Usage Based Insurance (UBI) is fast becoming a mainstream game-changing offering for general insurers in the US, Europe and elsewhere directly due to its outstanding results, says Mr Andrew Dart of CSC.

Once upon a time, an Insurance COO was walking along a beach, deep in thought. His CEO had just asked him to increase their motor business. He was in a sweat, knowing that he could quickly increase sales by dropping premium rates and excesses, but that claims would also follow. Their loss ratio was already 103 – a marketing push like that would certainly throw them further over the edge! On he walked.

As he strolled, deep in thought, he came across a strange glowing bottle, rolling back and forth in the surf as waves gently lapped on the beach. He picked up the bottle and marvelled at its exquisite beauty, yet simple design. Wondering what on earth could be inside such a work of art, he pulled off the cap. Suddenly, purple smoke erupted from the opening, which gradually took the form of a smiling Genie.

Three wishes for a motor portfolio

“Who the heck are you?” asked the stunned COO.

“I am the Career Genie. I grant three wishes that help people along with their jobs.” The Genie replied.

“OK” the COO thought, “Let’s test this guy out.” He said, “Genie, for my first wish, I would like safe drivers to buy my motor insurance product.”

The Genie crossed his arms and blinked. “It’s done,” he smiled, “Safe drivers will actively choose your insurance product over those of your competitors.”

“Amazing!” thought the COO. “OK Genie, for my next wish, I want to find a way charge more premium for dangerous drivers before they have an accident.”

Again the Genie crossed his arms and blinked. “Your wish is my command. Poor drivers will automatically get smaller discounts. You will know how well your policy holders drive as they drive. In fact, you will be able to coach them to be better drivers as they go. Bad drivers won’t like the net premium you charge, and will move to your competitors.”

“Awesome!!” thought the COO. “OK Genie, for my last wish, I want you to reduce claims and fraud – make my motor line of business really profitable.” Once again, the Genie crossed his arms and blinked. “Your wish is granted. Claims will drop by at least 20% and fraudsters will find my magic accident reconstruction technology difficult to overcome and will move to easier pickings with your competitors.” intoned the Genie.

Telematics the fantastic

The Insurance COO was dumbfounded. He stammered: “Oh great Career Genie, what is your name?” The Genie replied, “Some know me as UBI the amazing, others know me as Telematics the fantastic. I am a magical creature who simply likes to help mortals such as you to find better ways to do business. I hope your wishes work out for you.”

In a flash, the Genie disappeared and the COO was left alone, with his loss ratio sitting at 80, his customer renewal rate at 96% and his customer satisfaction going through the roof. Happily he headed back to the office, ready to recommend a brisk beach walk to all the other senior executives.

UBI is not a fairy tale

Yes, this story is a fiction, but the results are very real.

Usage Based Insurance (UBI) is fast becoming a mainstream game-changing offering for General Insurers in the US, Europe and elsewhere directly due to the outstanding results it delivers for insurers and customers.

The first truly successful UBI programme was Progressive in the US with their patented Snapshot technology that was introduced in 2010. As of the end of 2013, the programme has achieved over US$1.5 billion in annual premiums with nearly 35% of motor customers having signed up.

Customers are given discounts up to 30% by opting into the programme. Snapshot works through a device linked to the vehicle’s On Board Diagnostic Interface (OBDI) which captures the distance driven, braking force, and the time of journey and transmits the journey data back to the Insurer enabling the calculation of premium discount. Progressive continues to enhance Snapshot and is currently planning to add GPS location data.

A number of other large US P&C insurers have become fast followers, most notably Allstate with Drive wise, State Farm with Drive Safe & Save, plus another 10 carriers with similar programs.

Drive like a girl

In Europe, some legislation has stepped in to help drive UBI adoption. In the past, some premium rating factors discriminated based on gender with young males paying more premium than young females.

This practice is now banned under EU regulations and has spurred one UBI programme called “Drive like a girl” which combines a clever social media pitch to promote safe driving habits in young drivers while premium discounts are calculated in a gender neutral fashion, based purely on how the insured drives.

A recent study shows UBI programmes in the UK, Ireland, France, Germany, Spain, Italy, Belgium, Netherlands, Denmark, Finland and Sweden involving well over 50 insurers. It also estimates the global policy count to be over 5 million as of mid-2013.

Here in Asia, I am aware of established UBI programmes in Japan, China and Australia.

So what’s the buzz?

The UBI Genie is out of the bottle and more and more markets are catching on. The value proposition is really game-changing:

• Safe drivers will tend to opt-in to UBI programmes as they believe they will get a better deal and be rewarded for their superior driving skills;

• Poor drivers will migrate away simply based on price, if they can get a cheaper base deal;

• Overall the UBI approach appeals to people’s common sense fairness – you drive less, you pay less, you drive more, you pay more – you pay for what you use;

• Driver behaviour/style is monitored and where UBI provides feed-back, drivers tend to drive more safely;

• UBI programmes are statistically proven to reduce claims, and in some instances have achieved up to 30% reductions – this has the biggest impact on insurers’ bottom lines where typically motor makes up 65% of the portfolio and claims make up 70% of expenses;

• Claims are much more difficult to stage, since the UBI device records many of the vehicle’s performance data, geo-location data and coupled with Dashcams, accidents are easy to reconstruct, thereby chasing away fraudsters to competitors;

• Since UBI provides rich data and customer engagement, claims can be settled faster, thereby improving customer satisfaction; and

• Because the pricing is dynamic based on how you drive, it becomes more difficult for customers to do an apples to apples comparison between different insurance providers policies when shopping around.

A platform for value-added services

In the past, you bought your policy, tucked the schedule in the glove compartment and forgot about it until you had a claim, at which time your insurer became your adversary.

With the UBI model, your insurer is right there in the vehicle with you on every journey, telling you when you brake too hard, alerting you when you accelerate too quickly, letting you know when you are swerving and swapping lanes too much. Your insurer is engaging with you – partnering with you to avoid accidents, and to be a better more efficient driver.

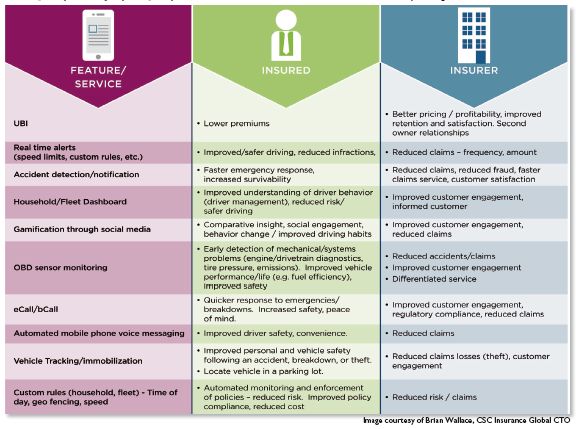

This is a perfect platform for introducing value-added services; see some examples in the table below. The UBI programme is serving up a great data set from which the insurer can potentially craft personalised services with relevance to each individual driver.

Ideally, the value created, will entice the insured to share even more data from which further services can be fashioned. With UBI customers focused on value, it becomes much more difficult for other insurers to compete simply on price. Policy retention rates and customer satisfaction will naturally increase.

The bottom line

It is clear that insurers in the region are starting to look at UBI. The rewards are immense for those that adopt this game-changing approach. Do not wait to stumble over your own Genie on the beach. Do your career and your customers a big favour by checking out this new approach to motor insurance. After all, if you don’t, your competitors certainly will.

Mr Andrew Dart is an Industry Strategist at CSC.