outcomes for insurers. The old status quo is no longer an option; investment in claims transformation and paradigm shifts are much welcomed and promise to continue for several years to come. The resulting effect on the Australian market could be as exciting and grand as the rebirth of the mythical phoenix.

Mr André Dreyer is Vice President, Business Development at RGA Reinsurance Company of Australia Ltd.