Asia’s fast-evolving markets and workforces are prime candidates for voluntary group insurance products, which can serve a myriad of needs. Mr Anil Sanwal of RGA discusses the benefits of voluntary products for employee, employer, broker and insurer.

Many trends in today’s Asia markets are increasing employers’ interest in providing voluntary (or supplemental) insurance products for Employer’s Life and Health Benefit plans.

Fast-evolving demographics is the strongest trend. Ageing baby boomers are driving rapid rises in median population ages in mature markets such as Korea and Japan, both of which are predicted by 2050 to have median ages of 53. In faster-growth developing economies, median ages skew far lower: for most, current median ages are 30 and younger.

A second trend is the gradual withdrawal of governments from providing social benefits. This is shifting the cost of providing these benefits to employers and ultimately individuals. Finally, Millennials are entering the workforce in increasing numbers.

Flexible customisable benefits

Today, a broader range of workers’ ages and insurance needs exists in each age group than ever before. Baby Boomers, now many of the oldest workers, have the most need for health-related covers and long-term care. Mid-career employees, whether pre-boomers (the latter half of the Baby Boom) or Generation X, require more varied life, health and disability benefits, as many have young children and older parents who depend on them for financial support.

All of these cohorts include singles (with or without children) and marrieds without children, both of which will need life insurance and generous health and possibly critical illness covers, to allow them to employ caregivers should they or an elderly parent becomes critically ill.

Insurers must be aware of these emerging and evolving needs and the expectations all of today’s workers. Today’s traditional one-size-fits-all benefits package holds little appeal for Generations X, Y and Millennials.

These workers want flexible, customisable benefits and seek access to a range of coverages and perks not traditionally thought of as employee benefits, such as home and auto insurance, extra vacation time and travel concierge services. These can present opportunities for insurers to increase their employee benefits business by focusing on solutions and developing effective voluntary products for them.

About voluntary benefits

Voluntary insurance benefits are typically offered at lower group premium rates. They are funded either in full or in part by employees and are generally in four categories: supplemental health; income/asset protection; security (eg, life insurance); and personal insurance.

The products supplement or can even replace employer-paid benefits such as life, health and disability cover. Some also cover niche needs such as financial counselling, identity theft protection and pet insurance.

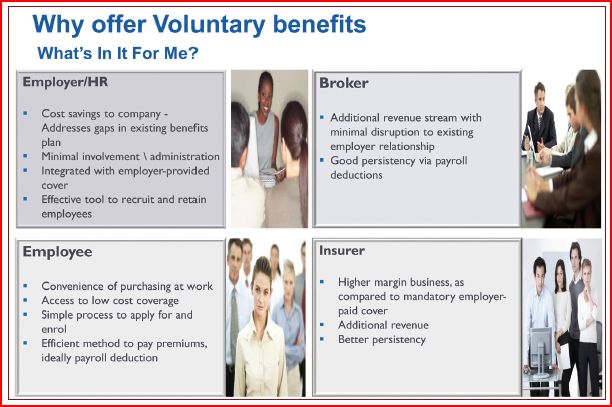

Designing voluntary products for employee benefit programmes can be an opportunity for insurers to differentiate themselves. The table on the left describes additional pluses for the insurer, the broker, the employer and the employee of making voluntary benefits available at the worksite.

Employers offering certain benefits on a voluntary basis can better control overall benefit plan costs, address gaps in existing plans, and are perceived as progressive and interested in employees’ well-being.

Research by Eastbridge Consulting Group Inc on the US voluntary benefits market – the largest in the world – shows that employees who can purchase voluntary benefits at the worksite are more engaged, more loyal, more productive, and less likely to leave for another job.

Increased insurer competition has resulted in commoditisation of many group insurance products, reducing the effectiveness of benefits programmes as a way to attract and retain good workers. Voluntary products can shift business development focus away from a few highly competitive and commoditised market segments and spark the development of a broader array of group products.

Opportunity markets

Right now, workers age 55 and older are presenting strong opportunities for voluntary insurance. Adults are increasingly working to older ages for a variety of reasons, the most frequent two being financial need and the desire to continue working.

However, employer-paid mandatory cover often reduces from ages 60 to 65 and terminates at around age 70. This is done to manage the higher mortality risk as well as acknowledge that life insurance needs diminish with age. An underwritten voluntary product for employees aged 55 and older designed to offset this reduction in employer-paid coverage could allow employees to retain sufficient life cover as long as they are actively working and based on their own unique needs.

The large, growing and underinsured middle-income market is also ideal for voluntary products. These individuals have a well-documented need for far more life insurance than is available from their employers. Employers typically provide insurance coverage at one or two times’ salary, yet their need range from three to 10 times’ salary, depending on their level of earnings and number of individuals dependent on them for financial support.

According to LIMRA, half of US households are currently underinsured and at least 60% are underinsured by an average of nearly US220,000. In Canada, LIMRA has found that 30% of working Canadians carry no life insurance on anyone in the household and 45% are underinsured, carrying only employer-provided group life insurance that covers, on average, only 2.2 years of replacement income.

Offering voluntary top-up life cover to middle market individuals can be a successful way for insurers to introduce a product and for employers to introduce a voluntary programme. If successful, the insurer’s voluntary portfolio can be increased in breadth and variety.

A third opportunity is disability income, where voluntary and mandatory cover can work hand-in-hand. Today’s typical group disability product pays approximately 66.6% of salary and continues to age 65. With morbidity costs rising and the average tenure of younger employees shrinking, some employers now offer products that replace only 30% to 40% of pay and a three- to five-year benefit period. Voluntary group disability cover that will top-up replacement ratios up to 70% of pay and a benefit period that could extend to age 65 can be a beneficial addition to employer programmes.

Successful entry

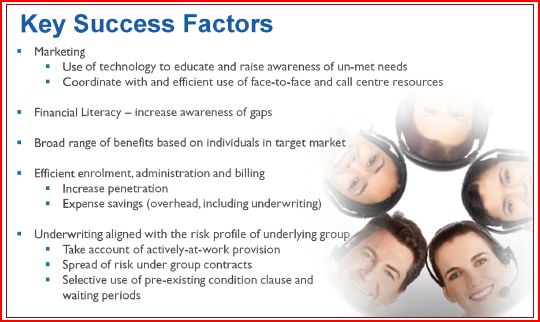

A successful plan of entry into voluntary benefits will require insurers to have a strong, well-strategised portfolio of products, an understanding of the market’s many areas of good potential as well as of its risks, and the ability to provide the technological capabilities to make end-to-end processing as smooth and seamless as possible.

The benefits of voluntary products for an insurer are many, but a primary one is that insurers can effectively reach underinsured workers at a range of life stages via a cost-efficient distribution channel.

By being aware of changing demographics and other risk factors, group insurers can enhance their voluntary offerings, protect the profitability of the business line, and help employer clients position themselves to respond to new and evolving market needs.

Mr Anil Sanwal is Vice President, Group Products at RGA.