In EY’s global insurance CFO survey, conducted in 2014, the participants operating in Asia ranked implementing new regulatory and financial reporting requirements and being a better business partner as their first and second priorities, respectively, through to 2020. In order to transform these and other capabilities over the next five years, the effective integration of finance, risk and actuarial functions will be crucial. Mr Ranjit Jaswal and Mr Phil Gough of EY look at the priorities and challenges of finance and actuarial functions in insurers across Asia.

Executive summary

Insurance companies in Asia, both multinational and domestic, are faced with a similar set of business drivers, priorities and challenges as those their peers in Europe or North America are facing.

Over the coming years, changes emanating from North America and Europe will lead to insurers in Asia implementing new financial and regulatory reporting requirements, such as IFRS 4 Phase II, IFRS 9 and Risk-Based Capital (RBC).

We expect that these will preoccupy finance and actuarial teams at various stages throughout the next five years and, naturally, will bring about some challenges in striking a balance between delivering value to the business and meeting reporting demands.

Our experience with European insurers having to comply with Solvency II was that it placed an increasing amount of pressure on both the finance and actuarial functions and the infrastructure that supported them. It appears that the perpetual challenge of ongoing change will continue for insurers in various guises over the coming years.

In the global survey, respondents ranked challenges in technology, data and people as the top three, and some insurers already seem to have improvement plans in place to address their specific challenges.

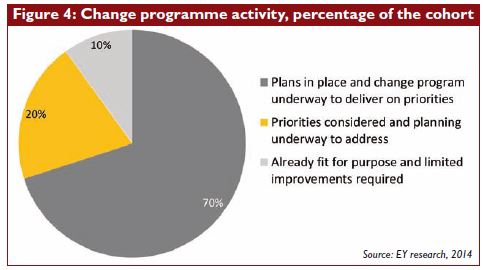

Of the 10 insurers whose survey results are included in this article (the cohort), 70% said they have launched improvement projects, while 20% say they are in the planning stage. Across the region, we believe that between 30% and 70% of insurers have recognised that investment is required, and planning is underway. In our experience, there is still some way to go.

Redefining the relationship from coexistence to cooperation in the areas of finance, risk and actuarial is necessary to build better alignment between the systems and to support stakeholder confidence.

Priorities and challenges

Based on the CFO survey results of the cohort, our major findings highlight:

• 80% of the cohort rank “implementing new regulatory and financial reporting requirements” among their top three priorities for the next five years.

• 70% of the cohort rank “being a better business partner” among their top three priorities for the next five years.

• 40% of the cohort cite responding to regulatory change as the number one business driver, with 80% of participants ranking regulatory change among the top three business drivers.

• 80% of the cohort rank data and technology issues among the top three challenges facing the finance and actuarial departments.

• 70% of the cohort have launched improvement projects, while 20% are in the planning stage.

The responses to a selection of the survey questions for the cohort of 10 and for the Asian markets included in this research are shown below.

Primary business drivers

Survey question: Please rank in order the following business drivers facing your organisation through 2020 (See Figure 1).

Of the cohort, four rank regulatory change as the number one business driver, while three rank regulatory change in second place. Across Asia, markets consistently ranked responding to regulatory change in first place, with the exception of Thailand, Vietnam and Singapore, where growth ranked as the highest priority.

In the next five years, the global insurance industry will continue to see significant regulatory and reporting change, with the International Accounting Standards Board (IASB) and the Financial Accounting Standards Board (FASB) both proposing changes to accounting for insurance contracts, and the replacement of the IASB’s IAS39 with IFRS 9 – Financial Instruments, and Solvency II (for European insurers) coming into effect.

Multinational insurers will have to comply with the regulatory requirements of their parent companies in the Americas and Europe, as well as in-market local demands. Most notably, a number of regulators are either introducing some form of RBC or are revisiting their existing RBC frameworks. For example, Singapore and Thailand are consulting with the industry on second-generation RBC frameworks while others, such as mainland China with its C-ROSS and Hong Kong, are considering moving in that direction.

In our view, compliance costs will continue to rise. Improving economies are stimulating new growth strategies for insurers; however, coupled with this are growing regulatory demands and competitive pressures. While the survey results indicate a growing confidence in Asian economies and growth will be a primary driver, a balance with cost control and regulatory rigidity will be needed.

Finance and actuarial priorities for 2020

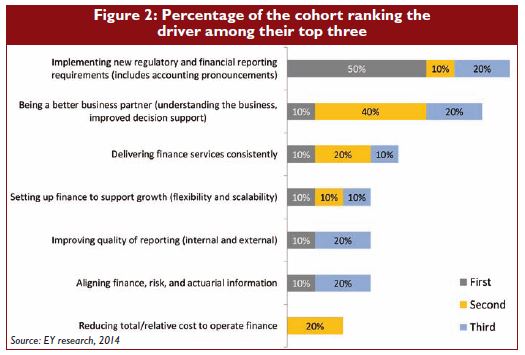

Survey question: Please rank in order the following finance and actuarial priorities facing your organisation through 2020 (See Figure 2).

Among the cohort of 10, eight ranked implementing new regulatory and financial reporting requirements among the top three priorities, with five ranking it as their highest priority. Being a better business partner ranked in second place overall among the 10 insurers while being ranked in first place overall in the global survey.

Implementing new regulatory and financial reporting requirements was ranked first for Hong Kong, Indonesia, Malaysia, the Philippines, Singapore and Thailand, with IFRS changes and second-generation RBC frameworks among the reasons cited.

Across Asia, being a better business partner was ranked in second place for insurers in Hong Kong, Singapore and Vietnam while the respondents in Thailand and the Philippines ranked it third.

Improving the quality of reporting was ranked first for Vietnam, while respondents in Thailand and the Philippines rated it second, and Taiwan ranked it as the third priority. In Vietnam, we see that many domestic players are looking for foreign strategic shareholders and thus need to improve the quality of their reporting.

In our experience, reporting processes among insurers in Asia can be inflexible, often with time-consuming manual workarounds. Some insurers have already begun to address this, as well as the lack of transparency and clarity in their reporting processes. However, given the likelihood of continual changes, we expect increased reporting over the coming years.

Challenges facing finance and actuarial organisations

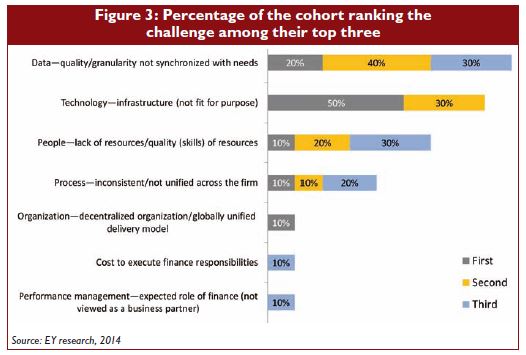

Survey question: Please rank in order the main challenges finance and actuarial organisations will need to address to become better business partners and fully participate in the execution of business strategy (See Figure 3).

In the global survey, data, technology and people were the top three challenges faced by finance and actuarial functions, and the survey results of the cohort identify the same challenges as the top three, with half of the cohort citing technology as their biggest challenge.

Across Asia, where life insurance is typically dominated by multinationals and general insurance by domestic companies, data was ranked as the biggest challenge in the Philippines while technology was ranked as the greatest challenge in Hong Kong, Malaysia, Singapore and Taiwan and for the domestic general insurers in Vietnam.

Our research also found that for the domestic insurers, talent and resourcing people is the biggest challenge, as is the case in Indonesia, Thailand and the Philippines. Talent is also a top-three challenge in Vietnam, as countries like Vietnam, with relatively low insurance penetration and density, are attractive to new entrants, and this intensifies the competition for qualified people.

Staff movements between insurers are frequent. In order to train, retain and increase the depth of technical skills, companies require a greater focus on knowledge-transfer and training.

Looking forward

Based on the survey results, the imperatives for finance, risk and actuarial in Asia are clear: fix the reporting processes, understand functional interdependencies, enhance value-add to the business, develop and deliver detailed training programmes, and achieve the right level of documentation and operating manuals so that knowledge is institutionalised.

Insurers should start improvement projects in the near future, and there may well be benefits to gain in terms of first-mover advantage. As indicated by our cohort, 90% have already launched a finance change programme or are in the planning stages of change initiatives in order to meet business demands.

Survey question: Where are you in your finance and actuarial planning to address the top five priorities? (See Figure 4).

We believe that, across the region, a number of insurance companies (between 30% and 70%) do have plans in place and change programmes underway, but the question is whether they go far enough.

Enhanced cooperation of the finance, risk and actuarial functions will deliver a better operating platform to achieve combined success.

Mr Ranjit Jaswal is Partner, Financial Services and Mr Phil Gough is Executive Director, Financial Services at EY (ey.com/insurance).

This publication contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment. Member firms of the global EY organisation cannot accept responsibility for loss to any person relying on this article.

|

Background and context

EY’s CFO survey of 35 global insurers across 10 leading insurance markets (the global survey) captured the priorities and challenges for finance and actuarial teams as they seek to support business growth strategies while addressing ongoing regulatory and cost pressures. (The full survey report can be downloaded from the EY website: http://www.ey.com/insurance).

This article focuses exclusively on the survey results of the nine multinational insurers (MNCs) operating across Asia and the single major domestic life insurer in mainland China that participated in the survey. It also captures additional insights gained by interviewing EY Assurance and Advisory partners in Hong Kong, Indonesia, Malaysia, the Philippines, Singapore, Taiwan, Thailand and Vietnam.

|