Public-Private Partnerships (PPP) are touted as the ideal catastrophe risk management and financing solution. In reality, the execution of this strategy in Asia is still far from being the success it is supposed to be. Who should take the lead – governments or insurers? And is there more that the insurance industry can do?

While views as to which stakeholder should play a leading role in a PPP differ, the consensus is that the ideal CAT risk management and financing solution would achieve the dual objectives of risk reduction and risk transfer. But this is easier said than done.

Public sector needs to lead risk reduction

Dr Robert Muir-Wood, Chief Research Officer at RMS said the problem with the “insurance solution alone” was that “all too often it only achieves the risk transfer” half of the equation. If it were a purely private insurance market, there may be little reason to drive risk reduction unless risks reach levels at which rates become inadequate.

Establishing a successful PPP means identifying where the two sectors can bring out its greatest capability. With adequate information, competition and trusted CAT models, the private sector can develop robust risk transfer solutions. Public sector endeavours can then focus on creating a larger role for insurance and linking activities related to building codes, zonation and improved resilience to reductions in insurance premiums.

Oftentimes however, the collaboration does not pan out as theorised. “All too often, governments apply flat-rated CAT insurance systems in such a way that it encourages maladaptive activity by builders. In addition so far, CAT insurance PPPs lack achievement around having any measureable targets for risk reduction,” said Dr Muir-Wood.

Government should form PPP backbone

Mr Tadashi Baba, Managing Director, Japan Earthquake Reinsurance Co, noted that countries in the Asia Pacific region vary in their size of national wealth and stages of economic development. Local insurers in the region are also relatively smaller in scale and weaker in financial capability in comparison with US or European insurers.

Hence, while local insurers have the market knowledge and technical know-how, governments being more stable financially, should form the backbone of a PPP and “take an active part in the regional risk financing and reinsurance programme”, he said.

Mr Baba also highlighted a 2011 recommendation report on disaster risk financing framework and options (see Recommendations for regional disaster risk financing and insurance strategy for ASEAN countries on page 32) prepared by a team of experts from the World Bank, the Global Facility for Disaster Reduction and Recover (GFDRR), the ASEAN Secretariat and the United Nations International Strategy for Disaster Reduction (UNISDR). He said he considers it as one of the best recommendation papers on this subject matter.

Government’s macro management & private sector’s support

Taking a similar stance, Mr Teddy Hailamsah, President Director of PT Asuransi Central Asia, concurred that the government should manage the collaboration, given its control over the country’s resources. “Catastrophic events such as war, earthquake or typhoon requires mobilisation on many aspects – not only financial resources, but also civil defence mechanisms, networks and equipment.”

Having said that, he added that the private sector at large, including insurers and reinsurers, should support and follow the government’s lead in restoration efforts helping to mitigate risks and minimise losses, given the private sector’s interests in ensuring businesses resume expediently in event of a disaster.

Insurers are well placed to lead

Dr Suzanne Corona, Chief Underwriter of Asia Agriculture Pool and Asia Catastrophe Pool, Asia Capital Reinsurance Malaysia begged to differ. While governments are in the position to “move mountains”, they are not specialised in risk management through insurance. A PPP collaboration – in the form of a pooling solution – can be most effective with additional partner institutions which have the expertise to provide expert risk analysis and modelling.

“Being in the businesses of assessing future losses, insurers are well placed to take the lead in organising pools by laying the foundation for product structure, terms and conditions,” she said. Drawing on their access to a long history of exposure and claims data, insurers can further lend expertise to designing solutions that abide by fundamental insurance principles and satisfies the needs of all interested parties.

However, there are also pitfalls to avoid, such as poor coordination between participating stakeholders, unrealistic expectations and a failure to achieve common understanding and interest alignment, she added.

More to be done, but what?

Asia is lagging behind the rest of the world when it comes to developing insurance, reinsurance and capital market solutions which enable workable disaster risk transfer markets, according to a recent report by the Asian Development Bank (ADB).

Dr Sittiporn Intuwonges, Senior Vice President of the Research and Statistics Department at Thai Reinsurance PCL acknowledged this lack: “Both the frequency and severity of natural disasters are intensifying, and it is quite challenging for both public and private sectors to develop applicable financial risk-sharing mechanisms against disasters. This observation is well-recognised by many developing countries, where risk market infrastructure, financial and technical resources are limited.”

True that most Asian countries are in their developing stage and are have limited resources, but developing countries also mean that there is a significant migrant population. Hence, consider this: diaspora earnings and savings.

Tapping the migrant pool

Diaspora earnings and savings can provide a significant source of financing in support of both risk reduction and post-disaster response. According to another 2013 ADB report, total developing country remittances reached three times the level of official development assistance in 2011, and are expected to rise by at least a further 65% from 2011-2014 alone.

In creating innovative products and efforts to increase insurance penetration, insurers could perhaps take the “fledgling insurance market for migrants” as an additional area of focus, to offer coverage against disruptions in flows of remittances and shocks faced by migrants’ families in their countries of origin; even including cover against natural hazards in a migrant’s home country.

Turning to the public sector, mechanisms could be established to secure flows of remittances for disaster risk reduction (DRR) initiatives that would benefit migrants’ communities back home, added ADB. Migrant organisations – such as hometown associations – already facilitate the flow of collective remittances to support infrastructural and community development projects back in the community of origin.

CAT pools should be pursued

Regionally, the establishment and participation of Nat CAT pools “should definitely stay on the agenda for the insurance industry”, said Dr Corona. “Pooling of risks is the best way to smooth the volatility inherent in an insurance portfolio, and this will have to start with concerted efforts to step up engagement among key stakeholders, especially with governments.”

Mr Hailamsah raised the Caribbean Catastrophe Risk Insurance Facility (CCRIF) as an example that perhaps the Association of Southeast Asian Nations (ASEAN) can emulate. “However, in view that the exposure to CAT risk varies for each member country, the ASEAN scheme should be designed in a way to take the ‘different exposure’ element into account, so that it would be equitable and viable for member countries to participate.”

Current thrusts remain crucial

Notwithstanding, current thrusts such as data collection and analysis, education and awareness, remain equally important.

“To develop a deeper understanding of the ‘true’ level of risk in the marketplace, we first need to identify and collect the appropriate market data in the space and then analyse the data using appropriate models,” said Mr Richard Milner, President and Chief Underwriting Officer, AXIS Re Asia Pacific.

The (re)insurance industry can be a significant driving force to both ascertaining better marketplace data and then appropriately modelling it to create innovative products that would profitably meet an unmet need, and allow businesses and individuals to make better planning decisions, he added.

Educating and increasing awareness of the consumer, is an important role that insurers hold, that can drive the success of catastrophe risk management and financing solutions, said Dr Corona. The industry needs to continuously demonstrate to clients the relevance and usefulness of such a financial tool; and it can do so by imparting knowledge to and developing real-time alert applications for the general population, among others.

Perhaps one goal to lead them all?

Regardless of views, industry players agree on several key factors that would contribute to a successful CAT risk management and financing solution: understanding risks through comprehensive data and analysis; complementing risk mitigation and prevention measures; education and awareness; a market offering demand-driven innovative products; multi-agency coordination for technical, political and financial input; and the support of governments and regulators.

As such, perhaps the question as to which stakeholder takes the lead is secondary; perhaps all stakeholders in a PPP should be led by the aligned objective of achieving disaster resilience, underscored by the above factors.

|

Recommendations for regional disaster risk financing and insurance strategy for ASEAN countries

Extract from an October 2011 Report by the World Bank, the Global Facility for Disaster Reduction and Recovery (GFDRR), the ASEAN Secretariat and United Nations International Strategy for Disaster Reduction (UNISDR).

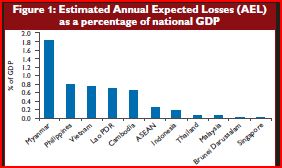

Each year, on average, the ASEAN region experiences annual expected losses caused by natural disasters estimated at US$ 4.6 billion, or 0.3% of the region’s GDP. This regional average hides a high disparity amongst the ASEAN countries due to differences in their exposure to natural hazards and the size of their economies. From the indicative analysis presented in this report, it is estimated that, as a percentage of national GDP, Myanmar, the Philippines and Vietnam experience the largest annual expected losses, standing at equivalent to 1.8%, 0.8% and 0.8% of GDP, respectively. See Figure 1.

Every 100 years on average, the ASEAN region will face disaster losses in excess of US$19 billion. Such losses will impact each ASEAN country differently. Indicative numbers suggest that Lao PDR is expected to face the highest losses relative to national GDP, followed by Cambodia and the Philippines. See Figure 2.

Natural disasters have the potential to significantly impact the fiscal budget of ASEAN governments. For major disasters (occurring once every 200 years), the contingent liability of ASEAN governments related to natural disasters could exceed 18% in Cambodia, Lao PDR and the Philippines.

ASEAN governments currently rely extensively on post-disaster budget reallocation and donor assistance to finance the cost of natural disaster response. Such a strategy can generate delays in post-disaster assistance and disrupt longer-term public investment plans and hence the development agenda.

Some ASEAN countries, however, are developing national disaster risk financing and insurance plans that promote ex ante budget planning. The Philippines recently signed a US$500 million contingent credit with the World Bank, to be drawn down in the event of a natural disaster. Indonesia and Vietnam are also exploring ex ante disaster risk financing strategies.

The development of private disaster risk insurance markets can also contribute to strengthened fiscal resilience of ASEAN countries against natural disasters. However, agricultural insurance, property catastrophe insurance and disaster microinsurance are still under-developed in most ASEAN countries.

This is the result of challenges on the supply side, such as product development, limited delivery channels, lack of technical capacity; challenges on the demand side, such as low insurance education, low awareness on exposure to disaster risks; and a need to strengthen regulatory

systems.

The report recommended several options for the development of cost-effective, affordable and sustainable disaster risk financing and insurance in ASEAN countries:

• Develop risk information and modelling systems for ASEAN governments to assess the economic and fiscal impact of natural disasters and include those risks in overall fiscal risk management strategies;

• Develop national disaster risk financing and insurance strategies, including the management of the budget volatility related to natural disasters and the insurance of key public assets;

• Establish national disaster funds as a financial mechanism to ensure the fast disbursement and execution of funds post disaster;

• Promote private catastrophe risk insurance markets through public-private partnerships and the development of enabling regulation and risk market infrastructure; and

• Strengthen regional cooperation on disaster risk financing and insurance.

The development of disaster risk financing and insurance should be supported by strong regional cooperation among ASEAN Member States. Three main areas of regional cooperation can be identified:

• Regional risk information and modelling systems;

• Regional knowledge advisory services and capacity building programs;

• Regional vehicles to leverage international reinsurance and capital markets, including risk pooling mechanisms at national, provincial and/or municipal levels and for domestic insurance companies.

ASEAN Member States may want to establish a regional programme for the development of disaster risk financing and insurance in ASEAN countries. The development objective of this programme would be to reduce the financial vulnerability of ASEAN states to natural disasters by improving financial response capacity in the aftermath of natural disasters while protecting their long term fiscal balance.

This programme would leverage the ongoing national disaster risk financing and insurance agendas in ASEAN countries and international experience, with the assistance of donor partners and the private sector.

|