Critical Illness (CI) insurance cover is mostly targeted at young adults rather than the elderly. However with the growing ageing population and lower birth rates in many countries, demand for CI policies will increase. In this extract taken from The Geneva Association newsletter, Mr Tim Eppert of Gen Re examines this scenario and suggests what a CI product that is directly addressed to the older generation should look like.

Critical illness (CI) insurance provides a financial lifeline to people facing the consequences of being diagnosed with a severe disease. Hundreds of thousands claims have been paid to people suffering from cancer, heart attack and other life-threatening diseases.

While most products are targeted at young adults or even children, they often offer protection into the higher ages and thus it is time to think about the impact of the demographic changes we observe.

In almost all important insurance markets, individual life expectancy has increased enormously during the past decades and is likely to increase further in the future – while birth rates fall in many countries. Although many societies are in the process of ageing, it is not yet possible to visualise the impact of this on CI insurance.

One reason is the lack of penetration the product has into this market – a fact borne out by the findings of Gen Re’s most recent market survey. The proportion of in-force CI policies held by people over age 60 is still marginal (see Table 1). Up to now, younger consumers are seen as the main target group in many markets.

CI demand by people aged 55 and above

There is also political pressure and an economic incentive for insurers to address the demand for CI insurance from people aged 55 and over. While traditional target groups will shrink in coming years, the proportion of wealthy and healthy consumers close to retirement age is set to grow in many markets.

Insurable interest continues even in retirement and not only if direct medical expenses need to be covered. The potential still exists to incur costs for short-term care following a medical event or when making housing adaptations to accommodate new disability, for example.

Income protection (IP) insurance has only a minor role, if any, to play for retired people, and their need to insure residual debts should also diminish. Hence, the insurable amount required by individuals should be smaller in the higher ages than in the younger ages for many markets.

In this scenario, it becomes increasingly relevant that CI policies sold today work effectively in the future when a significant proportion of in-force policyholders have aged into their 70s and 80s. It is also appropriate to ask at this point what a CI product that is directly addressed to the older generation should look like.

Shifts in claims and diseases

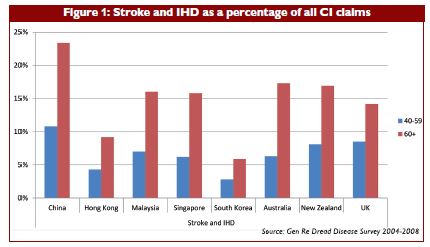

Cancer is currently responsible for almost 90% of all female CI claims in many markets. It is already possible to trace a marked increase in the proportion of cardiovascular disease claims compared to the age group 40-59 (see Figure 1). From population statistics it is possible to infer this effect will be even more pronounced for women in their 70s and 80s.

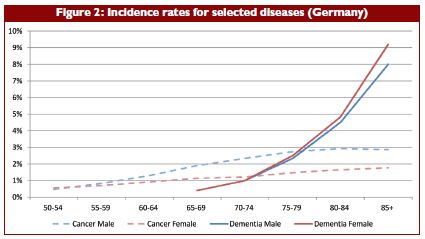

A major issue in higher ages will be dementia. As dementia in young portfolios is almost non-existent, insurers risk not focusing enough on this disease. A comparison of population rates for cancer and dementia reveals how strongly the weight of certain diseases on claims experience may change with increasing age (see Figure 2).

Consideration must be given to shifting medical guidelines if major organ transplantation or other surgical procedures are included in the scope of CI cover sold to older persons. Improvements in clinical practices, coupled with improved life expectancy, may increase the maximum age limits of people undergoing certain treatments and interventions, and this in turn could impact on future incidence rates in this area.

Incurring claims from elderly persons imply that a high proportion of claimants will have multi-morbidity. A study of 85-year-olds found that 68% had at least two chronic diseases. This can complicate CI claims management, as it will not always be clear what disease caused which physical limitation.

A possible response is to price for a lump sum disability benefit or long-term care cover based on an “activities of daily living” (ADL) definition. When the combined consequences of the multiple diseases are severe enough to fail ADLs, a claim is payable whether or not it is possible to link the physical decline to a specific disease. For the specific diseases, however, it becomes more important to stress that the severity levels, which are part of the disease definition, must be caused by this specific disease.

Underwriting

For a young target group, the maximum end age will only have a small influence on underwriting requirements. However, if dementia is covered without an age limit, dementia-specific questions can improve the underwriting result.

But a standard underwriting approach is reaching its limits if such a product is to be systematically sold to the 55+ generation. Classic risk factors such as hypertension are much more prevalent in the higher ages than in the younger ages. This means they work less successfully as indicators of substandard risks in an underwriting context for elderly lives. Using these classic risk factors in the same way as for a 20-year-old would lead to unacceptably and unnecessarily high declinature rates. Compared to these risk factors, existing disease and treatment become more important to identify sub-standard risks.

The increase in existing disease and disease risk factors hinders the effectiveness of underwriting in the absence of intensive individual assessment, which in turn leads to an increased risk of asymmetric information and anti-selection.

A limitation on the upper age limit for the entry age (eg, age 70 or 75) is recommended, especially when an insurance company is just starting to sell to higher age groups and still needs to gather experience.

Product design

For the highest ages, claims will not only become more frequent, but it is harder to derive rates for these ages.

Even in markets where CI is a commonly available product, insurers will rely on population data to some extent, while there is only a small number of insureds in the highest age category. Population statistics must be adjusted, as the underlying definition is different and the selection effect for the insured portfolio needs to be calibrated.

In addition, the very long durations between entry age and maximum covered age make it difficult to estimate how medical progress and changes to disease screening and social behaviours will impact the observed incidence rates over time. Taking this uncertainty into account will lead to a further increase in costs for old-age CI.

On the other hand, policyholders’ disposable income will typically not increase much after retirement and, in most cases, is likely to be significantly less than before. Unaffordable premiums in the higher ages are unlikely to meet customers’ needs, nor are they a suitable solution for reducing insurers’ exposure in the higher ages, as the likely lapses would be highly anti-selective.

Keeping it affordable

What are ways to limit the uncertainty for the insurer and keep the product affordable for the client?

One consideration is that robust definitions with objective severity criteria become even more important when higher ages are covered. Compared to a payout on any diagnosis, the risk of deteriorating claims experience is strongly reduced due to medical progress or changing screening behaviour.

In addition, if only severe events are covered, fewer claims are to be expected for each age. Where CI is not mainly sold to cover direct medical expenses, this approach is also adequate for elderly insureds. For example, a minor stroke might reduce the ability to work but will often still enable an independent life during retirement; thus, the need to cover early events is diminished.

In addition, it makes sense to decrease the capital at risk with a market segment increasing in age, especially if the product contains guaranteed premiums. One possibility would be the reduction of the sum insured over time – just as it is implicitly implemented, for instance, in credit life insurance – in line with the decreasing insurable interest.

This can reduce the risk for the insurer and limit the insurance costs for the policyholder. Another option is to use CI cover as an accelerator to a life insurance policy. At the very least it should be ensured that inflation protection and other increase options cannot lead to unreasonably high sums assured in the long run.

For a product with the end-age set during retirement or even whole life cover, a level premium makes more sense than risk premiums. As life expectancy is likely to increase, insurers may find that insured lives live longer than expected. A long premium payment period can help to ensure that at least a part of this prolonged cover is paid for.

If minor diseases with partial payments are covered as well, these should not lead to a waiver of premiums.

There will still be insurers that do not want to offer cover beyond retirement. To cope with current and potential future anti-age discrimination laws, they may think about selling policies with a fixed duration instead of a fixed end-age.

Robust definitions and limited sums at risk for higher ages

Demographic transition offers chances, and insurers who directly address elderly consumers can gain new and wealthy target groups. They will, however, need to rethink their underwriting process and product design.

All insurers that offer cover up to the higher ages – whether they concentrate on current target groups or not – will be affected by ageing portfolios. Robust definitions and limited sums at risk in the higher ages can help to manage the changing age structure. Insurers who adjust their products accordingly will be rewarded: due to increased awareness of the risks of critical illnesses in ageing societies, excellent marketing perspectives exist.

Mr Tim Eppert is Senior Pricing Actuary, Research & Development at Gen Re.