The costs of funding healthcare for the elderly are continually changing due to increasing life expectancy coupled with higher healthcare costs. However, in addition to these factors, the introduction of Solvency II and continued low interest rates have put pressure on the funding mechanisms. In this extract from The Geneva Association’s Health and Ageing newsletter, Mr Stephen Bishop from Munich Health (part of Munich Re) looks at the issues surrounding funding mechanisms and the impact of regulatory change.

The growth over time of health costs in excess of consumer inflation is well documented. The important issue for elderly care is the cost changes relative to the working-age population. Data from many sources indicate that the costs for both acute and chronic diseases increase almost exponentially as a person ages.

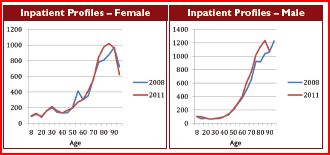

For insurers, this poses a challenge as the costs are not easily predictable due to small population samples and high claims volatility. The graphs below (courtesy of PKV [Verband der Privaten Krankenversicherung-the German private health insurance association]) indicate the changes in age profiles from 2008 to 2011 for both males and females in

Germany.

There was considerable change at the older ages during this relatively short period and this has serious implications for premium adjustment mechanism and, consequently, future premium increases.

Health insurance funding models

Funding mechanisms within healthcare insurance can be generalised into four distinct models:-

• risk premium models

• long-term funding models with levelled premiums

• risk equalisation systems

• Individual healthcare accounts (not common within Europe)

Risk premium funding

Risk premium funding is common in many countries, it involves the policyholder paying an annual premium which is directly linked to the expected annual healthcare costs.

The premium has no funding element and hence the premium will increase every year in proportion to annual medical inflation plus the increases due to ageing.

The risk premium funding model has the advantage of offering a lower starting premium to younger policyholders; this is beneficial in a non-compulsory system, as it encourages people to take out healthcare insurance early in their working careers. The disadvantage is that the premiums continue to increase because there is no savings mitigation with the premium structure; consequently there is a significant lapse risk at older ages since the premiums can become too

expensive.

However, there are significant advantages for the insurer under the new Solvency II legislation. Contracts will normally have a duration of one year if sufficient flexibility is allowed in the contract structure. A one-year contract duration allows the insurer to hold less statutory capital. Also, the reserve requirements are considerably reduced in this structure, as the insurer only has to hold reserves for claims which have been incurred but not paid.

Both effects together reduce the capital costs of writing risk premium business, and this can be passed onto the policyholder in terms of lower premiums.

Long-term funding models with levelled premiums

Long-term funding models are common in countries such as Germany and Austria. The premium rates are set to be level over the lifetime of the policyholder. So the premiums include a savings component.

However, the premiums do not include any allowance for future medical inflation, so the premiums will still increase annually. The business model requires an ageing reserve to be built up over time and later reserve releases to provide a lifetime funding mechanism. In some systems there is a policyholder fund built up within the insurer to cushion against shocks in the underlying health system.

The implications of long-term business for the insurer are totally different than for risk premium business. The Solvency II model requires insurers to perform long-term shocks on the business for lapses, morbidity, mortality and expenses in order to ensure that sufficient capital is held for the potential variation in these underwriting risks.

However, more importantly, the ageing reserves require asset backing and these assets, eg government or corporate bonds, create credit-spread risk for the insurer, but also a potential asset-liability mismatch (ALM).

The duration of long-term business liabilities can be in excess of 60 years and the asset universe does not have vehicles which can provide a perfect match for these long durations. This results in an ALM mismatch being created which requires the insurer to hold further capital.

Ultimately, an insurer writing long-term, funded business will have to hold considerably more capital than a risk premium insurer which increases the premium rates for the policyholder if the insurer is aiming to earn a target return on the capital employed.

Individual healthcare accounts

The individual healthcare account has been investigated in several countries. It consists of a product where there is a clear separation between the funding component (an individual savings account) and the insurance contract where the claims are paid.

There are many structures which can be employed to deduct monies from the savings account, for example, it could be the policyholder’s individual claims subject to a cap, or it could be a pooled risk charge across the underlying population.

The proposed advantages of the healthcare accounts are that they create more transparency about healthcare costs and, hence, allow policyholders to assess their healthcare consumption and become actively involved in their healthcare decisions. Also, in some cases, the account balance can be transferred and be directly allocated to the policyholder.

One disadvantage of healthcare accounts is that, for nationwide health systems with limited elderly care provision, the accounts need to be topped up if health-care costs continue to rise. This can prove to be costly for elderly people and result, in potential lapse activity.

For insurers, the advantages of healthcare accounts are that the insurer does not need to provide investment guarantees, as the account balance can be carefully outsourced to a third-party provider. This can reduce capital costs for the insurer.

However, depending on the contract between the account provider and the insurer, there could still be a residual credit risk to the insurer; hence, the legal structure of the contract needs to be carefully assessed.

Other forms of funding

Capitation arrangements

There are other systems of funding in operation, for example, the combined hospital and insurer partnership where the government and/or individual pay a capitation fee to the hospital/insurer.

The insurer and hospital then provide healthcare services for the elderly population within the predefined budget. This model works on the basis that the capitated rates have been calculated correctly and can cover the expected costs.

The insurer under this model is responsible for ensuring the costs are kept under control using standard managed-care approaches. The capital requirements will be similar to those of the risk premium insurer, but better claim management processes are normally required.

One of the disadvantages of this approach is that it can be difficult to become national, as local provider arrangements are required to make the system efficient. Even in the US, not all national carriers have a complete nationwide medical network and, in some cases, the insurers provide services in very compact geographical areas.

Pre-funding vehicles

Some companies have also developed pre-funding vehicles, which act as deferred annuity contracts to help minimise the cost increases at older ages by providing a fixed monetary reduction to the underlying premium.

These products, however, normally contain investment guarantees and hence are capital-expensive under the proposed Solvency II regime.

Alternatives changes to help manage costs

US Medicare insurers have had significant experience in implementing systems which control the underlying costs. These processes include initiatives such as home care, where nursing staff visit the elderly to assess the health status of the policyholder and to ensure that correct treatment is being provided.

Of course, the insurer has an interest in receiving an accurate health assessment to ensure it gets the correct reimbursement from the government and avoids costly inpatient treatment.

Also it is critical that there is a strong gatekeeper regime whereby the primary care structure can help to control the costs via regular health monitoring and strong directed network management. If policyholders have a strong link to their primary care physician, there is also less chance of them going to the emergency room for non-critical care.

Finally for elderly care it is necessary to have specialist outsourced services for very specific issues such as mental health, dialysis and diabetes care. These specialist services can avoid expensive escalation of the costs towards inpatient stays.

However the take-up of these initiatives in Europe has been relatively low. There are many reasons for this low take-up: many European countries are still focused on their national health services and there is a political reluctance to outsource activities to private providers.

In addition many European policyholders are used to having freedom of choice in selecting their healthcare services and dislike being closely monitored and directed by their insurers.

Conclusion

There is a wide range of funding mechanism across the worldwide healthcare insurance industry.

Each system essentially shares the healthcare costs across an individual’s lifetime, and the balance of guarantees is shared between the policyholder and insurance company to varying degrees. However, without any changes in the health system or government support, the funding mechanisms will not change the underlying cost structures.

Medical cost control is fundamental to making the lifetime cost more affordable to the policyholder. But this requires government, the insurance industry and providers to work together. Currently, there is no perfect system in place, the US is focusing on building up stronger incentives between the providers and insurance companies to minimise costs.

Whereas, within Europe, there are various initiatives to pass increased costs management responsibilities on to the insurance industry rather than negotiating directly with the providers.

Overall, there is no clear trend in the global health insurance industry and various models will continue to exist. Solvency II will place more pressure on health insurance providers to assess their capital costs and funding efficiencies.

Mr Stephen Bishop is Chief Actuary at Munich Health (part of Munich Re).