Based on findings from the Milliman research report: Asia Microinsurance Supply-side Study 2020. For the purpose of this study, microinsurance is broadly defined as "risk pooling products that are intentionally designed, in terms of costs, coverage, distribution and marketing, for low-income individuals, families and businesses".

With growing interest in microinsurance in the region, Milliman undertook a first-of-its-kind study examining the supply side to gather perspectives of the insurance industry regarding the importance of microinsurance, current practices and the enabling environment. Milliman carried out this study primarily through a questionnaire survey, with responses from regulated insurers providing microinsurance in five countries- Bangladesh, China, India, Indonesia, and the Philippines. This article highlights some key-takeaways based on observations from the Philippines. Twenty-seven insurers and microinsurance providers participated in the survey, of which over 90% (twenty-five) currently sold microinsurance in the Philippines insurance market. Three of the top 10 providers by total insurance market share in the Philippines participated in the study.

Current practices: taking a closer look at insurers’ microinsurance programs and how they implement them

The most prevalent types of microinsurance products insurers currently and planned to offer remain credit-life products, followed by disability and term life cover.

With a historically solid microfinance industry in the Philippines, it is of no surprise that credit-life products are found to be the top product offered by the majority of respondents. Credit-life or loan insurance is typically imposed on borrowers as a compulsory arrangement in order to safeguard the microfinance institution (MFI) of their financial viability in the event of the death of the borrower. Whilst life coverage is important, there is a great need to evolve beyond basic life products, particularly for markets like Philippines where maturity is observed in microinsurance development. As the market matures, a more diverse range of product offerings is expected to appear in servicing broader customer needs and diversifying insurers’ risk portfolio. Yet in the case of the Philippines, the range of products offered remains analogous. A key reason which life products have largely dominated the market is because of the tax-exempt status for mutual benefit associations (MBAs). On the other hand, general taxation for the non-life sector is one of the highest in the southeast Asian region which is hampering market development in non-life products. Such phenomena also highlight the need for insurers to promote the need for product evolution and risk diversification with regulators and governing bodies particularly when tax rules are impeding market development. For the microinsurance market to evolve, there is a need to move towards complex products such as health and agricultural insurance which are both considered highly relevant to the low-income population.

Numbers refer to the number of insurers who currently offer / plan to offer this type of product.

- Reference: 44.5% is calculated = 40.0 million lives covered / 89.9 million classified as low / middle income (as at Q1 2019).

http://www.bsp.gov.ph/downloads/Publications/2019/FIDashboard_1Q2019.pdf and https://www.pewresearch.org/global/interactives/global-population-by-income/

- In the Philippines, MBAs and cooperative microinsurers are only allowed to write life products, with the exception of CLIMBS, a cooperative microinsurer and fully regulated by the IC as an insurance company, which also writes non-life products. This has forced MBAs to go to commercial insurers for non-life covers. This also means that MBAs play a dual role as insurers for life products, and distributors for non-life covers. For particularly risky life products, they may also go to the commercial sector.

- University of Cambridge (2019): Mutual microinsurance and the Sustainable Development Goals

(http://www.cisl.cam.ac.uk/resources/publication-pdfs/mutual-microinsurance-sustainable-development.pdf)

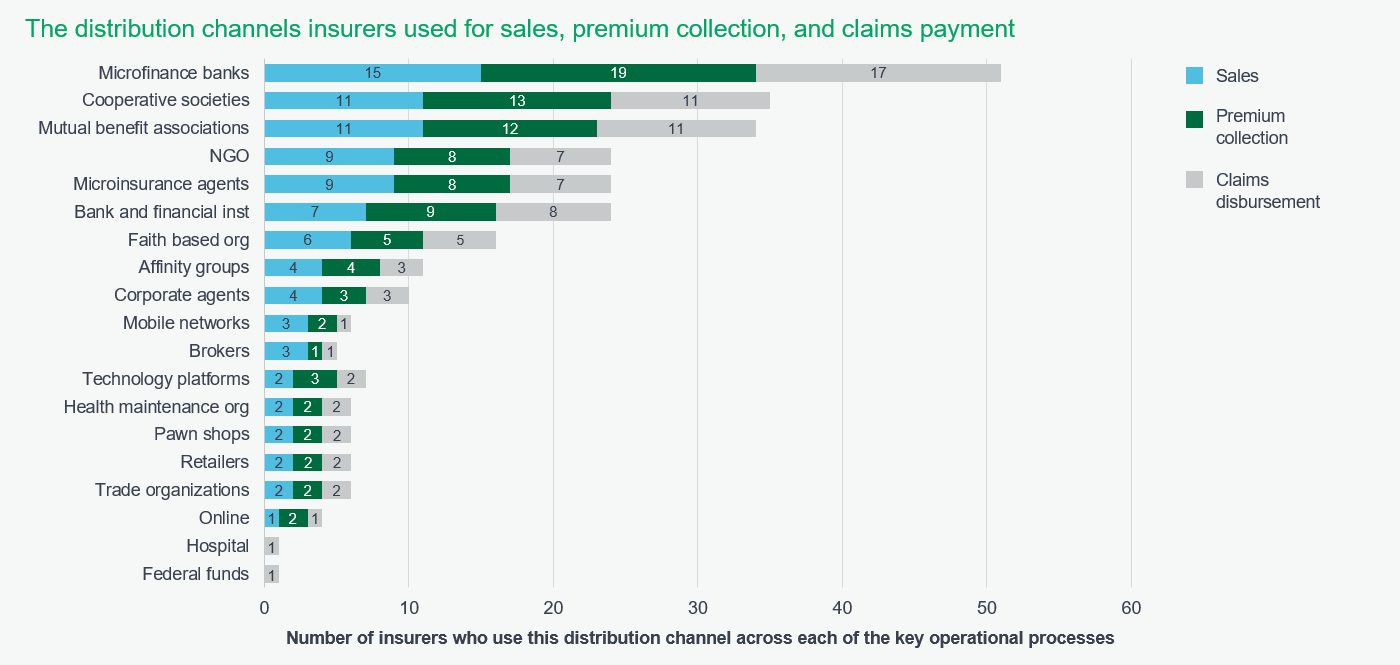

Microfinance banks, co-operative societies, MBAs and NGOs are the top distribution channels in Philippines.

The mutual sector made tremendous contributions to the growth of the microinsurance sector in the Philippines. The Insurance Commission (IC) introduced microinsurance MBAs (Mi-MBAs) as a new tier of microinsurance providers in 2006, which eventually became the key driver of microinsurance development. This served to formalize many MFIs and NGOs which had previously been operating informally. As a result, we see these channels emerging to be the top distribution outlets in the Philippines. Whilst pawnshop as a channel did not emerge as the top channel (skewed by number of insurers using this channel vs. amount in the portfolio), a significant amount of microinsurance products are sold through the vast pawnshop network of Cebuana Lhuillier (“Cebuana”). As of 2017, 30% of Filipinos covered by microinsurance sold through Cebuana, its unique selling point is its dominant position as a convenient local hub. However, the need on diversification of distribution channel for insurers should be noted in order to not become over reliant on one distribution channel. In the case of Cebuana, high commission fees are observed with fierce competition between insurers in obtaining business from this channel.

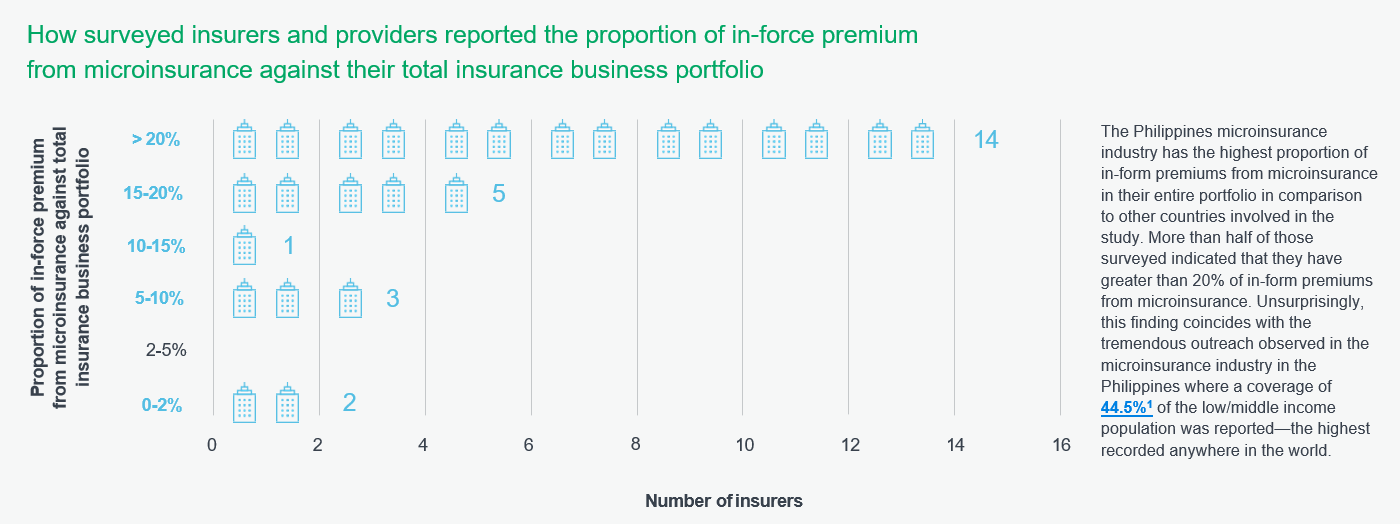

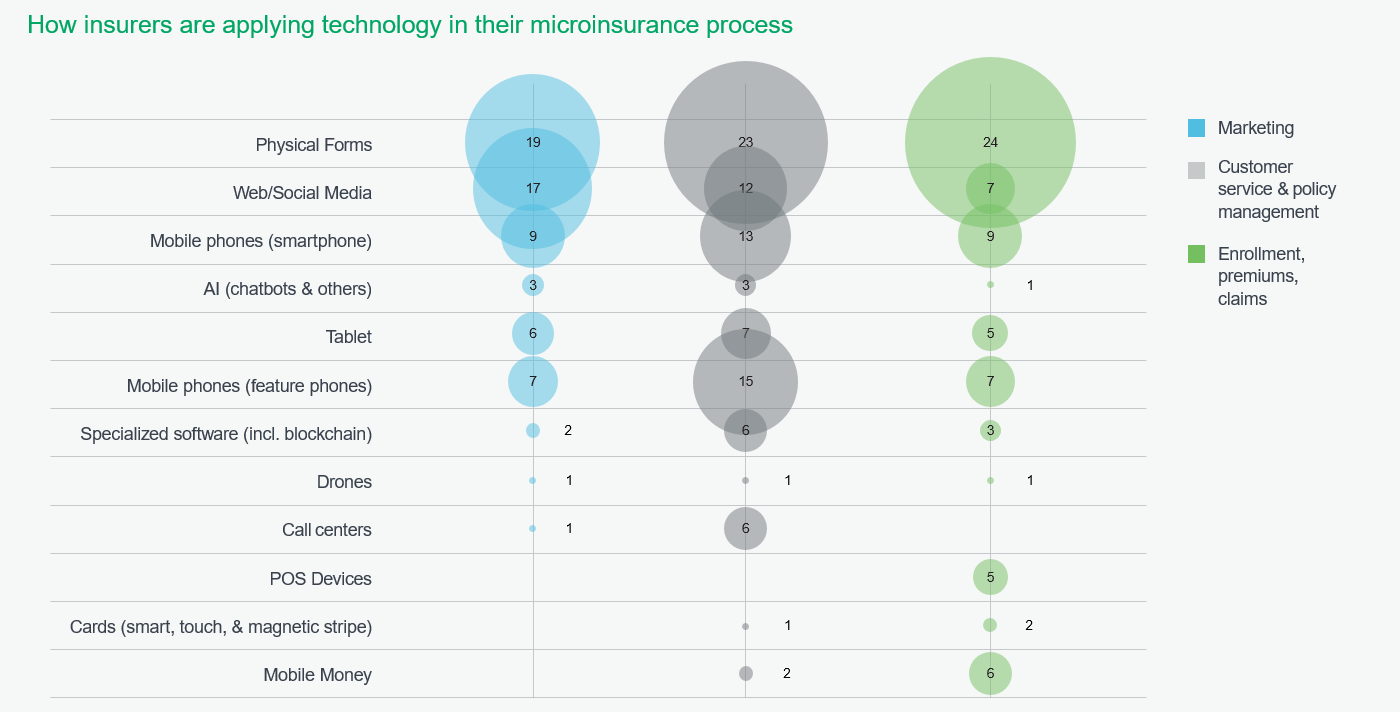

Despite the success of microinsurance in the Philippines, microinsurance providers continue to be heavily reliant on physical forms throughout all key processes. This is somewhat surprising given the high mobile phone penetration rate in the Philippines, whereby as at 2019, 65% of the population owned a smartphone and a further 24% owned feature phones, in line with the emerging economy median of 78%. A driving factor is the use of Cebuana and other money remittance networks in this market, which has been a big competitor of digital money. MBAs also suffer from resource constraints with regards to optimizing or upgrading their management information system automation. This problem is exacerbated by their restricted capacity to spend only up to a maximum 20% of their gross contributions for administrative and operating expenses. Despite the lack of technology use in microinsurance processes, the Philippines has the highest microinsurance outreach (percentage of the population covered) globally. This indicates that technology is not necessarily essential to develop a successful microinsurance model, but rather a valuable tool to help enhance the delivery and management of microinsurance.

Numbers refer to the number of insurers who have adopted this technology across each of the key operational processes.

- Cebuana (2018): Eight million Filipinos now covered by Cebuana Lhuillier microinsurance

https://www.cebuanalhuillier.com/eight-million-filipinos-now-covered-cebuana-lhuillier-microinsurance/

- Discussion with Junjay Perez, Executive Director of RIMANSI

Perspectives: insurers’ observations on their institutions and the microinsurance market

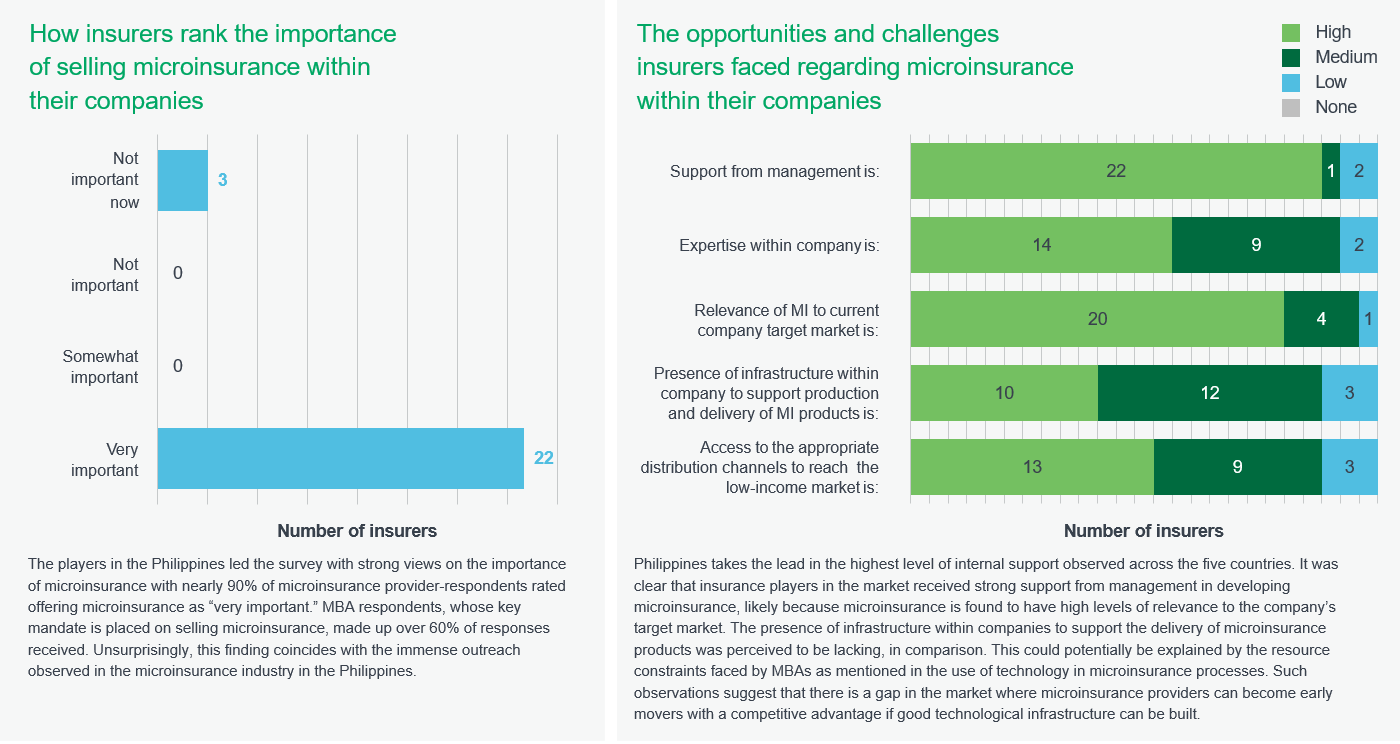

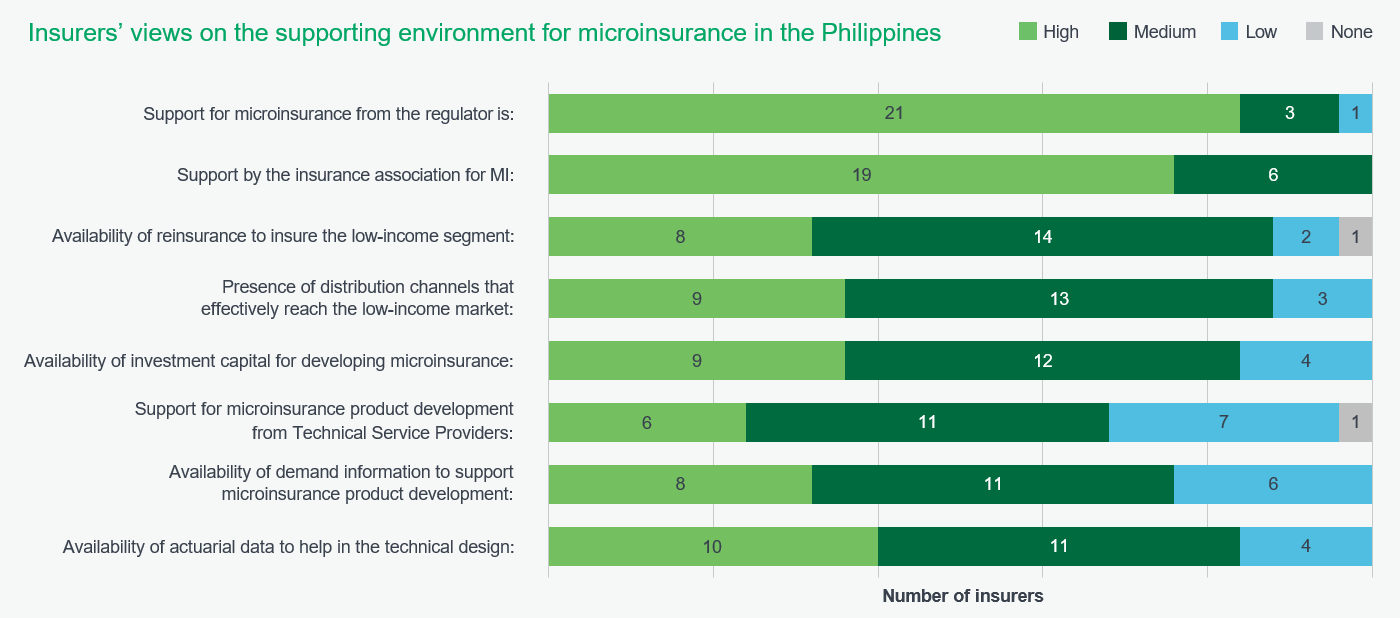

The Philippines led the survey responses with the highest level of perceived support across all pillars of success, a reflection of the strong operating environment in this country for microinsurance providers. Insurers believe that they are highly supported through facilitative regulations in microinsurance, driven particularly by the Insurance Commission (IC) of Philippines. Support form the insurance association for microinsurance was also given high ranking. On the contrary, the presence of technical service providers (TSPs) was perceived to be minimal, likely due to the absence of competition amongst mobile network operator (MNO) distribution channels in the Philippines’ MNO duopoly market; TSPs in microinsurance often partner with companies operating in the mobile telecommunications sector.

Key contacts

© 2020 Milliman, Inc. All Rights Reserved. The materials in this document represent the opinion of the authors and are not representative of the views of Milliman, Inc. Milliman does not certify the information, nor does it guarantee the accuracy and completeness of such information. Use of such information is voluntary and should not be relied upon unless an independent review of its accuracy and completeness has been performed. Materials may not be reproduced without the express consent of Milliman.