Japanese insurers have accelerated their overseas expansion in recent years. In this exclusive interview, Mr Takashi Hamano, Assistant Commissioner for International Affairs, Financial Services Agency, Japan, shares how his organisation supports that development and lays out the measures that will be enforced to ensure sustainable growth of the industry. In the Q&A session transcribed below touching on topics ranging from the industry’s recent performance to IFRS standards and the Stewardship code, Mr Hamano tells us that the negative spread that Japanese insurers had to grapple with for decades is now becoming a thing of the past.

Despite initial fears of a negative impact from the increased consumption tax, record losses from the heavy snowstorm in February and typhoon claims, insurers, especially non-life insurers, have reported strong results for FY2013-2014. Would you say this is partly due to the success of FSA’s “Better Regulation”?

Since 2007, JFSA has been pursuing “Better Regulation” which consists of the following four pillars as an overarching theme for its work in improving the quality of financial regulation.

• Optimal combination of rules-based and principles-based supervisory approaches;

• Timely recognition of priority issues and effective response;

• Encouraging voluntary efforts by financial institutions and placing greater emphasis on providing incentives; and

• Improving the transparency and predictability of regulatory actions.

Better Regulation intends to provide insurers and other regulated financial institutions with proper incentives to enhance their self-discipline. JFSA is of the view that the high-level of self-discipline promoted by Better Regulation will help insurance companies enhance their adaptation and resilience in an adverse environment.

The most recent financial results of major Japanese insurers and non-life insurers (as of end September 2014) show that those insurers have recorded strong profits despite the recent adverse environment, marked by an increased consumption tax (from April 2014), record losses from the heavy snowstorm (in February 2014) and typhoon(in Summer 2014). For major non-life insurers, such strong results are mainly attributable to increase in the revenue of overseas subsidiaries and increase in premiums written in the domestic market. Those major non-life insurers have fostered their life insurance business and overseas business as profit sources in addition to their non-life insurance business and thus will be able to earn profits in a balanced way even in an adverse environment for a single profit source.

The improved results of the insurers were also attributed to brisk sales of automobile and fire insurance, expansion into overseas operations, weak yen which helped to increase investment gains and hikes in fire and auto insurance premium rates. However, with the prospect that the consumption tax going up again, what do you think needs to be done to neutralise its negative impact?

Although, the Japanese Government has raised the consumption tax rate in April 2014 as scheduled (from 5 to 8%), it has decided to postpone further increase in consumption tax rate (from 8 to 10%) until April 2017 (originally scheduled in October 2015).

In response to the consumption tax hike in April 2014, major non-life insurers have taken steps such as increasing premium rates for automobile insurance in an attempt to neutralise negative effects resulting from increased consumption tax (eg augmented agency commissions paid to sales agencies).

How does the long persisting low-interest environment in Japan affect Japanese insurers’ earnings? Will they be able to meet their liabilities?

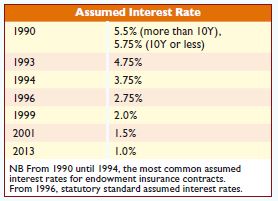

Long persisting low interest environment since 1990s has caused a “negative spread” problem (ie interest loss created by the difference in the guaranteed interest rate to policy holders and the actual investment yields) in Japan.

Under these circumstances, life insurance companies have been experiencing a difficult business environment. However, it is necessary to note that life insurance companies in general are making profits even after offsetting of the negative spread. It is partly because mortality gains from death insurances tend to be significant 1.

Moreover, assumed interest rate applicable to newly entered insurance contracts has also been continuously in decline since 1990s. The statutory “standard assumed interest rate” introduced in 1996 for the calculation of policy reserve requirements is determined on JGB yields and hence it has also been in decline continuously. Most recently, in April 2013, JFSA reduced the standard assumed interest rate from 1.5% to 1.0% for the first time in 12 years (See the table below).

This would imply that the negative spread problem mainly matters to insurance contracts entered into in the high interest rate environment in early 1990s. Those legacy insurance contracts have been decreasing in the last two decades. In addition, newly entered insurance contracts with lower assumed interest rate have increased in the same period. Against this backdrop, the negative spread problem is now being settled for many life insurance companies.

With a favourable investment environment (eg, higher stock prices and increased return from foreign securities investment) in the last two years, major life insurance companies’ have recorded strong core business profits.

In light of demographic trends, Japanese insurers might be more tempted to pursue more business overseas. In September 2014, the FSA outlined in a report from its website some of the measures that will be taken in 2014-2015 relating to the supervision and inspection of insurance companies. It said it will develop management and governance frameworks in response to the business expansion overseas. Can you elaborate on this point?

A decrease in population and an ageing population are one of the main drivers of Japanese insurers’ overseas expansion. It is important that insurance companies develop an appropriate management and governance framework in order to adequately adapt to the changing environment.

In September 2014, JFSA published its “Financial Monitoring Policy for 2014-2015” (In Japanese) 2. In the area of supervision/inspection of insurance companies, promotion of risk management upgrade and enhancement of management and governance have been identified as the most important policy objectives. This is an abridged summary of the current policy concerning overseas expansions of the insurers and is for reference purpose only. Please refer to the Japanese original for the authentic text.

(1) Promotion of risk management upgrade

Given that some insurance companies are expanding their overseas operations especially in Asia in order to diversify their business lines and profit opportunities, it is important that those insurance companies develop an ERM framework in tandem with management of profits in order to support and sustain those overseas expansions. For that reason, JFSA will promote risk management upgrade to secure financial soundness of insurance companies.

(2) Enhancement of management and governance

With regard to insurance companies with active overseas expansion, JFSA monitors business operations of their overseas establishments (subsidiaries/affiliates) and their joint business with foreign partners (joint ventures/joint partnerships etc) as part of JFSA’s monitoring of management and governance framework.

The mandatory adoption of IFRS was initially planned for 2015-2016 but was delayed due to several natural catastrophes in the country. Is the adoption of IFRS by Japanese companies high on the agenda? When is it expected to be implemented – and do you see this as having any impact on the industry?

In June 2013, the Business Accounting Council, an advisory body to the Commissioner of JFSA, published a report titled “The Present Policy on the Application of International Financial Reporting Standards (IFRS)” 3. The report states that “the time has not yet arrived to make a decision on mandatory application of IFRS in Japan when taking into account the various situations”. The report reiterates Japan’s commitment to the goal of a single set of high quality global accounting standards, and recommends the following steps:

• To encourage further application of IFRS in Japan, eliminate existing two requirements (being a listed company and having a subsidiary of material size abroad) limiting companies eligible to use IFRS;

• While continuing to allow the use of IFRS as issued by the IASB, introduce an additional set of standards identical to IFRS with limited modifications; and

• Simplify disclosure requirements on the non-consolidated single-entity financial statements.

In response to these recommendations, in October 2013, statutory requirements for eligibility to voluntary adoption of IFRS were relaxed to enable non-listed companies and companies without international activities to adopt IFRS.

Moreover, in June 2014, the Japanese Government revised its strategy paper, “Japan Revitalizing Strategy,” which was approved by the Cabinet 4.

In this strategy paper, it is clearly stated that the Government shall promote companies’ voluntary adoption of IFRS, with a view to achieving “a single set of high-quality accounting standards,” which was prescribed in the G20 Leader’s declaration. The strategy paper also sets out that the Government compiles and publishes “the IFRS Adoption Report (tentative name)” as a reference for companies considering adopting IFRS.

The number of companies voluntarily adopting IFRS has rapidly increased in recent months to 54 companies including a few non-listed companies (as of end-December, 2014). The market capitalization of the listed companies adopting IFRS is approximately US$574 billion, which accounts for 13% of the total market capitalization of Japanese listed companies.

Insurers have adopted a stewardship code earlier this year which was set by the FSA for institutional investors. They are as such increasing the pressure on companies they invest in to improve returns. It was reported that it is hoped that this code will make corporate Japan focus more on performance and be more transparent and accountable. How is the policy coming along?

In February 2014, the Council of Experts Concerning the Japanese Version of the Stewardship Code published what is referred to as the “Japan’s Stewardship Code” (Principles for Institutional Investors 5)

At the same time, the Council requested JFSA to publish and periodically update the list of institutional investors who announced their acceptance of the Stewardship Code. Most recently, in December 2014, JFSA published an updated version of the list of those institutional investors. As of end-November 2014, there are 175 institutional investors from Japan and abroad in the list, including six Trust banks, 122 investment managers, 19 Pension funds and 21 Insurance companies.

Besides, in September 2014, JFSA published the following message to institutional investors including those who have accepted the Stewardship Code in order to encourage better practices that go beyond the minimum standards.

In the same vein, “the Council of Experts Concerning the Corporate Governance Code” for which the Tokyo Stock Exchange and JFSA acted as joint secretariat published an exposure draft of “Japan’s Corporate Governance Code” in December 2014 (The draft Code is now open for public comments in both Japanese and English 6).

The draft Corporate Governance Code asks companies to take self-motivated actions for seeking sustainable corporate value. Such efforts by companies will make possible further corporate governance improvements, supported by purposeful dialogue with shareholders (institutional investors) based on the Stewardship Code. In this sense, the Corporate Governance Code and the Stewardship Code are “two wheels of a cart”, and it is hoped that they will work appropriately and together so as to achieve effective corporate governance in Japan.

Are there any other measures that you plan to introduce that would impact the insurance industry? Will there be any more new regulations in the pipeline in the near future?

In keeping up with the Financial System Council’s reports published in 2013, an important amendment to the Insurance Business Act was enacted by the Diet on 23 May 2014 and promulgated on 30 May 2014. The amended Act has been put into force on a gradual basis as elaborated below.

The background, main features and the timeline of the amendment is as follows.

(1) Background

In light of the following significant changes in business environment for insurers, the Council’s reports recommend that (i) regulatory regime for insurance solicitation shall be reviewed to respond to the changes and (ii) insurance regulation shall contribute to boosting of real economy through development of the financial business.

• Complicated insurance products and diversified sales channels;

• Emergence of “one-stop shopping agencies” soliciting for multiple insurers; and

• Growing needs for proactive business strategy including overseas expansion.

(2) Review of insurance solicitation rules

There are two main features as indicated below.

• Establishment of the basic solicitation rules: In addition to the existing solicitation rules such as the prohibition of inappropriate acts, the new solicitation rules will include more proactive rules for customers’ interests such as a duty to capture customers’ needs and a duty to provide sufficient information for the customers to make an informed decision to enter into an insurance contract.

• Enhanced regulation over independent insurance solicitors: To enhance regulation over newly emerged insurance solicitors that are independent from and not closely monitored by insurance companies (such as “one-stop shopping agencies”), a new sets of solicitation rules are introduced to require those insurance solicitors to establish an appropriate management system in proportion to their size and characteristics of their business.

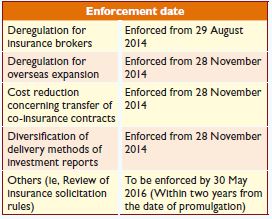

(3) Deregulation to boost the insurance market

In an attempt to boost the insurance market, the following deregulation measures were introduced.

• Deregulation for overseas expansion through M&A of foreign financial institutions: Expand the scope of business of an overseas subsidiary acquired through an M&A to include unpermitted business up to five years.

• Deregulation for insurance brokers: Abolish the existing licensing requirement to deal in a long-terms insurance contract for five years or more.

• Reduction of regulatory costs for transfer of co-insurance contracts: Allow notification to the customers by a public notice instead of customer-by-customer separate notification at the time of transfer of a co-insurance contract.

• Diversification of delivery methods of investment reports to customers: Allow new delivery methods such as browsing of an investment report at a customer-by-customer dedicated page on the insurer’s website.

(4) Timeline of the enforcement

Timeline of the enforcement of the amended Act can be summarised as follows. Because technical details of the amendment shall be prescribed by secondary legislation, JFSA has been engaged in revisions to relevant cabinet orders and ministerial ordinances (eg, “Order for Enforcement of the Insurance Business Act” and the “Ordinance for Enforcement of the Insurance Business Act”) as well as related supervisory guidelines (eg, “Comprehensive Guidelines for the Supervision of Insurance Companies”).

What do you see as the most pressing issues from the insurance industry that require regulatory attention at the moment?

The global insurance capital standard (ICS) currently being developed by IAIS as part of Comframe is of particular importance in the coming years given that ICS will be applicable to IAIGs worldwide including internationally-active Japanese insurers.

Given that Japanese insurers tend to expand their overseas operations, JFSA has been paying attention to these developments and actively engaged in the development of the standard.