Australian life insurers turned in a relatively healthy report card for 2014, registering a 23.4% jump in after-tax profits y-o-y although its total revenue dipped 13.5% y-o-y. For general insurers though, total net profit was down 13% in 2014 while its net earned premium was up 3.2%. In this excerpt extracted from the Australian Prudential Regulatory Authority (APRA)’s Insight newsletter, we bring you a quick round-up of the market’s developments.

Life insurance

Overview

The 12 months of 2013/14 for the life insurance industry could be characterised, on one hand, as one of stability in terms of industry structure after a long period of years of merger and acquisition activity. It was also a period where the industry successfully bedded down the revised capital framework that commenced 1 January 2013.

On the other hand, 2013/14 was also a period of significant instability and uncertainty, where the cost of a slow weakening in business and risk management practices over a number of years finally became evident, crystallising into substantial declines in the performance of risk insurance business.

The industry is nonetheless well-capitalised (the capital base for the industry was 1.81 times the prescribed capital amount) and is financially well-placed to work through the current challenges.

Life insurers have been making considerable efforts to remediate their pricing and risk management practices for insurance risk business while recognising that much still needs to be done. There were some early signs that profits could be returning to more “normal” levels but it would take a few years yet before it is clear that industry actions have achieved sustainable premiums and profits.

The integration of life insurance with broader wealth offerings in many institutions meant that the adjustment to regulatory changes such as the Future of Financial Advice (FOFA) and Stronger Super reforms were also key areas of focus during 2013/14 for both the industry and APRA.

Industry structure

Stable life sector with even business distribution

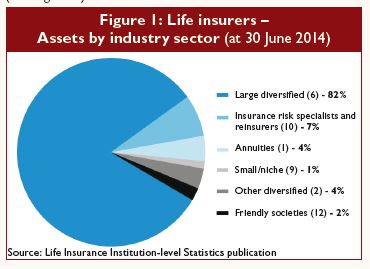

As at 30 June 2014, there were 28 registered life insurers, unchanged from the previous year. Life insurers are characterised by a heterogeneous mix of business profiles and strategies, comprising six medium to large life insurers (four of which are members of the major banking groups) selling a diversified but similar range of product types, together with a larger number of smaller but diverse life insurers specialising in niche products or markets.

Seven reinsurers (all subsidiaries of international groups) provide essential support for the risk insurance market in Australia. An additional 12 friendly societies, accounting for around 2% of industry assets, complete the mix.

(See Figure 1.)

Measured by gross assets at 30 June 2014, the largest three and five life insurers account for 76% and 85% respectively of industry assets. This level of concentration had been relatively static for a number of years and was not particularly different to that in the general insurance industry.

Many life insurers are, however, strategically centred on regular insurance risk premium revenue and its growth. From this perspective, the life insurance business is more evenly distributed across the industry, with the largest three and five life insurers writing 35% and 55% of the industry insurance risk premium respectively over 2013/14.

Financial performance

Although total revenue for the twelve months to 31 December 2014 dipped 13.5% y-o-y from last year’s A$48.7 billion to A$42.1 billion (US$32.5 billion), Australian life insurers turned in a relatively healthy report card for 2014 with a whopping 23.4% jump in after-tax profits y-o-y.

Net profit after tax was A$2.5 billion (US$1.9 billion), an increase of 23.4% from the previous year’s profit of $2.0 billion.

In terms of financial position as at 31 December 2014, total assets were A$291.1 billion compared with December 2013 assets of $273.9 billion (a 6.3% increase). Total liabilities were $267.8 billion compared with December 2013 liabilities of $252.5 billion (a 6.1% increase).

General insurance

Overview

The general insurance industry maintained a strong financial position during the year, driven primarily by the profitability of personal lines insurers in the absence of significant natural peril events.

In contrast, commercial lines insurers continue to face challenges in the current operating environment due to strong competition, excess capacity in the market and low interest rates impacting profitability.

The risk of these pressures leading to inadequate pricing by some commercial lines insurers is currently being examined by APRA, with the objective being to assist supervisors in their engagement with insurers on pricing strategies and processes. Reserving risk is also heightened at present because pressures on insurers’ results, through for example lower investment income may prompt some to use reserve releases to aid short term profitability, potentially compromising reserving adequacy.

A thematic review of insurers’ governance and risk management practices in catastrophe risk management highlighted a number of concerns. These included the reliance by some insurers on catastrophe model output used in reinsurance purchasing decisions and setting capital targets, without adequate challenge of this output. APRA provided feedback from the review to industry in late 2013 as part of the focus on improving industry practice in this area, and has been engaging with insurers during 2014 on the issues raised.

On the regulatory front, insurers successfully implemented the insurance concentration risk charge (ICRC) for a series of smaller sized loss events as from 1 January 2014. This part of the package of revised capital requirements for general insurers introduced by APRA on 1 January 2013 was deferred for one year to allow insurers time to prepare for the change.

Industry structure

Consolidation trend to continue?

There were 115 licensed general insurers and reinsurers at 30 June 2014, with 18 of these entities in run-off. To date, the 103 licensed insurers accounted for 90% of the industry’s A$114.4 billion in total assets.

Table 1 shows the steady decline in the number of licensed insurers and reinsurers in the market over the past four years. Further consolidation of insurance licenses took place in 2013/14, with most of this being due to Suncorp’s rationalisation of its insurance licenses following a group restructure.

Insurance Australia Group’s acquisition of Wesfarmers’ insurance business took effect on 30 June 2014, strengthening the market share held by large insurance groups in the personal and commercial lines markets. Despite the increasing concentration in both markets, healthy competition is evident among the large domestic insurance groups, APRA-authorised subsidiaries of foreign insurers and other local insurers.

An important source of competition in personal lines is provided by a number of challenger brands in the market, which continue to gain momentum and are starting to erode some of the established brands’ market share. Personal lines on-line aggregators continued to have a small presence in the market.

Financial performance

Total net profit after tax for the general insurance industry amounted to $4.1 billion in 2014, down from $4.7 billion in the previous year.

Charged growth in earned premium attributed to short-tail businesses

Net earned premium for the industry in the year ended 31 December 2014 was $31.7 billion, up 3.2 % from the previous year ($30.7 billion). Of this, direct insurers wrote $30.1 billion (95%).

The remaining $1.6 billion (5%) was written by reinsurers.

The increase in net earned premium was primarily driven by short-tail classes of business of domestic motor vehicle and houseowners/householders, as well as inwards reinsurance. Net earned premium for the domestic motor vehicle class of business in the year ended 31 December 2014 was $6.5 billion, up 4.1% from the previous year ($6.3 billion).

Meanwhile, net earned premium for the houseowners/householders class of business in the same period was $5.6 billion, an increase of 5.2% from the 2013 ($5.3 billion). Net earned premium for inwards reinsurance rose 6.3% from the previous year to reach $4 billion.

Rise in claims due to valuations and CAT occurrences

Gross incurred claims for the industry increased 3.6% from the previous year ($26.2 billion). The increase in gross incurred claims for the industry was mainly due to increases in gross incurred claims for the long tail classes of business of CTP motor vehicle and employers’ liability, as well as the short tail class of business of domestic motor vehicle.

For both CTP motor vehicle and employers’ liability, the increase in claims were due to the relative decrease in the Australian Government bond yield in the year to December 2014 compared to December 2013, hence impacting valuations of outstanding claims liabilities.

While the rise in gross incurred claims from the domestic motor vehicle class of business was due to higher claims experience arising from catastrophe events, including the December 2014 Brisbane hailstorm.

Insurance affordability – A hot potato

Affordability of natural perils insurance remains an area of reputational and potential political risk for the industry.

The issue received particular attention in north Queensland where the cost of property insurance has increased since the flood and cyclone events of 2011 and some insurers had chosen to withdraw from that market.

In instances where the cover for such perils is a compulsory part of insurers’ policy offering, home and contents insurance may be unaffordable. Equally, where riverine flood cover is available on an opt-out basis for properties at high flood risk, the cost of that cover may be unaffordable, leading policyholders to opt out of that cover.

In an attempt to increase competition in north Queensland, the Government has announced that it would establish a comparison website allowing consumers to compare premiums and product features for home and contents policies offered by insurers. Furthermore, the Government has clarified that licensed insurance brokers can sell policies from foreign insurers if they offer a better price to consumers.

|

Consumer protection poised to remain as main regulatory focus in 2015

The Australian insurance market has received considerable attention in 2014, positively driven by the successful listing of health insurer Medibank Private in October last year and, on the other hand, the ongoing scrutiny of the life insurance market (particularly financial advisers), said law firm Norton Rose Fulbright in a recent article, “2015 – What is on the horizon for insurance industry?”.

As such in 2015, the focus in Australia is expected to be on improving competition and market conduct than any significant reform to prudential regulation, they added.

Release of FSI report

The Financial Systems Inquiry final report (Murray Report), which was released last December, set out the scope of reforms to the financial services market that would be considered by the Federal Government in 2015.

Of the numerous recommendations, Norton Rose Fulbright said those potentially having an impact on the insurance market include:

• Conduct regulation: with an eye to regulatory developments in the UK and Europe, the Murray report recommended the introduction of a product design and distribution obligation on financial services providers, temporary product intervention powers where there is a significant risk of consumer detriment, better tools to measure insured values, increased powers to address commission and remuneration structures to align the interest of consumers with product providers and the introduction of higher training and competency standards for financial advisers.

• Market innovation: the Murray report recognises that competition and the success of the market will depend on encouraging innovation, and recommends government and industry co-operation, the removal of regulatory barriers to innovation (including more versatile product disclosure regulations), easier product rationalisation, increasing access to data, and reducing costs in respect of its use.

Little change to prudential regulation

The Murray report generally reflected the common view that the Australian market withstood the global financial crisis because of sound prudential regulation. As such, aside from recommendations aimed at improving the capital adequacy of the “Big Four” banks, very little change is envisaged for the existing prudential regulatory regime, said Norton Rose Fulbright.

It noted that in a surprising move by a regulator that has set high prudential requirements on market participants, APRA had expressed its intention to relax licensing requirements to allow unauthorised foreign insurers to enter the home and contents insurance market in far north Queensland.

The move is intended to address the lack of competition and affordability in that area caused predominantly by flood and wind risks. As such, this could create significant opportunities for offshore insurers.

Access to Justice – Class actions

The law firm also noted that the Productivity Commission Report into Access to Justice Arrangements in Australia, released on 3 December, contained both good and bad news for insurers.

The recommendation that contingency fees be allowed for the first time could see an increase in unmeritorious claims. This is exacerbated by the recommendation that restrictions on lawyers’ advertising be abolished.

On a more positive note, it said the Commission also recommended greater regulation of litigation funders, including licensing, disclosure and conflict of interest obligations.

FOS terms of reference

Lastly, Norton Rose Fulbright said since 1 January 2015, new terms of reference have also commenced for the Financial Ombudsman Service (FOS). Among other changes, the jurisdiction of the FOS will be expanded to include small business interruption insurance claims, broking disputes (for claims lodged after 1 January 2016) and uninsured third party motor vehicle disputes.

|